In 1972, Dr. Ahn Chang, an MIT physics professor, moved to Portland, Oregon, to provide consulting...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

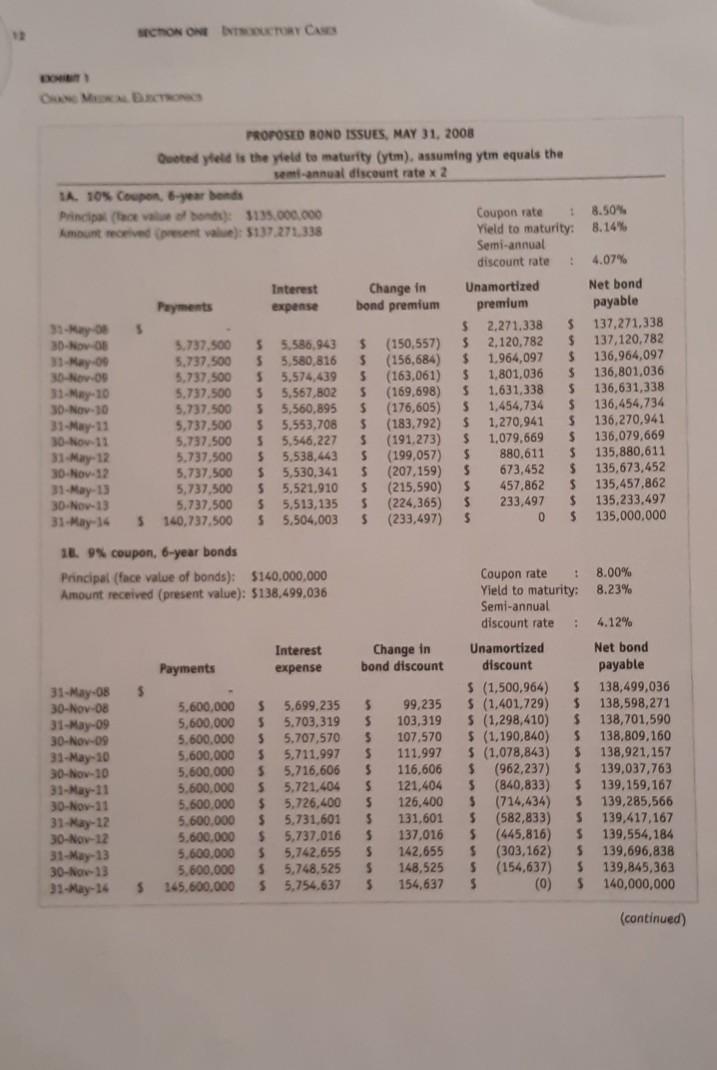

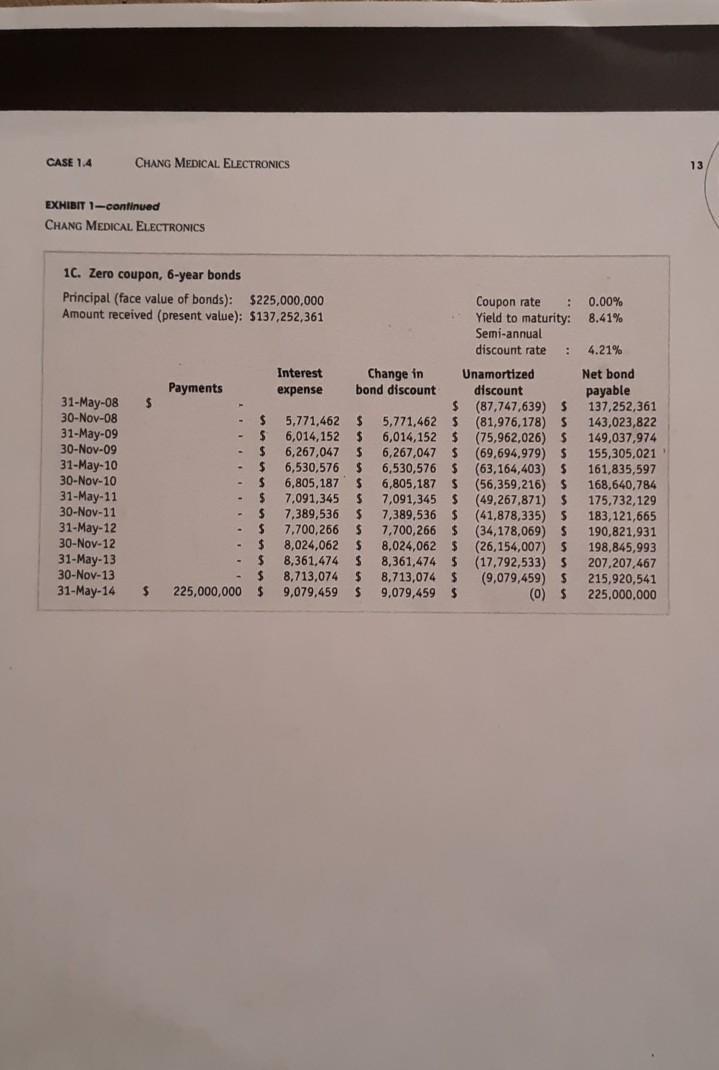

In 1972, Dr. Ahn Chang, an MIT physics professor, moved to Portland, Oregon, to provide consulting services to West Coast electronics firms. Within three years, Dr. Chang developed a proprietary health-care product, and his consulting firm evolved into Chang Medical Electronics (CME). Neither his son nor daughter was interested in working at the firm, so in mid-2008 Dr. Chang agreed to sell CME to LaSalle Capital, a private equity group. LaSalle Capital proposed to acquire CME by paying CME $10 million for 1,000,000 newly issued common shares at $10 per share and $50 million for mandatorily redeemable preferred stock that paid a 10% cumulative annual dividend. CME would then sell about $140 million of bonds to financial institutions through Rainier International, a West Coast investment bank. The $60 million investment from LaSalle Capital, plus the $140 million from newly issued debt, would be used to buy Dr. Chang's 1,825,000 shares of common stock for $102 per share ($186,150,000). Because CME would have adequate cash after the transaction closed, LaSalle Capital was unconcerned about the exact size of the debt issue. On May 1, 2008, five-year Treasuries yielded 3.1%, AAA-rated five-year corporate bonds yielded 5.57%, and Baa five-year corporate bonds yielded 6.93%. John Tilden, the LaSalle partner managing the CME acquisition, hoped to pay no more than 7.5%. Susan Hupp, the Rainier International banker managing the deal, believed the market yield to maturity would be between 8.15% and 8.5% for a small issue from a highly leveraged firm, depending on the terms. "I put together three proposals (Exhibit 1)," Ms. Hupp said. "(IA) is a six-year 8.5% bond; (IB) is a six-year 8% bond; (IC) is a six-year zero-coupon bond. Your yield to maturity should be about 8.14% with the 8.5% bond, 8.23% with the 8% bond, and 8.41% with the zero-coupon bond. I rounded each issue to the nearest $5 million so the amounts you receive under each issue differ slightly." Required 1. For each proposed issue, prepare journal entries to record the initial bond sale and the November 30, 2008, interest payment.. 2. Explain why the net bond payable changes with each interest payment. For example, explain why the net bond payable for the zero-coupon bond increases from $137,252,361 to $143,023,822 between May 31, 2008, and November 30, 2008. 3. Why are there different interest rates on the different bonds, even though they mature on the same date? Explain in detail. 4. If LaSalle needed to raise about $200 million, approximately how many $1,000 zero-coupon bonds would it issue? 5. Suppose CME issued $140 million of 8% coupon bonds on May 31, 2008, for $138,499,036, as in Exhibit 1(B). Also suppose that on May 31, 2010, immediately after it paid the $5.6 million interest payment, CME reacquired the entire bond. issue for $141,275,000. Show the required journal entry: Show the journal entry if CME instead re-acquired the entire bond issue for $137,250,000. 12 30-Nov-08 31-May-09 30-Nov-09 1A. 10% Coupon, 6-year bonds Principal (Tace value of bonds): $135,000,000 Amount received (present value): $137.271.338 31-May-10 30-Nov-10 31-May-11 30-Nov-11 31-May-12 30-Nov-12 31-May-08 30-Nov-08 SECTION ONE INTRODUCTORY CASES 31-May-09 30-Nov-09 31-May-10 10 30-Nov-10 31-May-11 30-Nov-11 31-May-12 30-Nov-12 S 5,737,500 31-May-13 5,737,500 30-Nov-13 5,737,500 31-May-14 $ 140,737.500 31-May-13 30-Nov-13 31-May-14 PROPOSED BOND ISSUES, MAY 31, 2008 Quoted yield is the yield to maturity (ytm), assuming ytm equals the semi-annual discount rate x2 Payments 18. 9% coupon, 6-year bonds Principal (face value of bonds): $140,000,000 Amount received (present value): $138,499,036 S Interest expense 5.737,500 5.737.500 5,737,500 $ 5.737.500 $ 5,737,500 $ $ 5,737,500 5.737.500 $ 5.737,500 $ $ $ 5,521,910 S $ 5,513,135 Payments Change in bond premium $ 145,600,000 Interest expense $ $ 2,271.338 $ 137,271.338 $ 5,586,943 $ (150,557) 2,120,782 $ 137,120,782 $ 5,580,816 $ (156,684) $ 1,964,097 $ 136,964,097 5,574,439 $ (163,061) 5,567,802 $ (169,698) (176,605) (183,792) 3 1,801,036 $ 1.631,338 5,560,895 $ 5,553,708 $ 3 S 3 5,546,227 $ (191,273) $ 5,538,443 S (199,057) $ 5,530,341 S (207,159) $ (215,590) $ S (224,365) S $ 5.504,003 $ (233,497) S Change in bond discount $5,726,400 S $ 5,731,601 S 5,600,000 $ 5,737,016 S S 5.600.000 $ 5,742.655 5,600,000 $ 5,748,525 $ S S 5,754.637 Coupon rate 18.50% Yield to maturity: 8.14% Semi-annual discount rate Unamortized premium S : S $ 136,801,036 $ 136,631,338 $ 136,454,734 1,454,734 1,270,941 $ 136,270,941 4 610220 1.079.669 $ 136,079,669 135,880,611 S 880,611 673,452 $ 135,673,452 S 457.862 233,497 $ 135,457,862 135,233,497 135,000,000 0 $ Coupon rate Yield to maturity: Semi-annual discount rate Unamortized discount 4.07% Net bond payable : : 8.00% 8.23% S 5,600,000 $ S 5,600,000 S 5.600,000 S 5,600,000 S $ (1,078,843) $ $ (962,237) $ S (1,500,964) 5,699,235 $ 99,235 S (1,401,729) 5.703,319 $ 103,319 S (1,298,410) $ 138,701,590 5,707,570 $ 107.570 $ (1,190,840) S 138,809,160 111.997 5,711.997 $ 138,921,157 * 5,600,000 S 5.716.606 S 116,606 139,037,763 ? 5,600,000 S 5.721.404 121,404 $ (840,833) $ 139,159,167 126,400 S (714,434) $ 139,285,566 131,601 $ (582,833) $ 139,417,167 137,016 S (445,816) $ 139,554,184 142,655 S (303,162) $ 139,696,838 148,525 S (154,637) $ 139,845,363 154,637 S (0) $ 140,000,000 5,600,000 5,600,000 (continued) 4.12% Net bond payable 138,499,036 138,598,271 CASE 1.4 CHANG MEDICAL ELECTRONICS EXHIBIT 1-continued CHANG MEDICAL ELECTRONICS 1C. Zero coupon, 6-year bonds Principal (face value of bonds): $225,000,000 Amount received (present value): $137,252,361 31-May-08 $ 30-Nov-08 31-May-09 30-Nov-09 31-May-10 34 10 30-Nov-10 21 Mar 31-May-11 30-Nov-11 30-Nov-11 Payments - $ $ $ $ $ $ S 31-May-12 30-Nov-12 31-May-13 30-Nov-13 S 31-May-14 $ 225,000,000 $ S $ $ Interest expense Change in bond discount 5,771,462 $ 6,014,152 $ 6,267,047 S 6,530,576 $ 6,805,187 S 7,091,345 S Tu 7,389,536 $ 7,700,266 $ Coupon rate : Yield to maturity: Semi-annual discount rate : (87,747,639) S $ 5,771,462 $ (81,976,178) S 6,014,152 $ (75,962,026) S 6,267,047 $ (69,694,979) S 6,805,187 $ 7,091,345 $ Unamortized discount 6,530,576 $ (63,164,403) S (56,359,216) $ (49,267,871) S (41,878,335) S (34,178,069) S (26,154,007) S 7,389,536 $ 7,700,266 $ 8,024,062 $ 8,024,062 $ 8,361,474 S 8,361,474 S 8,713,074 $ 8,713,074 S 9,079,459 $ 9,079,459 $ 0.00% 8.41% (17,792,533) S (9,079,459) S 4.21% Net bond payable 137,252,361 143,023,822 149,037,974 155,305,021 161,835,597 168,640,784 175,732,129 183.121.665 190,821,931 198,845,993 207,207,467 215.920.541 (0) $ 225,000,000 13 In 1972, Dr. Ahn Chang, an MIT physics professor, moved to Portland, Oregon, to provide consulting services to West Coast electronics firms. Within three years, Dr. Chang developed a proprietary health-care product, and his consulting firm evolved into Chang Medical Electronics (CME). Neither his son nor daughter was interested in working at the firm, so in mid-2008 Dr. Chang agreed to sell CME to LaSalle Capital, a private equity group. LaSalle Capital proposed to acquire CME by paying CME $10 million for 1,000,000 newly issued common shares at $10 per share and $50 million for mandatorily redeemable preferred stock that paid a 10% cumulative annual dividend. CME would then sell about $140 million of bonds to financial institutions through Rainier International, a West Coast investment bank. The $60 million investment from LaSalle Capital, plus the $140 million from newly issued debt, would be used to buy Dr. Chang's 1,825,000 shares of common stock for $102 per share ($186,150,000). Because CME would have adequate cash after the transaction closed, LaSalle Capital was unconcerned about the exact size of the debt issue. On May 1, 2008, five-year Treasuries yielded 3.1%, AAA-rated five-year corporate bonds yielded 5.57%, and Baa five-year corporate bonds yielded 6.93%. John Tilden, the LaSalle partner managing the CME acquisition, hoped to pay no more than 7.5%. Susan Hupp, the Rainier International banker managing the deal, believed the market yield to maturity would be between 8.15% and 8.5% for a small issue from a highly leveraged firm, depending on the terms. "I put together three proposals (Exhibit 1)," Ms. Hupp said. "(IA) is a six-year 8.5% bond; (IB) is a six-year 8% bond; (IC) is a six-year zero-coupon bond. Your yield to maturity should be about 8.14% with the 8.5% bond, 8.23% with the 8% bond, and 8.41% with the zero-coupon bond. I rounded each issue to the nearest $5 million so the amounts you receive under each issue differ slightly." Required 1. For each proposed issue, prepare journal entries to record the initial bond sale and the November 30, 2008, interest payment.. 2. Explain why the net bond payable changes with each interest payment. For example, explain why the net bond payable for the zero-coupon bond increases from $137,252,361 to $143,023,822 between May 31, 2008, and November 30, 2008. 3. Why are there different interest rates on the different bonds, even though they mature on the same date? Explain in detail. 4. If LaSalle needed to raise about $200 million, approximately how many $1,000 zero-coupon bonds would it issue? 5. Suppose CME issued $140 million of 8% coupon bonds on May 31, 2008, for $138,499,036, as in Exhibit 1(B). Also suppose that on May 31, 2010, immediately after it paid the $5.6 million interest payment, CME reacquired the entire bond. issue for $141,275,000. Show the required journal entry: Show the journal entry if CME instead re-acquired the entire bond issue for $137,250,000. 12 30-Nov-08 31-May-09 30-Nov-09 1A. 10% Coupon, 6-year bonds Principal (Tace value of bonds): $135,000,000 Amount received (present value): $137.271.338 31-May-10 30-Nov-10 31-May-11 30-Nov-11 31-May-12 30-Nov-12 31-May-08 30-Nov-08 SECTION ONE INTRODUCTORY CASES 31-May-09 30-Nov-09 31-May-10 10 30-Nov-10 31-May-11 30-Nov-11 31-May-12 30-Nov-12 S 5,737,500 31-May-13 5,737,500 30-Nov-13 5,737,500 31-May-14 $ 140,737.500 31-May-13 30-Nov-13 31-May-14 PROPOSED BOND ISSUES, MAY 31, 2008 Quoted yield is the yield to maturity (ytm), assuming ytm equals the semi-annual discount rate x2 Payments 18. 9% coupon, 6-year bonds Principal (face value of bonds): $140,000,000 Amount received (present value): $138,499,036 S Interest expense 5.737,500 5.737.500 5,737,500 $ 5.737.500 $ 5,737,500 $ $ 5,737,500 5.737.500 $ 5.737,500 $ $ $ 5,521,910 S $ 5,513,135 Payments Change in bond premium $ 145,600,000 Interest expense $ $ 2,271.338 $ 137,271.338 $ 5,586,943 $ (150,557) 2,120,782 $ 137,120,782 $ 5,580,816 $ (156,684) $ 1,964,097 $ 136,964,097 5,574,439 $ (163,061) 5,567,802 $ (169,698) (176,605) (183,792) 3 1,801,036 $ 1.631,338 5,560,895 $ 5,553,708 $ 3 S 3 5,546,227 $ (191,273) $ 5,538,443 S (199,057) $ 5,530,341 S (207,159) $ (215,590) $ S (224,365) S $ 5.504,003 $ (233,497) S Change in bond discount $5,726,400 S $ 5,731,601 S 5,600,000 $ 5,737,016 S S 5.600.000 $ 5,742.655 5,600,000 $ 5,748,525 $ S S 5,754.637 Coupon rate 18.50% Yield to maturity: 8.14% Semi-annual discount rate Unamortized premium S : S $ 136,801,036 $ 136,631,338 $ 136,454,734 1,454,734 1,270,941 $ 136,270,941 4 610220 1.079.669 $ 136,079,669 135,880,611 S 880,611 673,452 $ 135,673,452 S 457.862 233,497 $ 135,457,862 135,233,497 135,000,000 0 $ Coupon rate Yield to maturity: Semi-annual discount rate Unamortized discount 4.07% Net bond payable : : 8.00% 8.23% S 5,600,000 $ S 5,600,000 S 5.600,000 S 5,600,000 S $ (1,078,843) $ $ (962,237) $ S (1,500,964) 5,699,235 $ 99,235 S (1,401,729) 5.703,319 $ 103,319 S (1,298,410) $ 138,701,590 5,707,570 $ 107.570 $ (1,190,840) S 138,809,160 111.997 5,711.997 $ 138,921,157 * 5,600,000 S 5.716.606 S 116,606 139,037,763 ? 5,600,000 S 5.721.404 121,404 $ (840,833) $ 139,159,167 126,400 S (714,434) $ 139,285,566 131,601 $ (582,833) $ 139,417,167 137,016 S (445,816) $ 139,554,184 142,655 S (303,162) $ 139,696,838 148,525 S (154,637) $ 139,845,363 154,637 S (0) $ 140,000,000 5,600,000 5,600,000 (continued) 4.12% Net bond payable 138,499,036 138,598,271 CASE 1.4 CHANG MEDICAL ELECTRONICS EXHIBIT 1-continued CHANG MEDICAL ELECTRONICS 1C. Zero coupon, 6-year bonds Principal (face value of bonds): $225,000,000 Amount received (present value): $137,252,361 31-May-08 $ 30-Nov-08 31-May-09 30-Nov-09 31-May-10 34 10 30-Nov-10 21 Mar 31-May-11 30-Nov-11 30-Nov-11 Payments - $ $ $ $ $ $ S 31-May-12 30-Nov-12 31-May-13 30-Nov-13 S 31-May-14 $ 225,000,000 $ S $ $ Interest expense Change in bond discount 5,771,462 $ 6,014,152 $ 6,267,047 S 6,530,576 $ 6,805,187 S 7,091,345 S Tu 7,389,536 $ 7,700,266 $ Coupon rate : Yield to maturity: Semi-annual discount rate : (87,747,639) S $ 5,771,462 $ (81,976,178) S 6,014,152 $ (75,962,026) S 6,267,047 $ (69,694,979) S 6,805,187 $ 7,091,345 $ Unamortized discount 6,530,576 $ (63,164,403) S (56,359,216) $ (49,267,871) S (41,878,335) S (34,178,069) S (26,154,007) S 7,389,536 $ 7,700,266 $ 8,024,062 $ 8,024,062 $ 8,361,474 S 8,361,474 S 8,713,074 $ 8,713,074 S 9,079,459 $ 9,079,459 $ 0.00% 8.41% (17,792,533) S (9,079,459) S 4.21% Net bond payable 137,252,361 143,023,822 149,037,974 155,305,021 161,835,597 168,640,784 175,732,129 183.121.665 190,821,931 198,845,993 207,207,467 215.920.541 (0) $ 225,000,000 13

Expert Answer:

Answer rating: 100% (QA)

2 A bond is an instrument given by borrower to pay a lender Principal ... View the full answer

Related Book For

Cost Accounting Foundations and Evolutions

ISBN: 978-1111971724

9th edition

Authors: Michael R. Kinney, Cecily A. Raiborn

Posted Date:

Students also viewed these finance questions

-

United Inc. issued 150 common shares for $9.00 per share and 250 shares for $8.50 per share. What would be the journal entry to record the combined issue?

-

Is mandatorily redeemable preferred stock classified as equity? Explain.

-

Does IFRS classify mandatorily redeemable preferred stock as equity? Explain.

-

The joint density function of the discrete random variable (X, Y) is given in Table. (a) Find E(XY). (b) Find Cov (X, Y). (c) Find the correlation coefficient ?X, Y. xl 1 2 1 y 2 3 3 1515 6 0

-

Define what is meant by scaling.

-

A gas turbine power plant operates on a simple Brayton cycle with air (use the PG model) as the working fluid. The air enters the turbine at 1 MPa and 1000 K and leaves at 125 kPa, 610 K. Heat is...

-

What assumptions underlie ecological accounting? Consider whether one assumption behind ecological accounting and reporting is more important than the other assumptions.

-

Determine the components of the reactions at A and E when a counterclockwise couple of magnitude120 N m is applied to the frame (a) At B, (b) At D. 100mm - 400 mm 250 m

-

H 5. Determine a simplified acceleration function for the following position function, s (t) = (1 + 2) (31 1+5), 10

-

Natalie Lawson spent much of her youth playing sports. She passed many hours on the soccer field and in the dance studio. As Natalie grew older, her passion for healthy living continued as she...

-

Pls Write the Summary from Text Below : Spencer Harpin and his wife Kathy live with their two sons in a small northern town on the Atlantic coast in USA. They are reasonably well off, and consider...

-

The table sets out the demand and supply schedules for roses on a normal weekend. Questions 1. If the price of a rose is $6, describe the situation in the rose market. Explain how the price adjusts....

-

Author Margie Warrell recalls keeping on wearing a pair of designer shoes even though they made her feet ache because she had paid a lot for them. She says she was thinking I need to get my moneys...

-

The Federal Trade Commission says Qualcomm is trying to corner the market for chips used in smartphones. Qualcomm has a set of patents that Intel says prevent it from competing in the smartphone...

-

List and comment on the advantages and disadvantages of both full and partial storage systems.

-

General Motors will temporarily idle five U.S. assembly plants that build sedans and coupes, such as the Chevrolet Cruze, Cadillac CTS, and Chevy Camaro, as American motorists by the millions shift...

-

The World Wide Web - a system in the global network is called: * 1 point FTP BBS WWW E - m il

-

Ask students to outline the reasons why the various elements of culture (social structures and control systems, language and aesthetics, religion and other belief systems, educational systems, etc.)...

-

Sepchek Oil Field Services is considering the installation of a new electronic surveillance system for its warehouse. The system has an initial cost of $ 160,000 and an expected life of five years....

-

In November 2013, DayTime Publishing Companys costs and quantities of paper consumed in manufacturing its 2014 Executive Planner and Calendar were as follows: Actual unit purchase price...

-

Reschman Co. manufactures two products. Following is a production and cost analysis for each product for 2013: Elysia Sanderson, the firms cost accountant, has just returned from a seminar on...

-

Does the fact that selling is included as part of the promotional mix weaken or strengthen its role as a sub-element of marketing?

-

Discuss the role and function of selling.

-

Comment on why the proposed changes to sales processes are necessary. Also, which changes would you recommend in terms of their: (a) selling activities? (b) sales value proposition?

Study smarter with the SolutionInn App