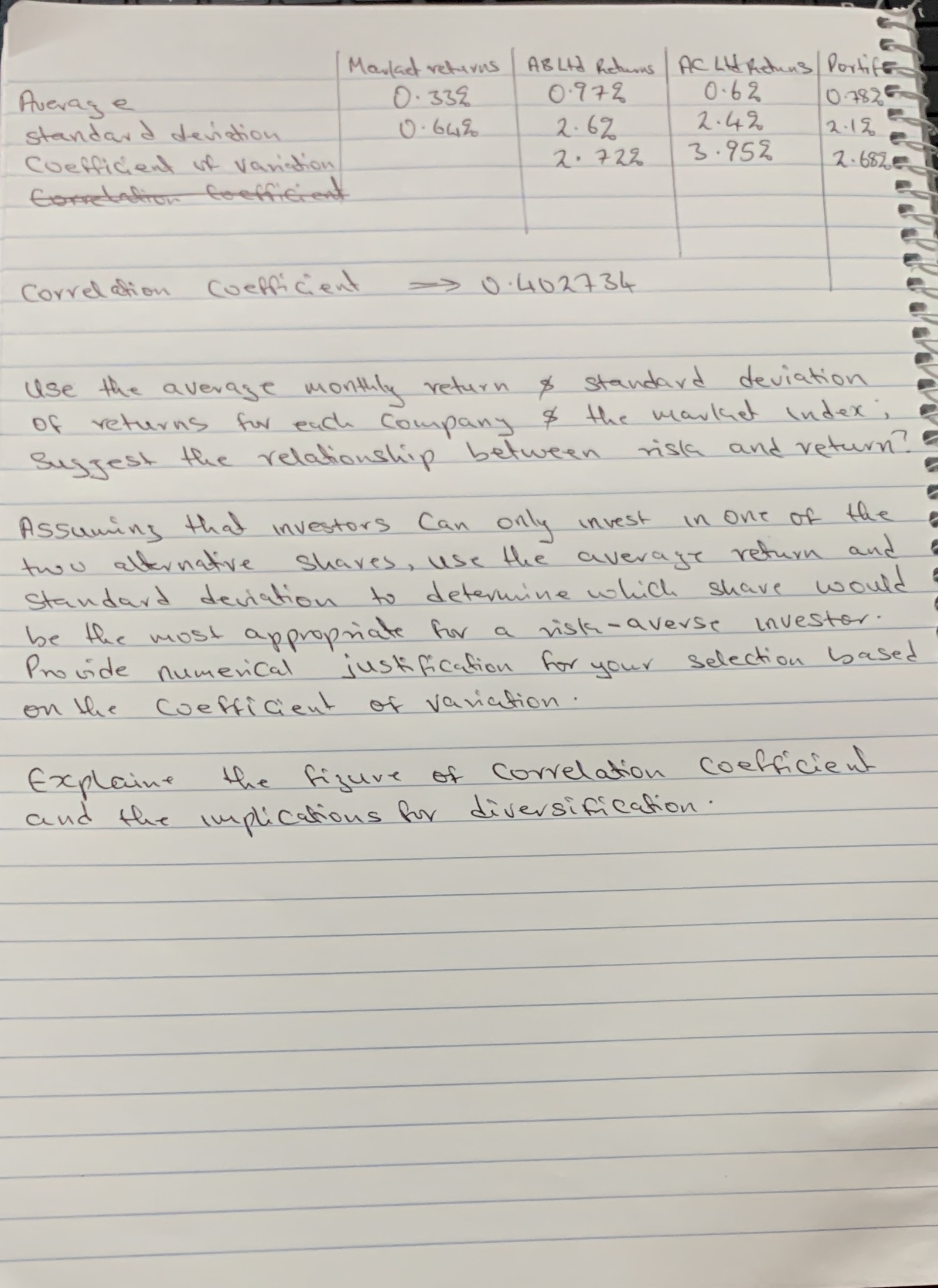

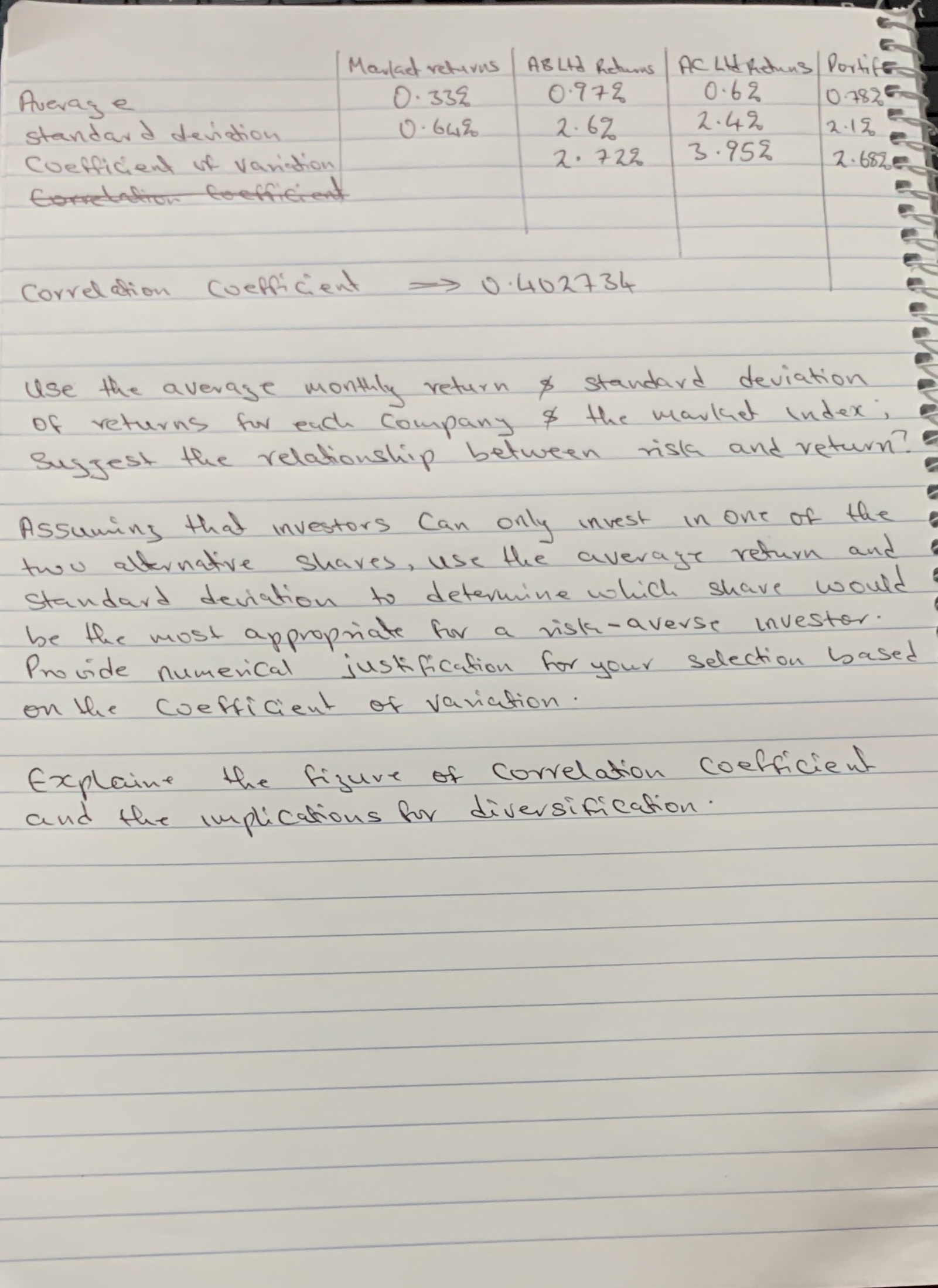

Question: Marlast returns ABLAd Returns Average 0. 338 0. 97% ACLU Richens Portife 0.6% 0782 standard deviation 2. 6% 2. 4% Coefficient of variation 3. 95%

Marlast returns ABLAd Returns Average 0. 338 0. 97% ACLU Richens Portife 0.6% 0782 standard deviation 2. 6% 2. 4% Coefficient of variation 3. 95% 2. 1% 2 . 72% Correlation coefficient Correlation coefficient => 0.402734 Use the average monthly return standard deviation of returns for each company $ the market index " Suggest the relationship between risk and return? Assuming that investors Can only invest in one of the two alternative shares , use the average return and standard deviation to determine which shave would be the most appropriate for a risk-averse investor . Provide numerical justification for your selection based on the Coefficient of variation . Explain the figure of Correlation coefficient and the implications for diversification

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts