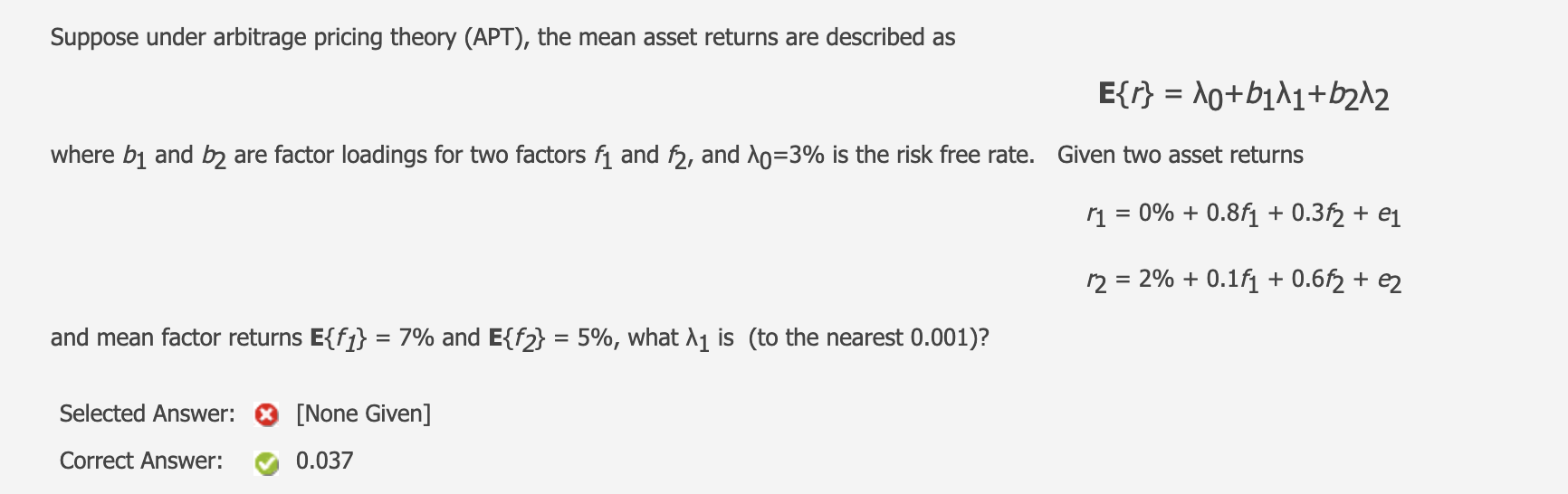

Question: How to do that Suppose under arbitrage pricing theory (APT), the mean asset returns are described as E{r} = 10+b111+212 = where by and b2

How to do that

How to do that

Suppose under arbitrage pricing theory (APT), the mean asset returns are described as E{r} = 10+b111+212 = where by and b2 are factor loadings for two factors f and f2, and lo=3% is the risk free rate. Given two asset returns r1 = 0% + 0.8f1 + 0.372 + 1 r2 = = 2% + 0.1f1 + 0.672 + ez and mean factor returns E{f1} = 7% and E{f2} = 5%, what 11 is (to the nearest 0.001)? = = Selected Answer: [None Given] Correct Answer: 0.037

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock