Question: nstruction: 1. Show your calculation steps sufficiently clear. 2. Round your answers with 4 decimals. 2. The binomial tree below shows the logarithmic short-term rate

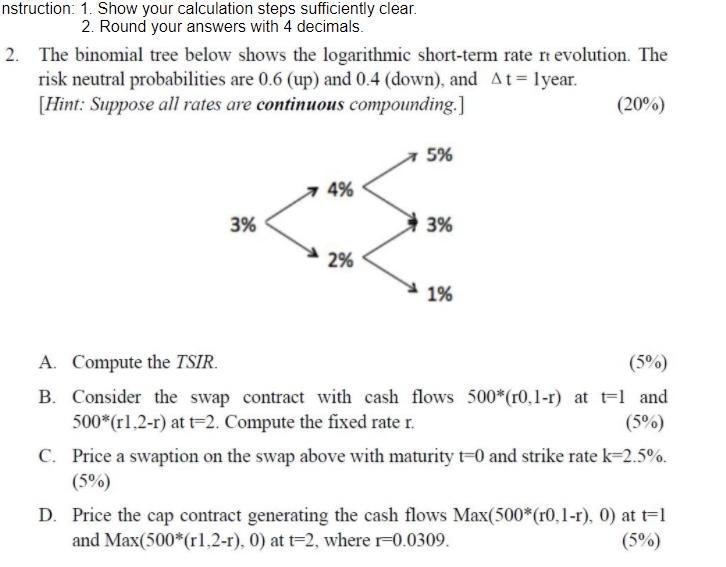

nstruction: 1. Show your calculation steps sufficiently clear. 2. Round your answers with 4 decimals. 2. The binomial tree below shows the logarithmic short-term rate rt evolution. The risk neutral probabilities are 0.6 (up) and 0.4 (down), and At= lyear. [Hint: Suppose all rates are continuous compounding.) (20) 5% 4% 3% 3% 2% 1% A. Compute the TSIR. (59) B. Consider the swap contract with cash flows 500*(10.1-r) at El and 500*(r1.2-r) at F2. Compute the fixed rate r. (5) C. Price a swaption on the swap above with maturity t=0 and strike rate k=2.5%. (5%) D. Price the cap contract generating the cash flows Max(500*(r0.1-r), 0) at tl and Max(500*(r1,2-r), 0) at =2, where r=0.0309. (5%) nstruction: 1. Show your calculation steps sufficiently clear. 2. Round your answers with 4 decimals. 2. The binomial tree below shows the logarithmic short-term rate rt evolution. The risk neutral probabilities are 0.6 (up) and 0.4 (down), and At= lyear. [Hint: Suppose all rates are continuous compounding.) (20) 5% 4% 3% 3% 2% 1% A. Compute the TSIR. (59) B. Consider the swap contract with cash flows 500*(10.1-r) at El and 500*(r1.2-r) at F2. Compute the fixed rate r. (5) C. Price a swaption on the swap above with maturity t=0 and strike rate k=2.5%. (5%) D. Price the cap contract generating the cash flows Max(500*(r0.1-r), 0) at tl and Max(500*(r1,2-r), 0) at =2, where r=0.0309. (5%)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts