Question: I need 100% correct answer will be upvote A risk manager prepares a presentation on the interest rate risk of the bank's bond portfolio. The

I need 100% correct answer will be upvote

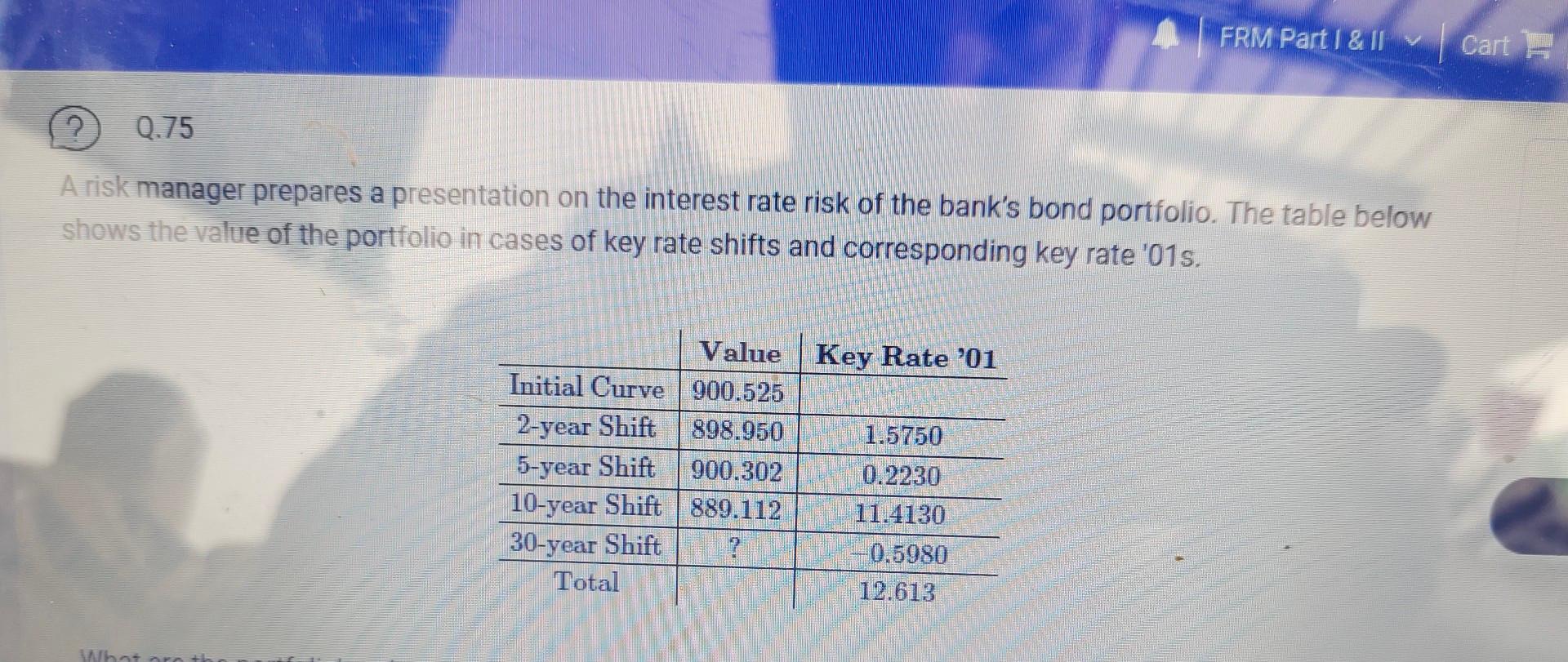

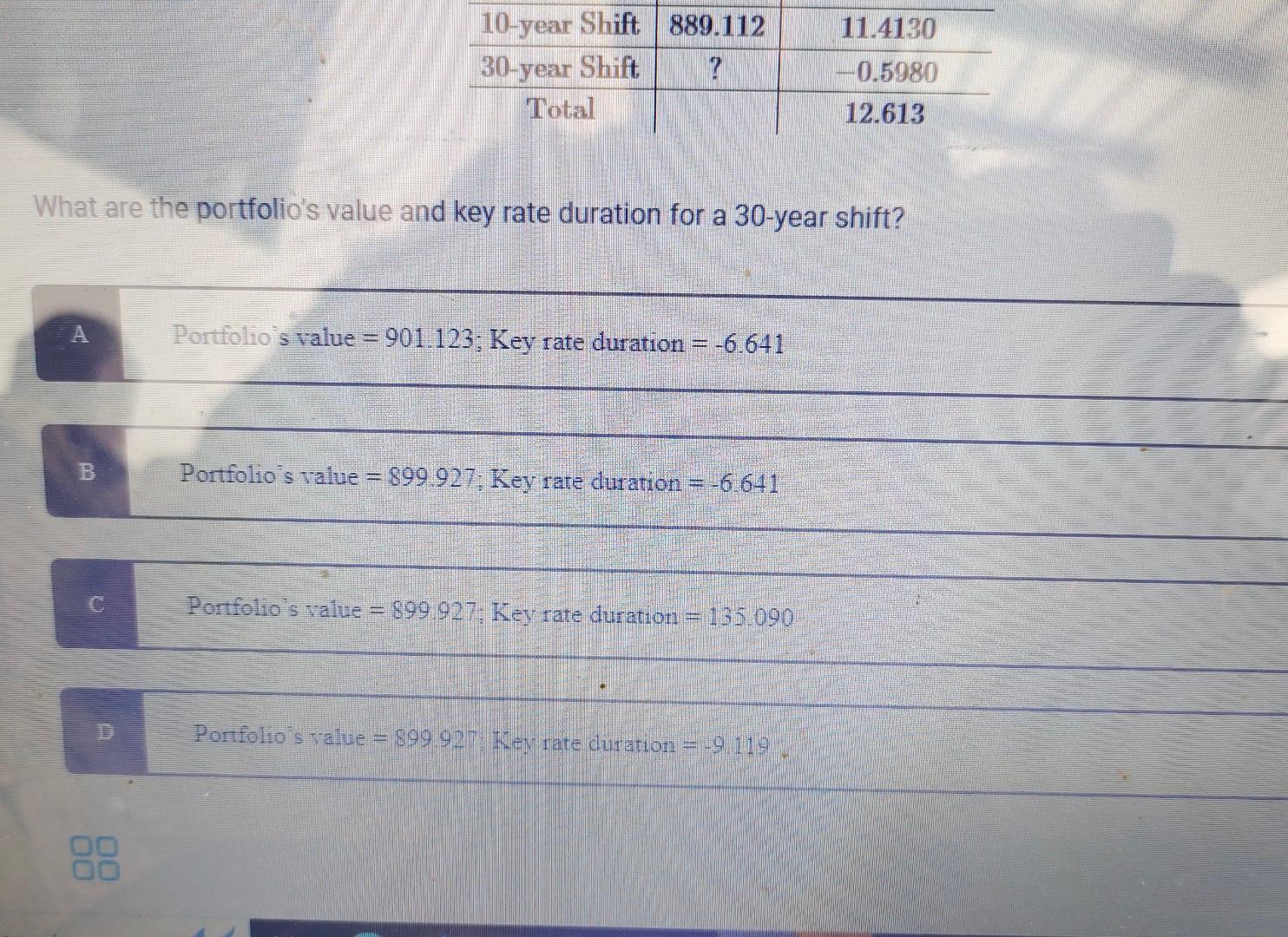

A risk manager prepares a presentation on the interest rate risk of the bank's bond portfolio. The table below shows the value of the portfolio in cases of key rate shifts and corresponding key rate '01s. What are the portfolio's value and key rate duration for a 30-year shift

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock