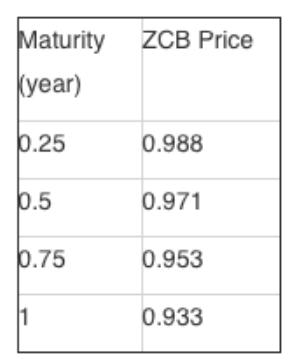

If you want to borrow $100,000 6 months later for 3 months with an FRA, what is

Question:

If you want to borrow $100,000 6 months later for 3 months with an FRA, what is the forward rate (effectively for 3 months)?

Suppose 6 months later, the 3-month annualized spot rate is 5%. What is the settlement amount of the FRA if settle at initiation?

Suppose 6 months later, the 3-month annualized spot rate is 5%. What is the settlement amount of the FRA if settle in arrears?

Instead of using an FRA directly, what positions in zero coupon bonds would you use to synthetically create the FRA borrower position?

Select one:

a. Long the 6 months zero coupon bonds and short the 9 months zero coupon bonds

b. Short the 6 months zero coupon bonds and long the 9 months zero coupon bonds.

c. Long the 6 months zero coupon bonds and short the 3 months zero coupon bonds.

d. Short the 6 months zero coupon bonds and long the 3 months zero coupon bonds.

Expert Answer:

d Short the 6 months zero coupon bonds and long the 3 months zero coupon bonds EXPLAN... View the full answer