Question: How to calculate this problem? Question 5 0 / 1 pts You have the following variance covariance matrix and vector of returns: A B C

How to calculate this problem?

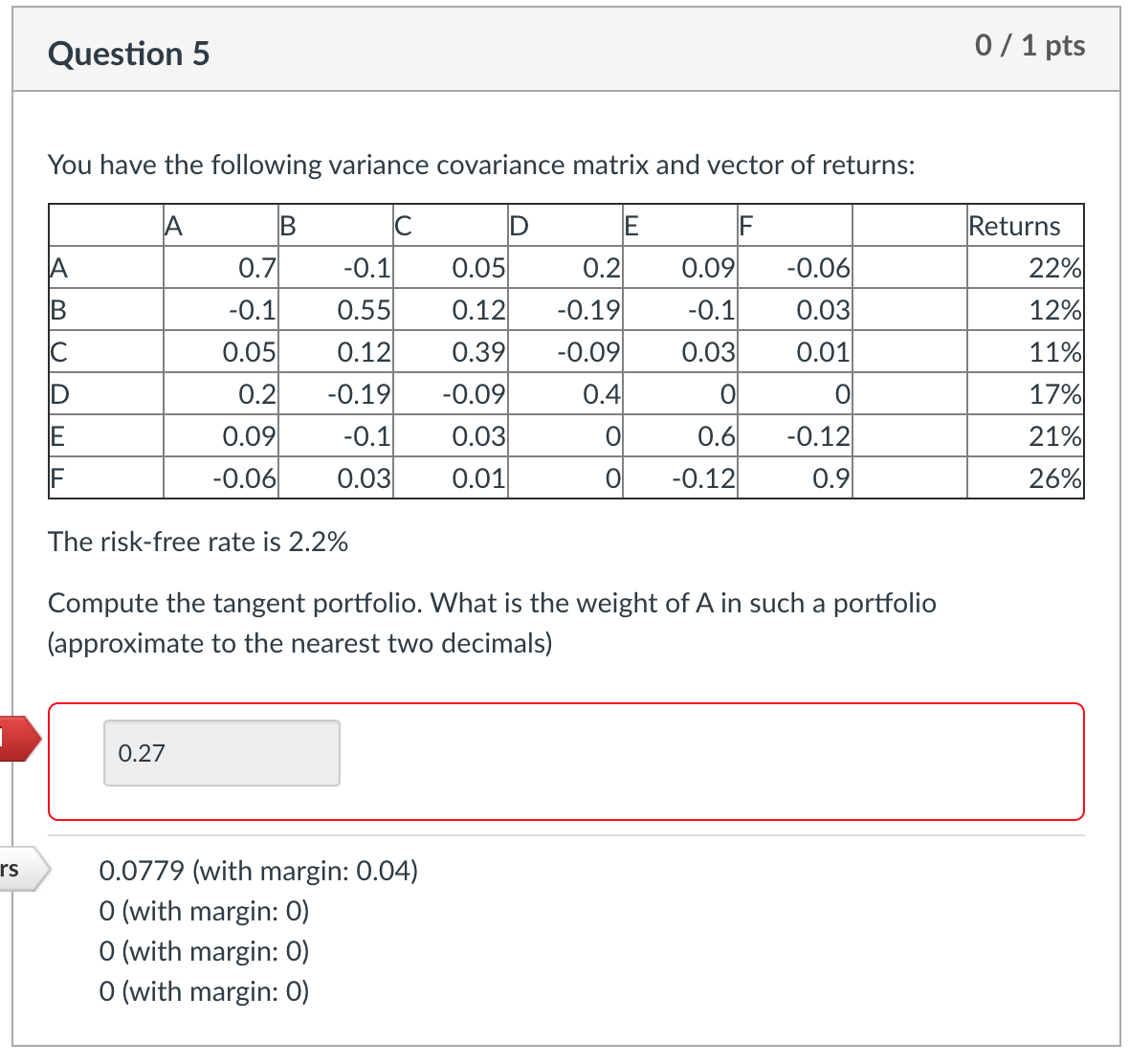

Question 5 0 / 1 pts You have the following variance covariance matrix and vector of returns: A B C D E F Returns A 0.7 -0.1 0.05 0.2 0.09 -0.06 22% B -0.1 0.55 0.12 -0.19 -0.1 0.03 12% C 0.05 0.12 0.39 -0.09 0.03 0.01 11% ID 0.2 -0.19 -0.09 0.4 O 17% m 0.09 -0.1 0.03 O 0.6 -0.12 21% TI -0.06 0.03 0.01 O -0.12 0.9 26% The risk-free rate is 2.2% Compute the tangent portfolio. What is the weight of A in such a portfolio (approximate to the nearest two decimals) 0.27 rs 0.0779 (with margin: 0.04) 0 (with margin: 0) 0 (with margin: 0) O (with margin: 0)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock