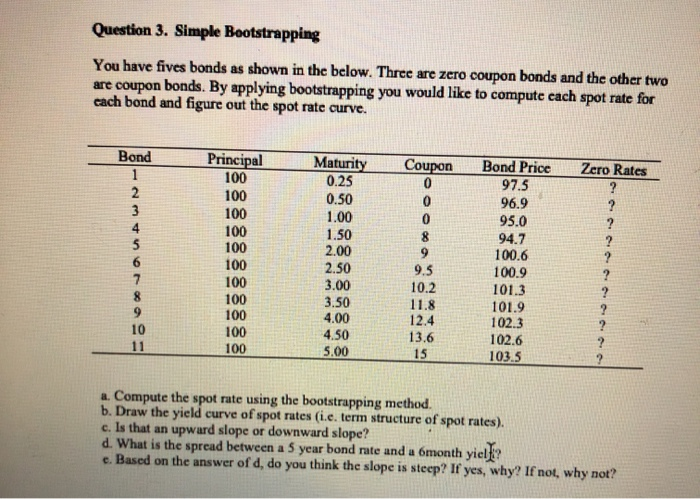

Question: need help. show work on excel this is a I got! Question 3. Simple Bootstrapping You have fives bonds as shown in the below. Three

Question 3. Simple Bootstrapping You have fives bonds as shown in the below. Three are zero coupon bonds and the other two are coupon bonds. By applying bootstrapping you would like to compute cach spot rate for cach bond and figure out the spot rate curve. Bond Coupon Zero Rates Principal 100 100 Maturity 0.25 0.50 1.00 van AWN- 1.50 2.00 Bond Price 97.5 96.9 95.0 94.7 100.6 100.9 101.3 101.9 102.3 102.6 103.5 a. Compute the spot rate using the bootstrapping method. b. Draw the yield curve of spot rates (i.e. term structure of spot rates). c. Is that an upward slope or downward slope? d. What is the spread between a 5 year bond rate and a 6month yielf? e. Based on the answer of d, do you think the slope is steep? If yes, why? If not, why not

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts