Question: Let us consider an 18-month basis swap that makes payments semiannually. Assume the notional principal is $100,000,000. The accrual period is = 180/360. a. What

Let us consider an 18-month basis swap that makes payments semiannually. Assume the notional principal is $100,000,000. The accrual period is = 180/360.

- a. What is its basis spread given the information below?

- b. What is the swap value at the outset of the swap?

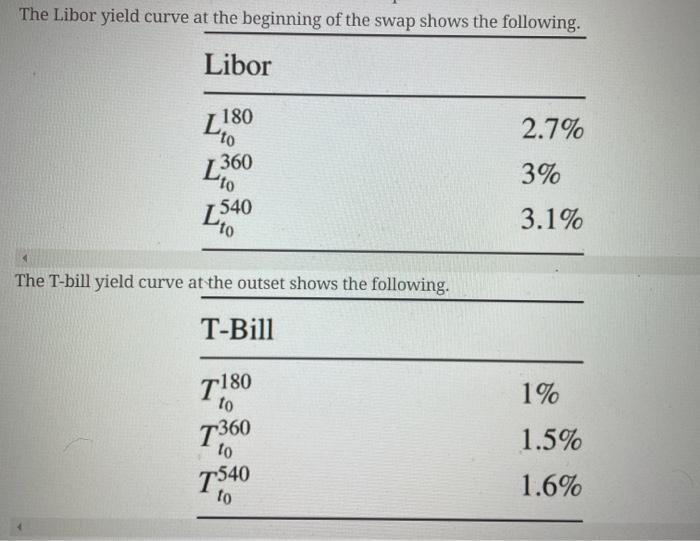

The Libor yield curve at the beginning of the swap shows the following.

The T-bill yield curve at the outset shows the following.

The Libor yield curve at the beginning of the swap shows the following. Libor 180 to 2.7% 360 LIO 3% 2540 3.1% The T-bill yield curve at the outset shows the following. T-Bill 7180 1% to T360 1.5% to T540 1.6% to The Libor yield curve at the beginning of the swap shows the following. Libor 180 to 2.7% 360 LIO 3% 2540 3.1% The T-bill yield curve at the outset shows the following. T-Bill 7180 1% to T360 1.5% to T540 1.6% to

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts