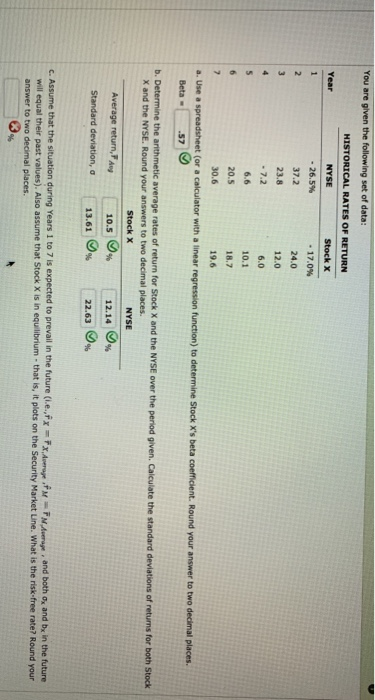

Question: how do you calculate (c) ? You are given the following set of data: Year 1 HISTORICAL RATES OF RETURN NYSE Stock X - 26.5%

You are given the following set of data: Year 1 HISTORICAL RATES OF RETURN NYSE Stock X - 26.5% 17.0% 37.2 24.0 23.8 12.0 2. 3 4 - 7.2 6.0 5 6.6 10.1 6 20.5 18.7 7 30.6 19.6 a. Use a spreadsheet (or a calculator with a linear regression function) to determine Stock X's beta coefficient. Round your answer to two decimal places. Beta- .57 b. Determine the arithmetic average rates of return for Stock X and the NYSE over the period given. Calculate the standard deviations of retums for both Stock X and the NYSE. Round your answers to two decimal places Stock X NYSE Average return. Ang Standard deviation, o 12.14 10,5 % 13,61 22.63 C. Assume that the situation during Years 1 to 7 is expected to prevail in the future (l.e.,Fx = x Avrope FM - FM Average, and both ox and be in the future will equal their past values). Also assume that Stock X is in equilibrium - that is, it plots on the Security Market Line. What is the risk-free rate? Round your answer to two decimal places

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts