In Case 10.1, we projected financial statements for Starbucks for Years +1 through +5. In this...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

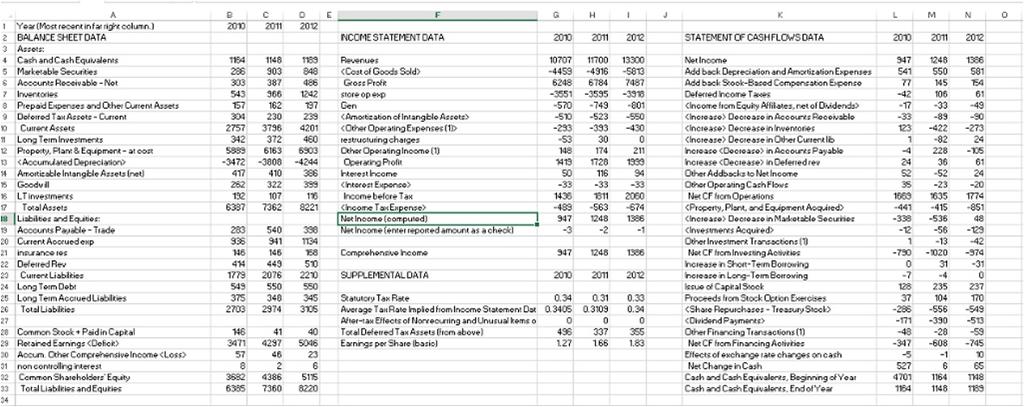

In Case 10.1, we projected financial statements for Starbucks for Years +1 through +5. In this portion of the Starbucks Integrative Case, we use the projected financial statements from Case 10.1 and apply the techniques learned in this chapter to compute Starbucks' required rate of return on equity and share value based on the free cash flows valuation models. We also compare our value estimate to Starbucks' share price at the time of the case development to provide an investment recommendation. The market equity beta for Starbucks at the end of 2012 is 0.75. Assume that the risk-free interest rate is 3.0% and the market risk premium is 6.0%. Starbucks has 749.3 million shares outstanding at the end of 2012. At the start of Year +1, Starbucks' share price was $50.15. REQUIRED Part I-Computing Starbucks' Share Value Using Free Cash Flows to Common Equity Shareholders a. Use the CAPM to compute the required rate of return on common equity capital for Starbucks. b. Using your projected financial statements from Case 10.1 for Starbucks, begin with pro- jected net cash flows from operations and derive the projected free cash flows for com- mon equity shareholders for Starbucks for Years +1 through +5. You must determine whether your projected changes in cash are necessary for operating liquidity purposes. c. Project the continuing free cash flow for common equity shareholders in Year +6. Assume that the steady-state, long-run growth rate will be 3% in Year +6 and beyond. Project that the Year +5 income statement and balance sheet amounts will grow by 3% in Year +6; then derive the projected statement of cash flows for Year +6. Derive the projected free cash flow for common equity shareholders in Year +6 from the projected statement of cash flows for Year + 6. d. Using the required rate of return on common equity from Requirement a as a dis- count rate, compute the sum of the present value of free cash flows for common eq- uity share holders for Starbucks for Years +1 through +5. e. Using the required rate of return on common equity from Requirement a as a discount rate and the long-run growth rate from Requirement c, compute the continuing value of Starbucks as of the start of Year +6 based on Starbucks' continuing free cash flows for common equity shareholders in Year +6 and beyond. After computing continuing value as of the start of Year +6, discount it to present value at the start of Year +1. f. Compute the value of a share of Starbucks common stock. (1) Compute the total sum of the present value of free cash flows for equity share- holders (from Requirements d and e). (2) Adjust the total sum of the present value using the midyear discounting adjust- ment factor. (3) Compute the per-share value estimate. Note: If you worked Integrative Case 11.1 from Chapter 11 and computed Starbucks' share value using the dividends valuation approach, compare your value estimate from that case with the value estimate you obtain here. They should be the same. Part II-Computing Starbucks' Share Value Using Free Cash Flows to All Debt and Equity Stakeholders g. At the end of 2012, Starbucks had $1,263 million in outstanding interest-bearing short-term and long-term debt on the balance sheet and no preferred stock. Assume, that the balance sheet value of Starbucks' debt equals the market value of the debt. Starbucks faces an interest rate of roughly 6.25% on its outstanding debt. Assume that Starbucks will continue to face the same interest rate on this outstanding debt capital over the remaining life of the debt. Assume that Starbucks will continue to face a 33% income tax rate over the forecast horizon. Compute the weighted-average cost of capital for Starbucks as of the start of Year +1. Compare your computation of Starbucks' weighted-average cost of capital with your estimate of Starbucks' required return on equity from Requirement a. Why do the two amounts differ? h. Based on your projections of Starbucks' financial statements, begin with projected net cash flows from operations and derive the projected free cash flows for all debt and equity stakeholders for Years +1 through +5. Compare your forecasts of Star- bucks' free cash flows for all debt and equity stakeholders Years +1 through +5 with your forecast of Starbucks' free cash flows for equity shareholders in Requirement b. Why are the amounts not identical-what causes the difference each year? 954 CHAPTER 12 Valuation: Cash-Flow-Based Approaches i. Project the continuing free cash flows for all debt and equity stakeholders in Year +6. Use the projected financial statements for Year +6 from Requirement c to derive the projected free cash flows for all debt and equity stakeholders in Year +6. j. Using the weighted average cost of capital from Requirement g as a discount rate, compute the sum of the present value of free cash flows for all debt and equity stakeholders for Starbucks for Years +1 through +5. k. Using the weighted-average cost of capital from Requirement g as a discount rate and the long-run growth rate from Requirement c, compute the continuing value of Star- bucks as of the start of Year +6 based on Starbucks' continuing free cash flows for all debt and equity stakeholders in Year +6 and beyond. After computing continuing value as of the start of Year +6, discount it to present value at the start of Year +1. I. Compute the value of a share of Starbucks common stock. (1) Compute the value of Starbucks' net operating assets using the total sum of the present value of free cash flows for all debt and equity stakeholders (from Requirements j and k). (2) Subtract the value of outstanding debt to obtain the value of equity. (3) Adjust the present value of equity using the midyear discounting adjustment factor. (4) Compute the per-share value estimate. m. Compare your share value estimate from Requirement f with your share value esti- mate from Requirement I. These values should be similar. Part III-Sensitivity Analysis and Recommendation n. Using the free cash flows to common equity shareholders, recompute the value of Starbucks shares under two alternative scenarios. Scenario 1: Assume that Starbucks' long-run growth will be 2%, not 3% as before, and assume that Starbucks' required rate of return on equity is 1 percentage point higher than the rate you computed using the CAPM in Requirement a. Scenario 2: Assume that Starbucks' long-run growth will be 4%, not 3% as before, and assume that Starbucks' required rate of return on equity is 1 percentage point lower than the rate you computed using the CAPM in Requirement a. To quantify the sensitivity of your share value estimate for Starbucks to these variations in growth and discount rates, compare (in percentage terms) your value estimates under these two scenarios with your value estimate from Requirement f. o. At the end of 2012, what reasonable range of share values would you have expected for Starbucks common stock? At that time, where was the market price for Starbucks shares relative to this range? What would you have recommended? p. If you computed Starbucks' common equity share value using the dividends-based valuation approach in Case 11.1, compare the value estimate you obtained in that case with the estimate you obtained in this case. They should be identical. CASE 12.2 Holmes Corporation A 1 Year (Most recent infar right column) 2 BALANCE SHEET DATA 3 Assets: 4 Cach and Cash Equivalents 5 Marketable Securities & Accounts Receivable-Not 7 Inventories 8 Prepaid Expenses and Other Current Assets 9 Deferred Tax Assets-Current 10 Current Assets 11 Long Term Investments 12 Property, Plant & Equipment-at cost 13 <Accumulated Depreciation 14 Amortizable Intangible Azzets (net) 15 Goodvil LT investments 17 Total Assets 18 Liabilter and Equities 19 Accounts Payable-Trade 20 Current Accrued exp 21 insurance res 22 Deferred Rev 20 Current Liabilities 24 Long Term Deb 25 Long Term Accrued Liabilities 26 Total Liabilities 27 20 Common Stock Paid in Capital 29 Retained Earnings (Delick) 20 Accum Other Comprehensive Income (Loss) 31 non controlling interest 32 33 34 Common Shareholders Equity Total Liabiliries and Eques . ************** ******** *55°18 2010 1154 303 543 157 -3472 417 387 966 162 304 230 239 342 372 2757 3796 4201 460 6163 6903 -3808-4244 410 322 107 7362 192 6387 283 414 1779 549 375 2703 146 3471 C 57 2011 2012 1148 903 540 941 D E 398 1134 158 449 510 2076 2210 550 550 340 345 2974 3105 146 41 4297 46 2 1189 848 486 1242 197 3682 4386 386 399 116 8221 140 5046 23 6 5115 6385 7360 8220 F NCOME STATEMENT DATA Revenues (Cost of Goods Sold) Gross Profi store op exp Gen <Amortization of Intangible Assets) <Other Operating Expenses (1) restructuring charges Other Operating Income (1) Operating Profit Interest Income Cinterest Expense) Income before Tax (Income Tax Expense> Net Income (computed) Net Income (enter reported amount as a checkl Comprehensive income SUPPLEMENTAL DATA Statutory Tax Rate Average Tax Rate Impled from Income Statement Dat After-tax Effects of Nonrecuring and Unusual kems o Total Deferred Tax Assets from above) Earnings per Share (basic) G H 947 2010 2011 10707 11700 13300 -4459 -4916 -5813 6248 6784 7487 -3551 -3595 -3918 -570 -749 -601 -510 -523 -550 -293 -393 -430 -53 30 174 1728 50 116 0 148 1419 211 1963 94 -33 2060 -33 -33 1436 1811 -489 -563 -674 947 1248 1386 -2 -3 -1 1 1248 2012 1306 2010 2011 0.34 0.31 0.33 0.3405 0.3109 0.34 0 0 496 337 127 166 0 355 1.83 2012 J STATEMENT OF CASHFLOWS DATA Net Income Add back Depreciation and Amortization Expenses Add back Scook-Based Compensation Expense Deferred Income Taxes Cincome from Equity Affilates, net of Dividends <Increase> Decrease in Accounts Receivable <Increase> Decrease in Inventories Cincrease) Decrease in Other Current lib Increase (Decrease) in Accounts Payable hcrease (Decrease in Deferred rev Other Addbacks to Net Income Other Operating Cash Flows Net CF from Operations <Property, Plant, and Equipment Acquired) Cincrease> Decrease in Marketable Securrier Cinvestments Acquired> Other Investment Transactions (1) Not CF from Investing Activities Increase in Short-Team Borrowing Increase in Long-Term Borrowing lesue of Capital Stock Proceeds from Stock Option Exercises <Share Repurchases-Treasury Stock> <Dividend Payments) Other Financing Transactions (1) Net CF from Financing Activities Effects of exchange rate changes on cash Net Change in Cash Cash and Cash Equivalents, Beginning of Year Cash and Cash Equivalents. End of Year L 2010 947 1248 541 550 77 145 106 -33 M -42 -17 -33 -89 123 -422 1 -82 法蓉约发车当新us08-左营80以上 2011 228 36 52 -52 -750 35 -23 1635 -415 -338 -536 -56 -13 -10.20 31 -4 235 104 -286 -556 -390 -28 -608 -1 6 4701 1164 1148 N 德君叹s美出出家当您。台县内隐8878wedg88cago系 -49 0 In Case 10.1, we projected financial statements for Starbucks for Years +1 through +5. In this portion of the Starbucks Integrative Case, we use the projected financial statements from Case 10.1 and apply the techniques learned in this chapter to compute Starbucks' required rate of return on equity and share value based on the free cash flows valuation models. We also compare our value estimate to Starbucks' share price at the time of the case development to provide an investment recommendation. The market equity beta for Starbucks at the end of 2012 is 0.75. Assume that the risk-free interest rate is 3.0% and the market risk premium is 6.0%. Starbucks has 749.3 million shares outstanding at the end of 2012. At the start of Year +1, Starbucks' share price was $50.15. REQUIRED Part I-Computing Starbucks' Share Value Using Free Cash Flows to Common Equity Shareholders a. Use the CAPM to compute the required rate of return on common equity capital for Starbucks. b. Using your projected financial statements from Case 10.1 for Starbucks, begin with pro- jected net cash flows from operations and derive the projected free cash flows for com- mon equity shareholders for Starbucks for Years +1 through +5. You must determine whether your projected changes in cash are necessary for operating liquidity purposes. c. Project the continuing free cash flow for common equity shareholders in Year +6. Assume that the steady-state, long-run growth rate will be 3% in Year +6 and beyond. Project that the Year +5 income statement and balance sheet amounts will grow by 3% in Year +6; then derive the projected statement of cash flows for Year +6. Derive the projected free cash flow for common equity shareholders in Year +6 from the projected statement of cash flows for Year + 6. d. Using the required rate of return on common equity from Requirement a as a dis- count rate, compute the sum of the present value of free cash flows for common eq- uity share holders for Starbucks for Years +1 through +5. e. Using the required rate of return on common equity from Requirement a as a discount rate and the long-run growth rate from Requirement c, compute the continuing value of Starbucks as of the start of Year +6 based on Starbucks' continuing free cash flows for common equity shareholders in Year +6 and beyond. After computing continuing value as of the start of Year +6, discount it to present value at the start of Year +1. f. Compute the value of a share of Starbucks common stock. (1) Compute the total sum of the present value of free cash flows for equity share- holders (from Requirements d and e). (2) Adjust the total sum of the present value using the midyear discounting adjust- ment factor. (3) Compute the per-share value estimate. Note: If you worked Integrative Case 11.1 from Chapter 11 and computed Starbucks' share value using the dividends valuation approach, compare your value estimate from that case with the value estimate you obtain here. They should be the same. Part II-Computing Starbucks' Share Value Using Free Cash Flows to All Debt and Equity Stakeholders g. At the end of 2012, Starbucks had $1,263 million in outstanding interest-bearing short-term and long-term debt on the balance sheet and no preferred stock. Assume, that the balance sheet value of Starbucks' debt equals the market value of the debt. Starbucks faces an interest rate of roughly 6.25% on its outstanding debt. Assume that Starbucks will continue to face the same interest rate on this outstanding debt capital over the remaining life of the debt. Assume that Starbucks will continue to face a 33% income tax rate over the forecast horizon. Compute the weighted-average cost of capital for Starbucks as of the start of Year +1. Compare your computation of Starbucks' weighted-average cost of capital with your estimate of Starbucks' required return on equity from Requirement a. Why do the two amounts differ? h. Based on your projections of Starbucks' financial statements, begin with projected net cash flows from operations and derive the projected free cash flows for all debt and equity stakeholders for Years +1 through +5. Compare your forecasts of Star- bucks' free cash flows for all debt and equity stakeholders Years +1 through +5 with your forecast of Starbucks' free cash flows for equity shareholders in Requirement b. Why are the amounts not identical-what causes the difference each year? 954 CHAPTER 12 Valuation: Cash-Flow-Based Approaches i. Project the continuing free cash flows for all debt and equity stakeholders in Year +6. Use the projected financial statements for Year +6 from Requirement c to derive the projected free cash flows for all debt and equity stakeholders in Year +6. j. Using the weighted average cost of capital from Requirement g as a discount rate, compute the sum of the present value of free cash flows for all debt and equity stakeholders for Starbucks for Years +1 through +5. k. Using the weighted-average cost of capital from Requirement g as a discount rate and the long-run growth rate from Requirement c, compute the continuing value of Star- bucks as of the start of Year +6 based on Starbucks' continuing free cash flows for all debt and equity stakeholders in Year +6 and beyond. After computing continuing value as of the start of Year +6, discount it to present value at the start of Year +1. I. Compute the value of a share of Starbucks common stock. (1) Compute the value of Starbucks' net operating assets using the total sum of the present value of free cash flows for all debt and equity stakeholders (from Requirements j and k). (2) Subtract the value of outstanding debt to obtain the value of equity. (3) Adjust the present value of equity using the midyear discounting adjustment factor. (4) Compute the per-share value estimate. m. Compare your share value estimate from Requirement f with your share value esti- mate from Requirement I. These values should be similar. Part III-Sensitivity Analysis and Recommendation n. Using the free cash flows to common equity shareholders, recompute the value of Starbucks shares under two alternative scenarios. Scenario 1: Assume that Starbucks' long-run growth will be 2%, not 3% as before, and assume that Starbucks' required rate of return on equity is 1 percentage point higher than the rate you computed using the CAPM in Requirement a. Scenario 2: Assume that Starbucks' long-run growth will be 4%, not 3% as before, and assume that Starbucks' required rate of return on equity is 1 percentage point lower than the rate you computed using the CAPM in Requirement a. To quantify the sensitivity of your share value estimate for Starbucks to these variations in growth and discount rates, compare (in percentage terms) your value estimates under these two scenarios with your value estimate from Requirement f. o. At the end of 2012, what reasonable range of share values would you have expected for Starbucks common stock? At that time, where was the market price for Starbucks shares relative to this range? What would you have recommended? p. If you computed Starbucks' common equity share value using the dividends-based valuation approach in Case 11.1, compare the value estimate you obtained in that case with the estimate you obtained in this case. They should be identical. CASE 12.2 Holmes Corporation A 1 Year (Most recent infar right column) 2 BALANCE SHEET DATA 3 Assets: 4 Cach and Cash Equivalents 5 Marketable Securities & Accounts Receivable-Not 7 Inventories 8 Prepaid Expenses and Other Current Assets 9 Deferred Tax Assets-Current 10 Current Assets 11 Long Term Investments 12 Property, Plant & Equipment-at cost 13 <Accumulated Depreciation 14 Amortizable Intangible Azzets (net) 15 Goodvil LT investments 17 Total Assets 18 Liabilter and Equities 19 Accounts Payable-Trade 20 Current Accrued exp 21 insurance res 22 Deferred Rev 20 Current Liabilities 24 Long Term Deb 25 Long Term Accrued Liabilities 26 Total Liabilities 27 20 Common Stock Paid in Capital 29 Retained Earnings (Delick) 20 Accum Other Comprehensive Income (Loss) 31 non controlling interest 32 33 34 Common Shareholders Equity Total Liabiliries and Eques . ************** ******** *55°18 2010 1154 303 543 157 -3472 417 387 966 162 304 230 239 342 372 2757 3796 4201 460 6163 6903 -3808-4244 410 322 107 7362 192 6387 283 414 1779 549 375 2703 146 3471 C 57 2011 2012 1148 903 540 941 D E 398 1134 158 449 510 2076 2210 550 550 340 345 2974 3105 146 41 4297 46 2 1189 848 486 1242 197 3682 4386 386 399 116 8221 140 5046 23 6 5115 6385 7360 8220 F NCOME STATEMENT DATA Revenues (Cost of Goods Sold) Gross Profi store op exp Gen <Amortization of Intangible Assets) <Other Operating Expenses (1) restructuring charges Other Operating Income (1) Operating Profit Interest Income Cinterest Expense) Income before Tax (Income Tax Expense> Net Income (computed) Net Income (enter reported amount as a checkl Comprehensive income SUPPLEMENTAL DATA Statutory Tax Rate Average Tax Rate Impled from Income Statement Dat After-tax Effects of Nonrecuring and Unusual kems o Total Deferred Tax Assets from above) Earnings per Share (basic) G H 947 2010 2011 10707 11700 13300 -4459 -4916 -5813 6248 6784 7487 -3551 -3595 -3918 -570 -749 -601 -510 -523 -550 -293 -393 -430 -53 30 174 1728 50 116 0 148 1419 211 1963 94 -33 2060 -33 -33 1436 1811 -489 -563 -674 947 1248 1386 -2 -3 -1 1 1248 2012 1306 2010 2011 0.34 0.31 0.33 0.3405 0.3109 0.34 0 0 496 337 127 166 0 355 1.83 2012 J STATEMENT OF CASHFLOWS DATA Net Income Add back Depreciation and Amortization Expenses Add back Scook-Based Compensation Expense Deferred Income Taxes Cincome from Equity Affilates, net of Dividends <Increase> Decrease in Accounts Receivable <Increase> Decrease in Inventories Cincrease) Decrease in Other Current lib Increase (Decrease) in Accounts Payable hcrease (Decrease in Deferred rev Other Addbacks to Net Income Other Operating Cash Flows Net CF from Operations <Property, Plant, and Equipment Acquired) Cincrease> Decrease in Marketable Securrier Cinvestments Acquired> Other Investment Transactions (1) Not CF from Investing Activities Increase in Short-Team Borrowing Increase in Long-Term Borrowing lesue of Capital Stock Proceeds from Stock Option Exercises <Share Repurchases-Treasury Stock> <Dividend Payments) Other Financing Transactions (1) Net CF from Financing Activities Effects of exchange rate changes on cash Net Change in Cash Cash and Cash Equivalents, Beginning of Year Cash and Cash Equivalents. End of Year L 2010 947 1248 541 550 77 145 106 -33 M -42 -17 -33 -89 123 -422 1 -82 法蓉约发车当新us08-左营80以上 2011 228 36 52 -52 -750 35 -23 1635 -415 -338 -536 -56 -13 -10.20 31 -4 235 104 -286 -556 -390 -28 -608 -1 6 4701 1164 1148 N 德君叹s美出出家当您。台县内隐8878wedg88cago系 -49 0

Expert Answer:

Related Book For

Financial Reporting Financial Statement Analysis and Valuation a strategic perspective

ISBN: 978-1337614689

9th edition

Authors: James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Posted Date:

Students also viewed these accounting questions

-

In Integrative Case 10.1, we projected financial statements for Walmart Stores for Years +1 through +5. The data in Chapter 12, Exhibits 12.17 through 12.19 include the actual amounts for 2015 and...

-

In Integrative Case 10.1, we projected financial statements for Starbucks for Years +1 through +5. In this portion of the Starbucks Integrative Case, we use the projected financial statements from...

-

In Integrative Case 10.1, we projected financial statements for Walmart Stores, Inc. (Walmart), for Years +1 through +5. In this portion of the Walmart Integrative Case, we use the projected...

-

1-Is it a good business strategy to have a day care center, Harley Davidson Motorcycle Dealership Sales and repair, Namaste Yoga studio, bookstore, temporary worker (day laborer) center, state prison...

-

Abby Landis is the CEO of Pletchers Electronics. Landis is an expert engineer but a novice in accounting. She asks you to explain (1) the bases for comparison in analyzing Pletchers financial...

-

An emergency pump is installed in the pipeline system of Example 4.4 at a distance of 500 m from reservoir A. The pump is used to boost the flow rate when needed. Determine the pressure head the pump...

-

La Salle Exploration Company reported these figures for 2008 and 2007: Compute rate of return on total assets and rate of return on common stockholders' equity for 2008. Do these rates of return...

-

McKnight Exercise Equipment, Inc., reported the following financial statements for 2012: Requirement 1. Compute the amount of McKnight Exercises acquisition of plant assets. McKnight Exercise sold no...

-

How do emergent properties of complex adaptive systems manifest within organizational structures, influencing decision-making processes and strategic outcomes ?

-

You own a flooring company that sells the following items. Product Premium Carpet Basic Carpet Luxury Vinyl Flooring Standard Vinyl Flooring Delivery Fee Installation Price $4.00 / square ft....

-

Thoughts on Validity in research studies?

-

Design a program that calculates the total amount of a meal purchased at a restaurant. The program should ask the user to enter the charge for the food, and then calculate the amount of a 15 percent...

-

Ms. Vigor lives on carrot juice and tofu. In 2000, she bought 1,000 bottles of carrot juice for $2.00 per bottle and 400 pounds of tofu for $3.00 per pound. In 2010, Vigors carrot juice cost $2.50...

-

A case involving Wendys fast-food chain made national headlines when a woman claimed she had found a finger in her bowl of chili. The restaurants became the butt of jokes (some said they served nail...

-

The chapter discusses the positive and negative potential effects of corporate sociopolitical activism (CSA). Whats your feelingshould a company link itself to a social cause, or should it remain...

-

The global airline industry exemplifies many of the concepts and influences we have discussed. Life-Cycle Stage The industry can be described as having some mature characteristics because average...

-

Melbourne Metal is considering becoming a supplier of transmission housings. It would require buying a new forge that would cost $125,000 (including all setup costs) and is expected to last five...

-

Chapter 9 Stock Valuation at Ragan Engines Input area: Shares owned by each sibling Ragan EPS Dividend to each sibling Ragan ROE Ragan required return Blue Ribband Motors Corp. Bon Voyage Marine,...

-

Describe circumstances and give an example of when free cash flows to equity shareholders and free cash flows to all debt and equity stakeholders will be identical. Under those circumstances, will...

-

In Integrative Case 10.1, we projected financial statements for Walmart Stores, Inc. (Walmart), for Years +1 through +5. The data in Chapter 12's Exhibits 12.17, 12.18, and 12.19 include the actual...

-

Selected data for The Hershey Company for Year 1 through Year 3 appear in Exhibit 4.29. REQUIRED a. Compute ROA and its decomposition for Year 2 and Year 3. Assume a tax rate of 35%.b. Compute ROCE...

-

Suggest a general outline marketing planning strategy for 12 months ahead for Graham Keddie.

-

What part should the sales function play when drawing up a detailed 12 months operational marketing plan for EMA?

-

Explain the differences between marketing strategies and sales strategies.

Study smarter with the SolutionInn App