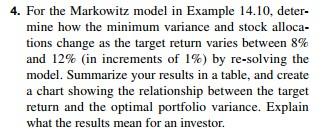

Question: Markowitz Portfolio Model Data Target Return Min. Variance Stock 1 Stock 2 Stock 3 Expected Variance-Covariance Matrix 8% 0.004 0.28 0.03 0.69 Return Stock 1

| Markowitz Portfolio Model | |||||||||||||

| Data | Target Return | Min. Variance | Stock 1 | Stock 2 | Stock 3 | ||||||||

| Expected | Variance-Covariance Matrix | 8% | 0.004 | 0.28 | 0.03 | 0.69 | |||||||

| Return | Stock 1 | Stock 2 | Stock 3 | 9% | 0.007 | 0.27 | 0.24 | 0.49 | |||||

| Stock 1 | 10% | Stock 1 | 0.025 | 0.015 | -0.002 | 10% | 0.012 | 0.25 | 0.45 | 0.3 | |||

| Stock 2 | 12% | Stock 2 | 0.03 | 0.005 | 11% | 0.02 | 0.24 | 0.66 | 0.11 | ||||

| Stock 3 | 7% | Stock 3 | 0.004 | 12% | 0.03 | 0.00 | 1.00 | 0.00 | |||||

| Target Return | 10% | ||||||||||||

| | |||||||||||||

| Model | |||||||||||||

| Variance Calculations | |||||||||||||

| Allocation | Squared Terms | Cross-Products | |||||||||||

| Stock 1 | 0.25 | 0.001579256 | 0.003387 | ||||||||||

| Stock 2 | 0.45 | 0.006053362 | -0.000301067 | ||||||||||

| Stock 3 | 0.30 | 0.000358718 | 0.001345191 | ||||||||||

| Total | 1 | ||||||||||||

| Return | Variance | ||||||||||||

| Portfolio | 10.0% | 0.012 | |||||||||||

4. For the Markowitz model in Example 14.10, deter- mine how the minimum variance and stock alloca- tions change as the target return varies between 8% and 12% (in increments of 1%) by re-solving the model. Summarize your results in a table, and create a chart showing the relationship between the target return and the optimal portfolio variance. Explain what the results mean for an investor. 4. For the Markowitz model in Example 14.10, deter- mine how the minimum variance and stock alloca- tions change as the target return varies between 8% and 12% (in increments of 1%) by re-solving the model. Summarize your results in a table, and create a chart showing the relationship between the target return and the optimal portfolio variance. Explain what the results mean for an investor

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts