Question: need equations too not just answers please. just answer part 1-4 Question 3. The popular Carry Trade (Covered Interest Arbitrage) between the USD and MXN

need equations too not just answers please. just answer part 1-4

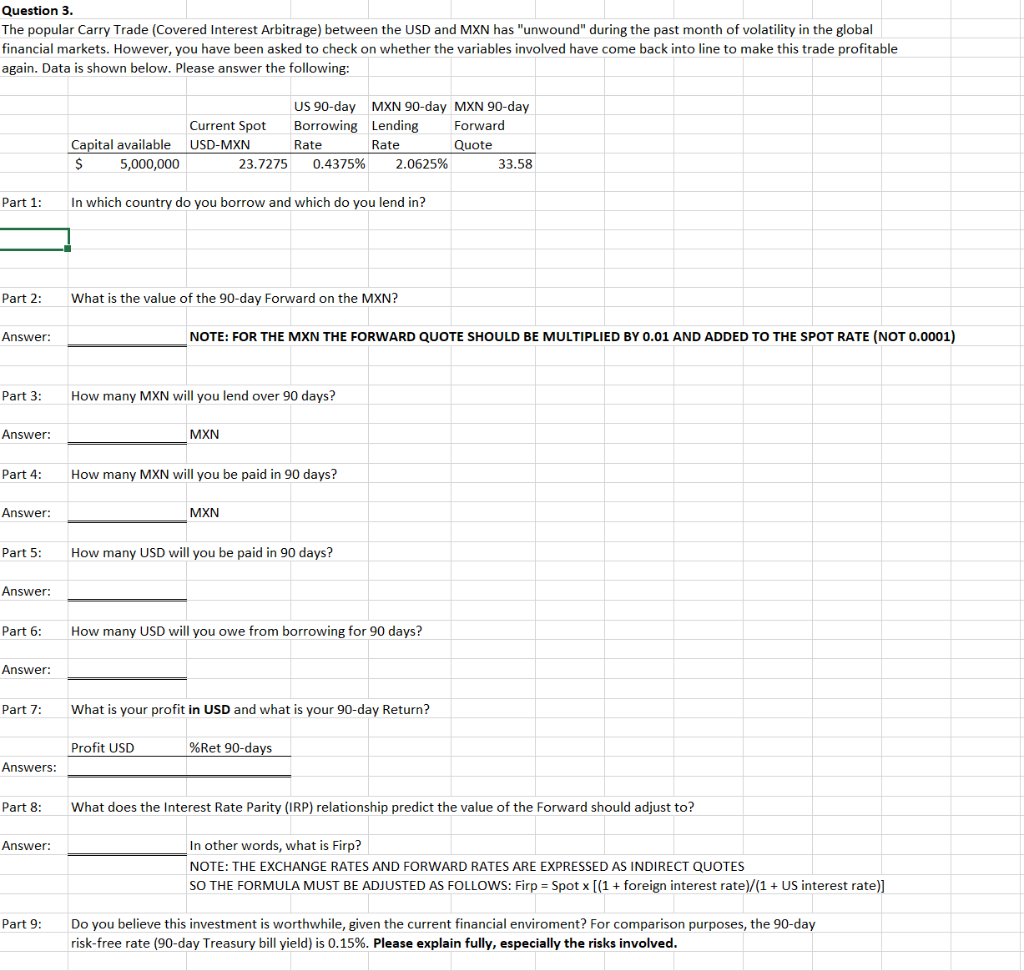

Question 3. The popular Carry Trade (Covered Interest Arbitrage) between the USD and MXN has "unwound" during the past month of volatility in the global financial markets. However, you have been asked to check on whether the variables involved have come back into line to make this trade profitable again. Data is shown below. Please answer the following: US 90-day MXN 90-day MXN 90-day Current Spot Borrowing Lending Forward USD-MXN Rate Rate Quote 23.7275 0.4375% 2.0625% 33.58 Capital available $ 5,000,000 Part 1: In which country do you borrow and which do you lend in? Part 2: What is the value of the 90-day Forward on the MXN? Answer: NOTE: FOR THE MXN THE FORWARD QUOTE SHOULD BE MULTIPLIED BY 0.01 AND ADDED TO THE SPOT RATE (NOT 0.0001) Part 3: How many MXN will you lend over 90 days? Answer: MXN Part 4: How many MXN will you be paid in 90 days? Answer: MXN Part 5: How many USD will you be paid in 90 days? Answer: Part 6: How many USD will you owe from borrowing for 90 days? Answer: Part 7: What is your profit in USD and what is your 90-day Return? Profit USD %Ret 90-days Answers: Part 8: What does the Interest Rate Parity (IRP) relationship predict the value of the Forward should adjust to? Answer: In other words, what is Firp? NOTE: THE EXCHANGE RATES AND FORWARD RATES ARE EXPRESSED AS INDIRECT QUOTES SO THE FORMULA MUST BE ADJUSTED AS FOLLOWS: Firp = Spot x [(1 + foreign interest rate)/(1 + US interest rate)] Part 9: Do you believe this investment is worthwhile, given the current financial enviroment? For comparison purposes, the 90-day risk-free rate (90-day Treasury bill yield) is 0.15%. Please explain fully, especially the risks involved. Question 3. The popular Carry Trade (Covered Interest Arbitrage) between the USD and MXN has "unwound" during the past month of volatility in the global financial markets. However, you have been asked to check on whether the variables involved have come back into line to make this trade profitable again. Data is shown below. Please answer the following: US 90-day MXN 90-day MXN 90-day Current Spot Borrowing Lending Forward USD-MXN Rate Rate Quote 23.7275 0.4375% 2.0625% 33.58 Capital available $ 5,000,000 Part 1: In which country do you borrow and which do you lend in? Part 2: What is the value of the 90-day Forward on the MXN? Answer: NOTE: FOR THE MXN THE FORWARD QUOTE SHOULD BE MULTIPLIED BY 0.01 AND ADDED TO THE SPOT RATE (NOT 0.0001) Part 3: How many MXN will you lend over 90 days? Answer: MXN Part 4: How many MXN will you be paid in 90 days? Answer: MXN Part 5: How many USD will you be paid in 90 days? Answer: Part 6: How many USD will you owe from borrowing for 90 days? Answer: Part 7: What is your profit in USD and what is your 90-day Return? Profit USD %Ret 90-days Answers: Part 8: What does the Interest Rate Parity (IRP) relationship predict the value of the Forward should adjust to? Answer: In other words, what is Firp? NOTE: THE EXCHANGE RATES AND FORWARD RATES ARE EXPRESSED AS INDIRECT QUOTES SO THE FORMULA MUST BE ADJUSTED AS FOLLOWS: Firp = Spot x [(1 + foreign interest rate)/(1 + US interest rate)] Part 9: Do you believe this investment is worthwhile, given the current financial enviroment? For comparison purposes, the 90-day risk-free rate (90-day Treasury bill yield) is 0.15%. Please explain fully, especially the risks involved

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts