Question: Let M = (B, S) be a generic complete and arbitrage-free model where B is the money market account and S is the stock

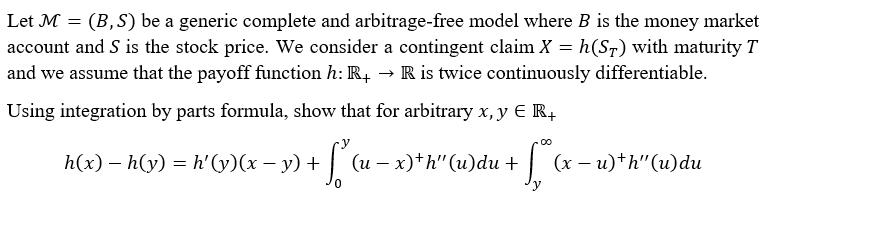

Let M = (B, S) be a generic complete and arbitrage-free model where B is the money market account and S is the stock price. We consider a contingent claim X = h(ST) with maturity T and we assume that the payoff function h: R+ R is twice continuously differentiable. Using integration by parts formula, show that for arbitrary x, y E R+ h(x) h(y) = h'(y)(x y) + f ( - -00 (u-x)+h" (u)du + S (x-u)+h" (u) du

Step by Step Solution

3.37 Rating (153 Votes )

There are 3 Steps involved in it

To prove the given equation using integration by parts well start with the integration by parts form... View full answer

Get step-by-step solutions from verified subject matter experts