Question: Intro Suppose that the excess return for all securities can be described by a single index model: Ri = ai + BiRm + ej The

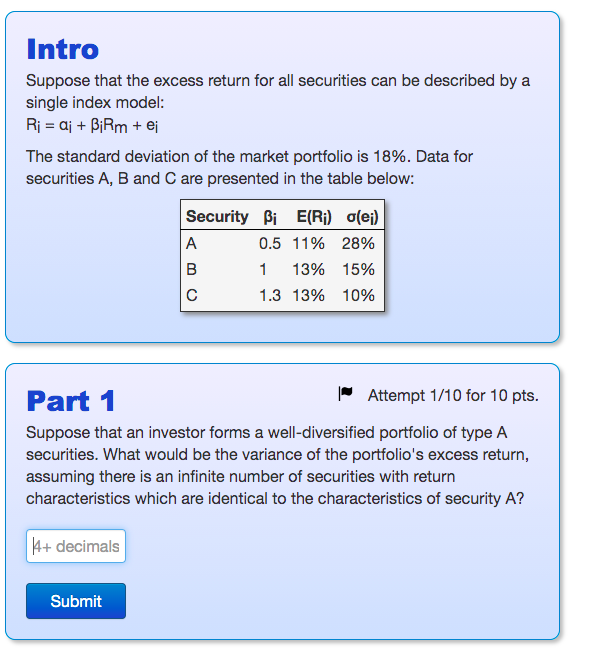

Intro Suppose that the excess return for all securities can be described by a single index model: Ri = ai + BiRm + ej The standard deviation of the market portfolio is 18%. Data for securities A, B and C are presented in the table below: Security Bi E(Ri) o(ei) A 0.5 11% 28% B 1 13% 15% 1.3 13% 10% Part 1 | Attempt 1/10 for 10 pts. Suppose that an investor forms a well-diversified portfolio of type A securities. What would be the variance of the portfolio's excess return, assuming there is an infinite number of securities with return characteristics which are identical to the characteristics of security A? 14+ decimals Submit Intro Suppose that the excess return for all securities can be described by a single index model: Ri = ai + BiRm + ej The standard deviation of the market portfolio is 18%. Data for securities A, B and C are presented in the table below: Security Bi E(Ri) o(ei) A 0.5 11% 28% B 1 13% 15% 1.3 13% 10% Part 1 | Attempt 1/10 for 10 pts. Suppose that an investor forms a well-diversified portfolio of type A securities. What would be the variance of the portfolio's excess return, assuming there is an infinite number of securities with return characteristics which are identical to the characteristics of security A? 14+ decimals Submit

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts