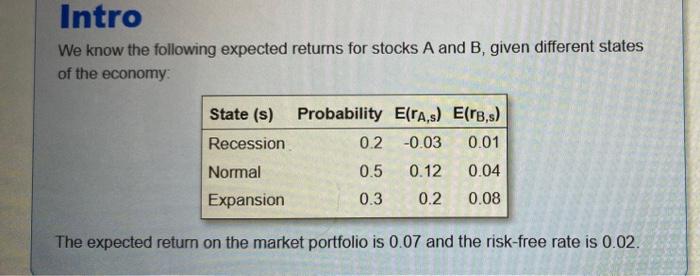

Question: Intro We know the following expected returns for stocks A and B, given different states of the economy Probability E(TA.s) E(TB,s) 0.2 -0.03 0.01 State

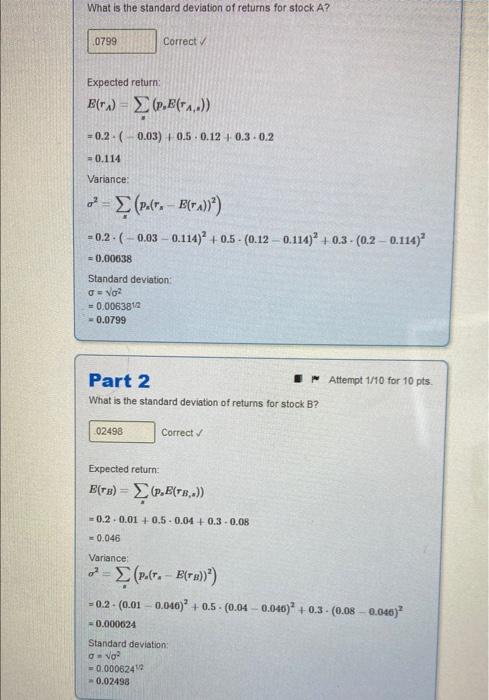

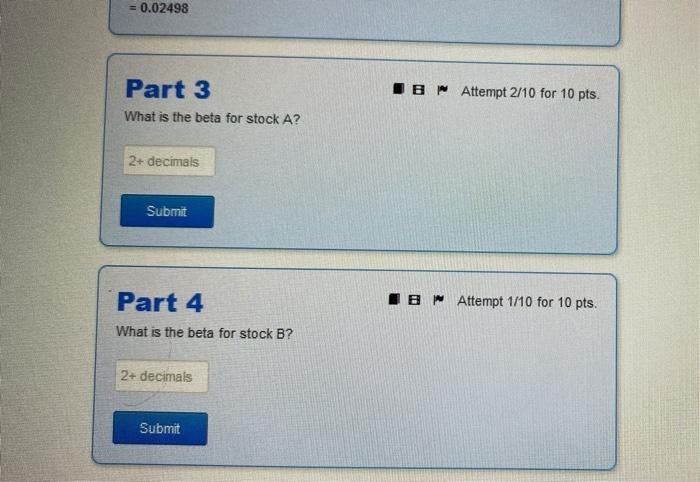

Intro We know the following expected returns for stocks A and B, given different states of the economy Probability E(TA.s) E(TB,s) 0.2 -0.03 0.01 State (s) Recession Normal Expansion 0.5 0.12 0.04 0.3 0.2 0.08 The expected return on the market portfolio is 0.07 and the risk-free rate is 0.02. What is the standard deviation of returns for stock A? 0799 Correct Expected return (ru) (.(TA..) =0.2 ( 0.03) +0.5.0.12 0.3.0.2 = 0.114 Variance: o? (par. E(v.))) =0.2.( -0.03 -0.114)2 +0.5 - (0.12 -0.114)" +0.3 - (0.2 - 0.114) = 0.00038 Standard deviation: = Vol = 0.0063812 -0.0799 Attempt 1/10 for 10 pts Part 2 What is the standard deviation of returns for stock B? 02498 Correct Expected return E(FE) = P.E[ts,.)) 0.2 -0.01 +0.5 -0.04 +0.3 -0.08 = 0.046 Variance o? (pol. Etru)") = 0.2-0.01 -0.040) + 0.5 - (0.04 -0.048)+0.3 - (0.08 -0.046) = 0.000024 Standard deviation: ovo = 0.00062412 0.02498 = 0.02498 IS Attempt 2/10 for 10 pts. Part 3 What is the beta for stock A? 2+ decimals Submit Part 4 IB Attempt 1/10 for 10 pts. What is the beta for stock B? 2+ decimals Submit

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts