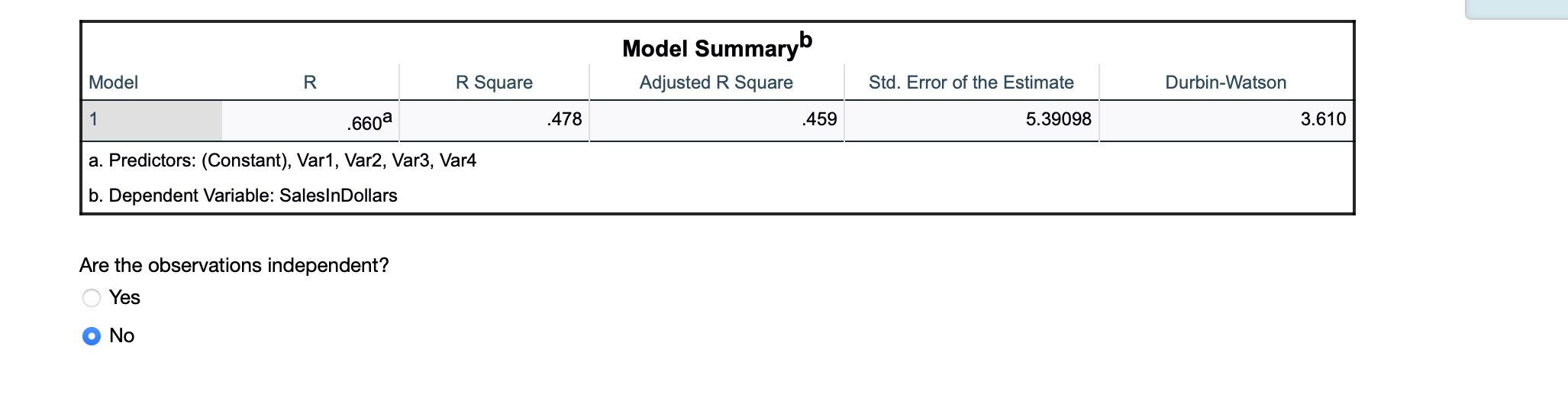

Question: Model Summaryb Adjusted R Square Model R R Square Std. Error of the Estimate Durbin-Watson 1 .6608 .478 459 5.39098 3.610 a. Predictors: (Constant), Var1,

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock