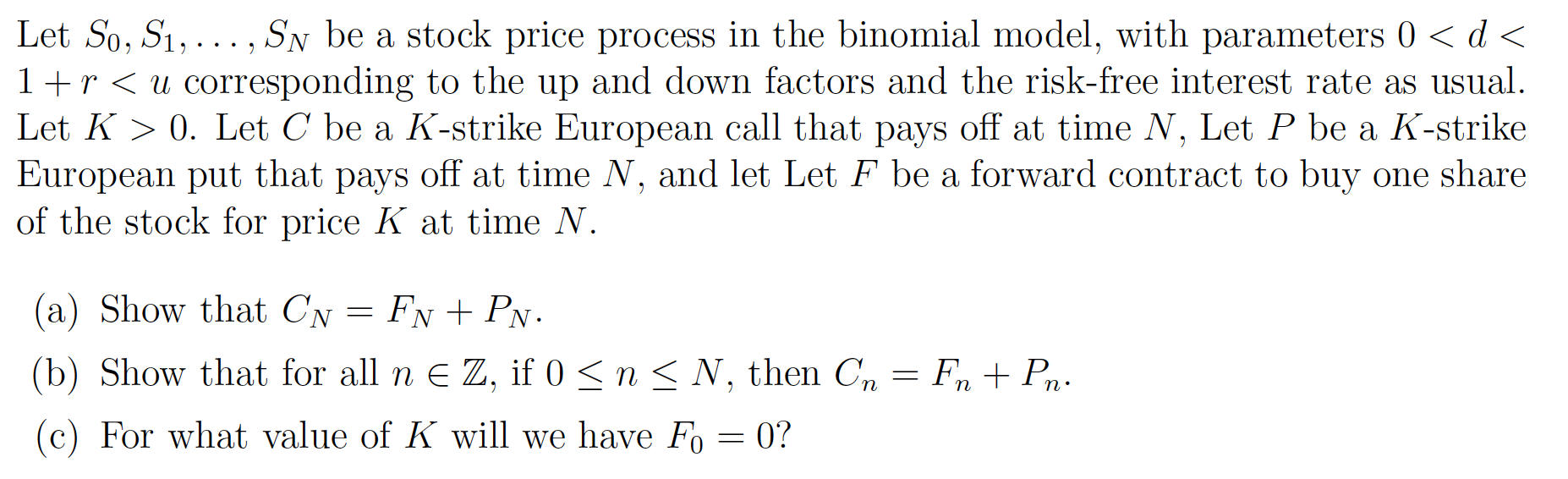

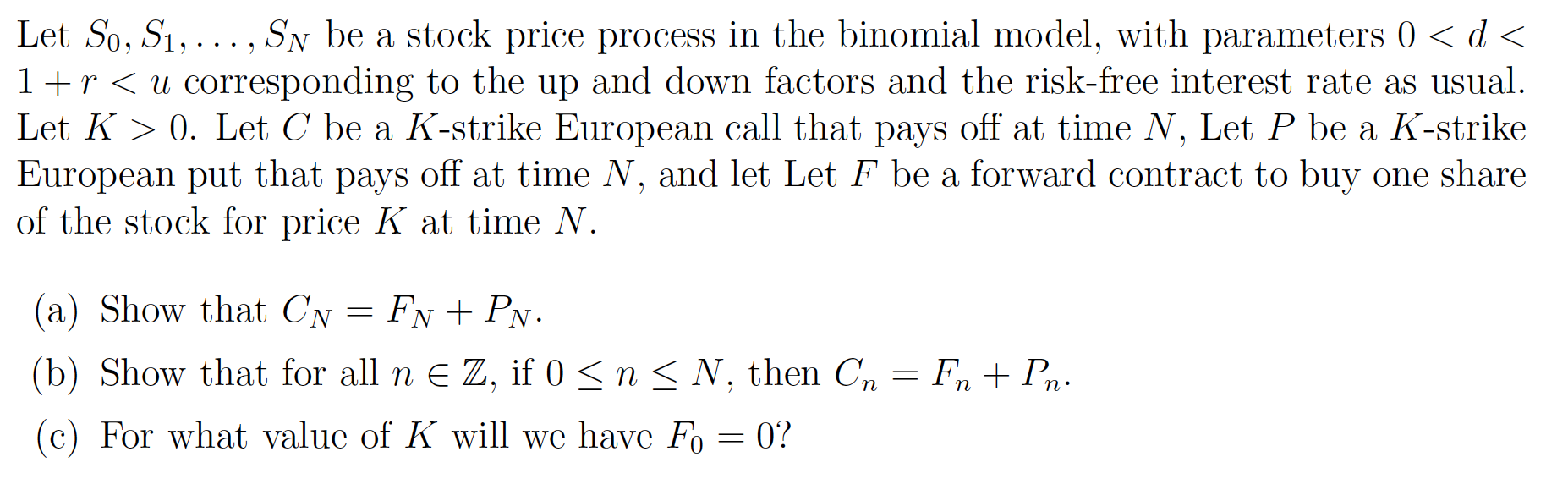

Question: Let So, 81, . . . , SN be a stock price process in the binomial model, with parameters 0 0. Let C be a

Let So, 81, . . . , SN be a stock price process in the binomial model, with parameters 0 0. Let C be a K strike European call that pays off at time N , Let P be a K strike European put that pays off at time N , and let Let F be a forward contract to buy one share of the stock for price K at time N. (a) Show that ON 2 FN + PN. (b) Show that for all n E Z, if 0 S n g N, then On : Fn + P". (c) For what value of K will we have F0 : 0

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock