Question: I need help solving this problem? Suppose that a pension manager needs to fund a series of payments. The payments and the prices of zeros

I need help solving this problem?

I need help solving this problem?

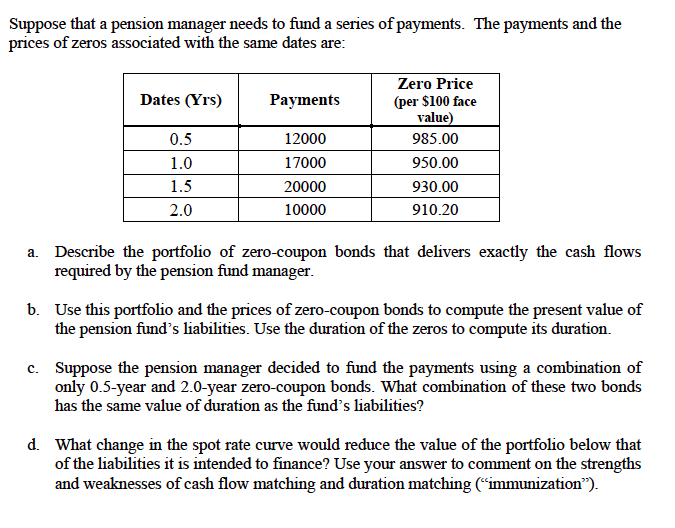

Suppose that a pension manager needs to fund a series of payments. The payments and the prices of zeros associated with the same dates are: a. Describe the portfolio of zero-coupon bonds that delivers exactly the cash flows required by the pension fund manager. b. Use this portfolio and the prices of zero-coupon bonds to compute the present value of the pension fund's liabilities. Use the duration of the zeros to compute its duration. c. Suppose the pension manager decided to fund the payments using a combination of only 0.5-year and 2.0-year zero-coupon bonds. What combination of these two bonds has the same value of duration as the fund's liabilities? d. What change in the spot rate curve would reduce the value of the portfolio below that of the liabilities it is intended to finance? Use your answer to comment on the strengths and weaknesses of cash flow matching and duration matching ("immunization"). Suppose that a pension manager needs to fund a series of payments. The payments and the prices of zeros associated with the same dates are: a. Describe the portfolio of zero-coupon bonds that delivers exactly the cash flows required by the pension fund manager. b. Use this portfolio and the prices of zero-coupon bonds to compute the present value of the pension fund's liabilities. Use the duration of the zeros to compute its duration. c. Suppose the pension manager decided to fund the payments using a combination of only 0.5-year and 2.0-year zero-coupon bonds. What combination of these two bonds has the same value of duration as the fund's liabilities? d. What change in the spot rate curve would reduce the value of the portfolio below that of the liabilities it is intended to finance? Use your answer to comment on the strengths and weaknesses of cash flow matching and duration matching ("immunization")

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts