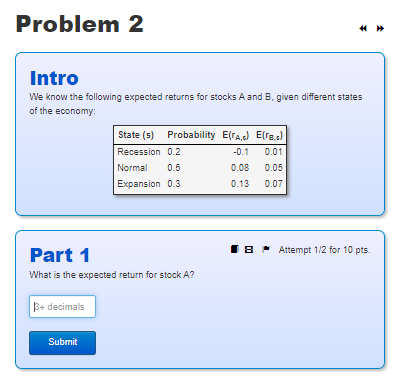

Question: Problem 2 H H Intro We know the following expected returns for stocks A and B, given different states of the economy: State (s] Probability

![(s] Probability E(rA,) E( B..) Recession 0.2 0.1 0.01 Normal 0.5 0.08](https://s3.amazonaws.com/si.experts.images/answers/2024/07/6682ccfa8e15b_1866682ccfa80adf.jpg)

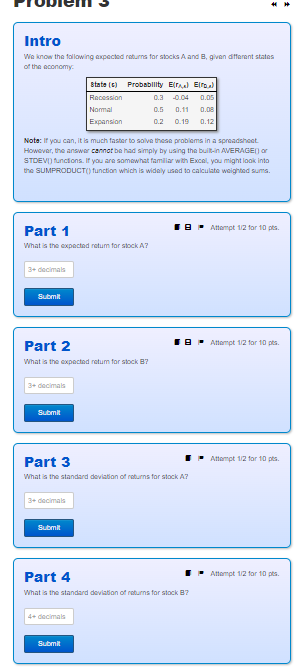

Problem 2 H H Intro We know the following expected returns for stocks A and B, given different states of the economy: State (s] Probability E(rA,) E( B..) Recession 0.2 0.1 0.01 Normal 0.5 0.08 0.05 Expansion 0.3 0.13 0.07 Part 1 1 8 Attempt 1/2 for 10 pts. What is the expected return for stock A? 3+ decimals SubmitProblem 1 Intro An investment costs $80 and offers a payoff of $100 with probability p and 0 with probability 1-p. Time-equivalent Treasuries offer an interest rate of 4%. Assume risk neutrality, Le. the expected return on any security of the same time duration should be the same regardless of how risky the payoff is. Part 1 Attempt 1/2 for 10 pts. What is the promised return of the investment? 3+ decimals Submit Part 2 Attempt 1/2 for 10 pts. What is the probability of default? 2+ decimals SubmitProblem 4 Intro A stock has a beta of 1.2. The risk-free rate is 4%. Assume that the CAPM holds. Part 1 1 8 Attempt 212 for 5 pts. What is the cupacted retum for the stock if the cupscind ralum on the market is 3+ decimals Submit Part 2 1 8 Attempt 12 for 10 pts. What is the cupacted retum for the stock if the expected market risk premium b 3+ decimal SubmitTODICI Intro We know the following expected returns for stocks A and B, given diffamant stains of the aconomy. atute [c) Probability Er) Elroad Recession -0.04 10.05 Normal 0. 11 0.0B Expansion 0.2 0.19 0.12 Note: If you can, it is much faster to solve these problems in a spreadsheet However, the answer cannot be had simply by using the built-in AVERAGED or STDEVI] funcions. If you are somewhat familiar with Excel, you might look into the SUMPRODUCT() function which is widely used to calculate weighted sums. Part 1 1 8 Attempt 12 for 10 pts. What is the cupacted retum for stock A7 3+ decimals Submit Part 2 1 8 Attempt 12 for 10 pts. What is the expected retum for stock 87 3+ decimals Submit Part 3 P Attempt 12 for 10 pts. What is the standard deviation of returns for stock AT 3+ decimals Submit Part 4 I P Attempt 12 for 10 pts. What is the standard deviation of returns for stock 87 4+ decimals Submit

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts