Question: Need a full explanation on this question please. Step by Step please Question 8 Estimate the percentage change in price of a bond using the

Need a full explanation on this question please. Step by Step please

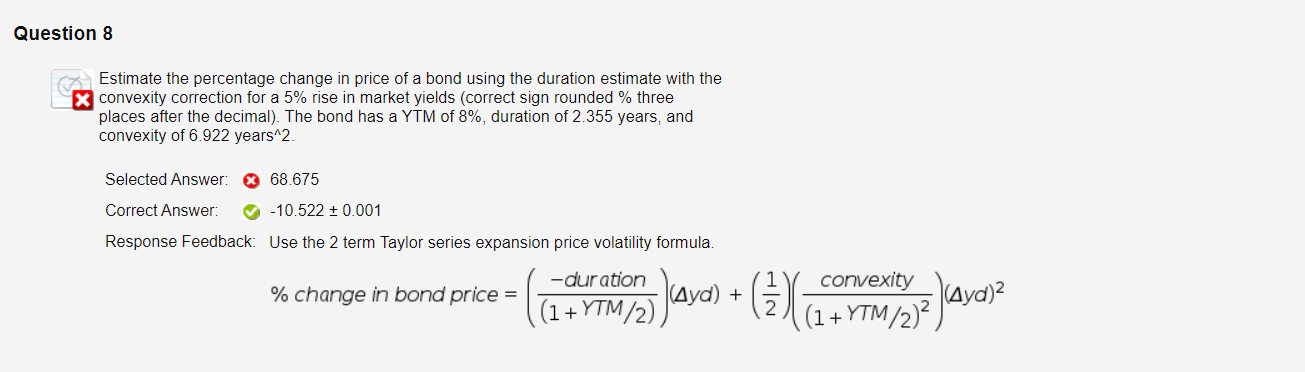

Question 8 Estimate the percentage change in price of a bond using the duration estimate with the convexity correction for a 5% rise in market yields (correct sign rounded % three places after the decimal). The bond has a YTM of 8%, duration of 2.355 years, and convexity of 6.922 years^2 Selected Answer: X 68.675 Correct Answer: ~ -10.522 +0.001 Response Feedback: Use the 2 term Taylor series expansion price volatility formula -duration convexity % change in bond price = (Ayd) + (1 + YTM/2) + ? (1) 44YTM/23 Ayd)2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock