Question: Note: answer required in 30 mnts please help universitt Discounted Cash Flows, Duration and Convexingsbri Example: What is the duration of a coupon bond with

Note: answer required in 30 mnts please help

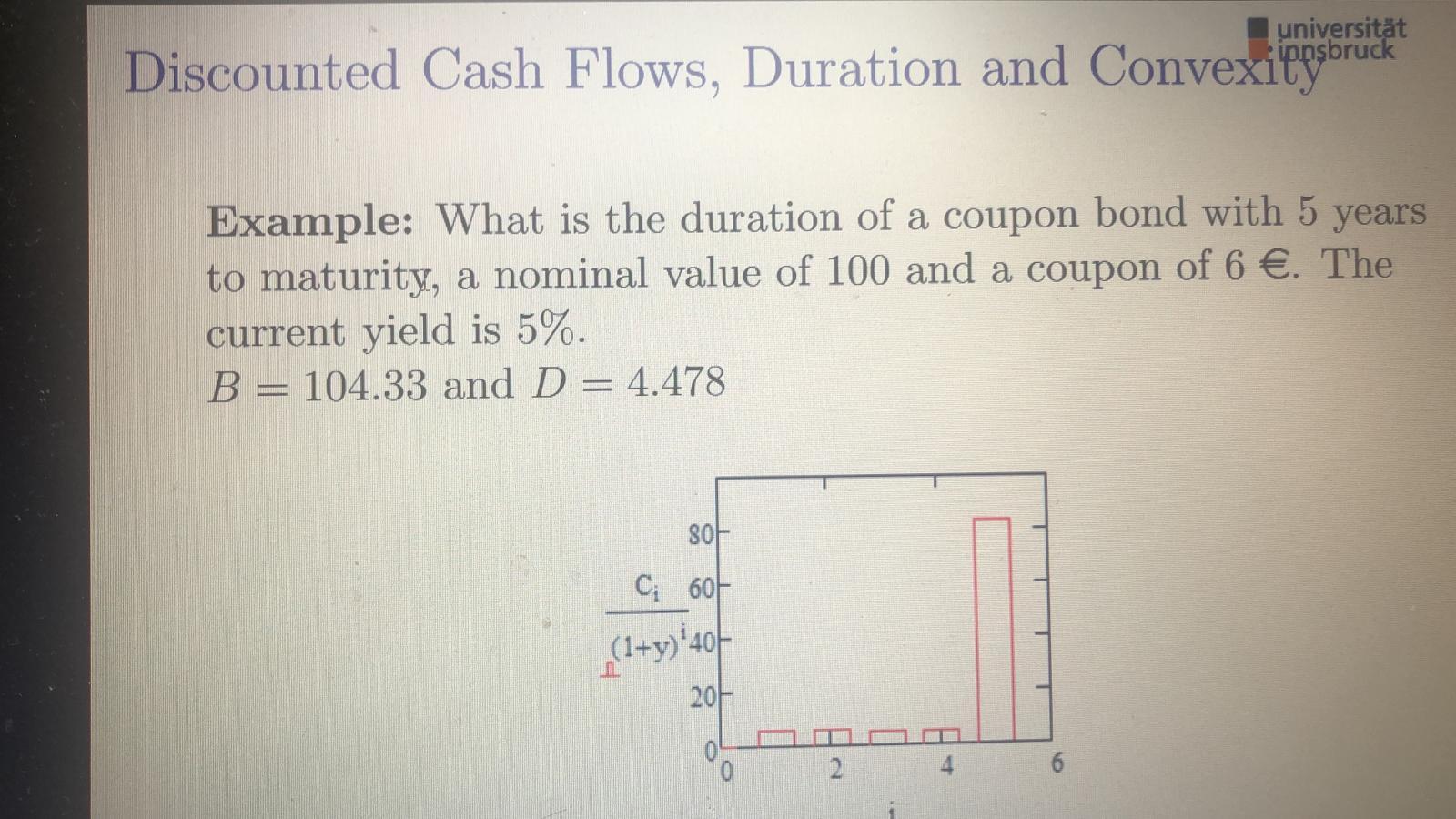

universitt Discounted Cash Flows, Duration and Convexingsbri Example: What is the duration of a coupon bond with 5 years to maturity, a nominal value of 100 and a coupon of 6 . The current yield is 5%. B = 104.33 and D = 4.478 80F C; 60% (1+y)'401 20F 2. 4. 6

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock