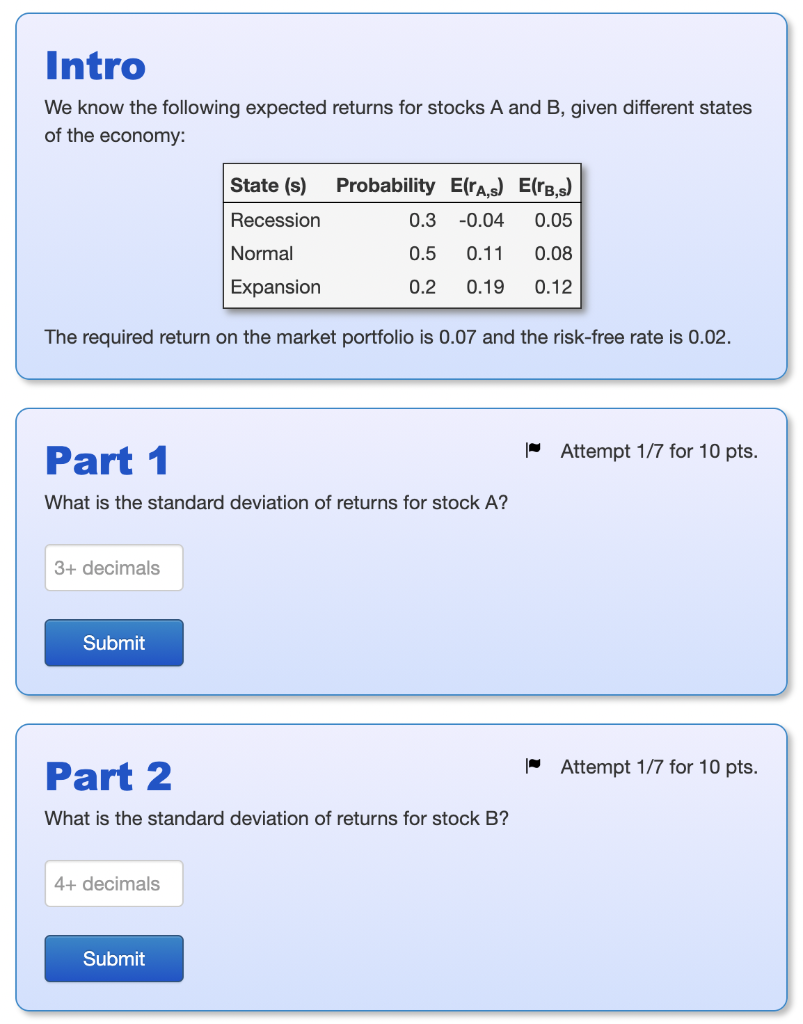

Question: Intro We know the following expected returns for stocks A and B, given different states of the economy: State (s) Recession Probability E(ra,s) E(rs,s) 0.3

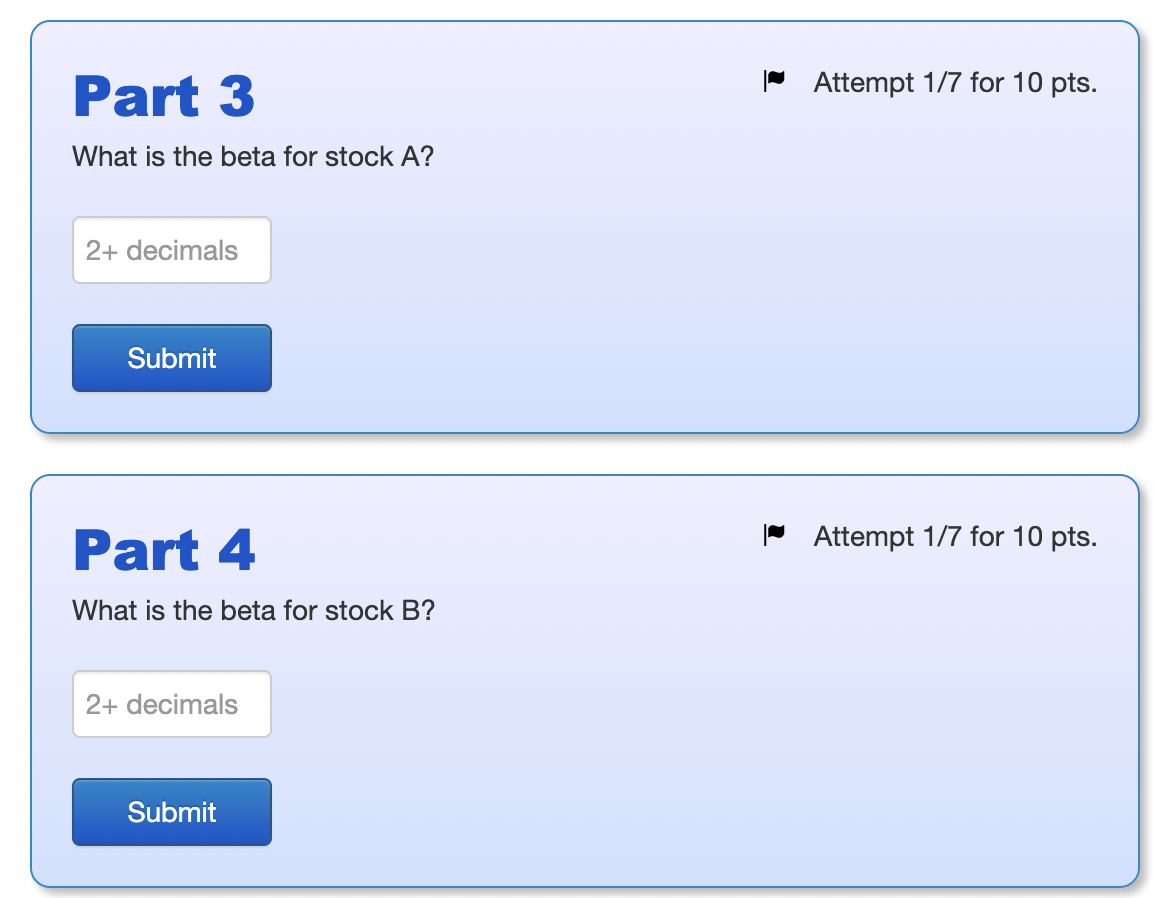

Intro We know the following expected returns for stocks A and B, given different states of the economy: State (s) Recession Probability E(ra,s) E(rs,s) 0.3 -0.04 0.05 0.5 0.11 0.08 Normal Expansion 0.2 0.19 0.12 The required return on the market portfolio is 0.07 and the risk-free rate is 0.02. Part 1 | Attempt 1/7 for 10 pts. What is the standard deviation of returns for stock A? 3+ decimals Submit Part 2 Attempt 1/7 for 10 pts. What is the standard deviation of returns for stock B? 4+ decimals Submit Part 3 Attempt 1/7 for 10 pts. What is the beta for stock A? 2+ decimals Submit Part 4 Attempt 1/7 for 10 pts. What is the beta for stock B? 2+ decimals Submit

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts