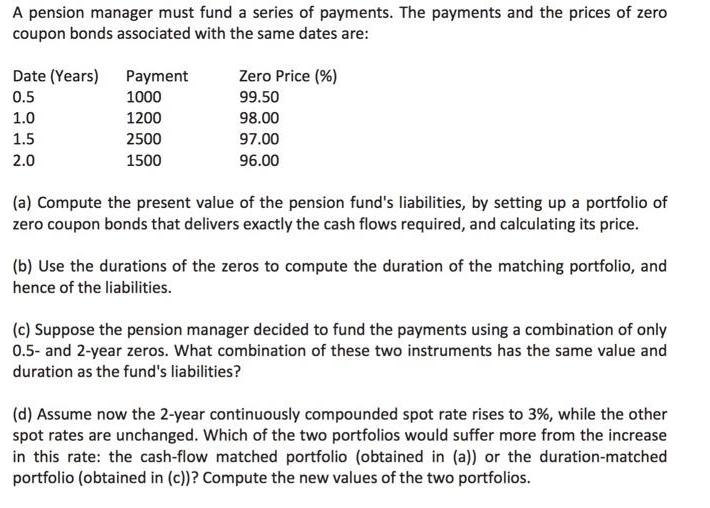

Question: A pension manager must fund a series of payments. The payments and the prices of zero coupon bonds associated with the same dates are:

A pension manager must fund a series of payments. The payments and the prices of zero coupon bonds associated with the same dates are: Date (Years) Payment 0.5 Zero Price (%) 1000 99.50 1.0 1200 98.00 1.5 2500 97.00 2.0 1500 96.00 (a) Compute the present value of the pension fund's liabilities, by setting up a portfolio of zero coupon bonds that delivers exactly the cash flows required, and calculating its price. (b) Use the durations of the zeros to compute the duration of the matching portfolio, and hence of the liabilities. (c) Suppose the pension manager decided to fund the payments using a combination of only 0.5- and 2-year zeros. What combination of these two instruments has the same value and duration as the fund's liabilities? (d) Assume now the 2-year continuously compounded spot rate rises to 3%, while the other spot rates are unchanged. Which of the two portfolios would suffer more from the increase in this rate: the cash-flow matched portfolio (obtained in (a)) or the duration-matched portfolio (obtained in (c))? Compute the new values of the two portfolios.

Step by Step Solution

3.38 Rating (164 Votes )

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts