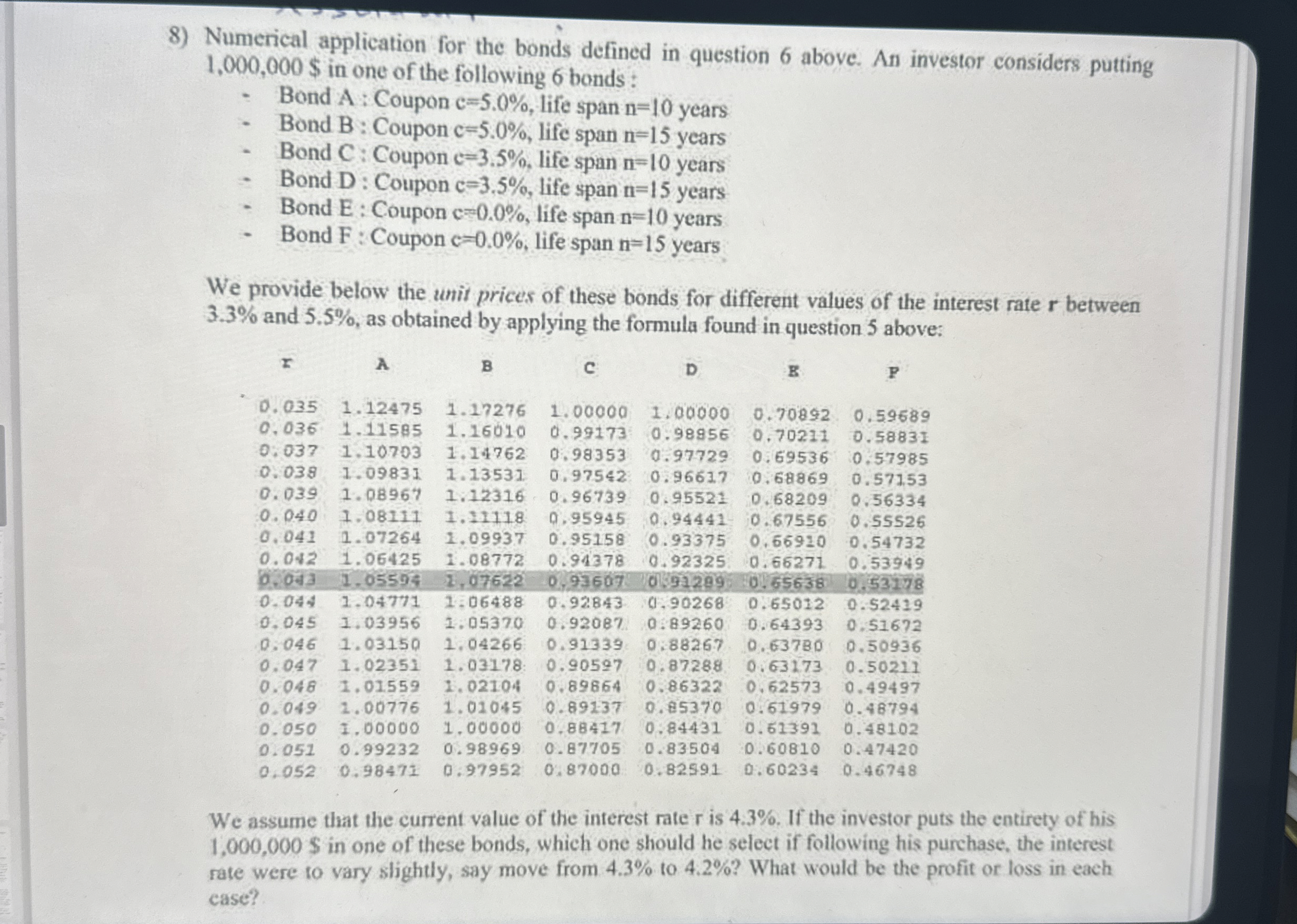

Question: Numerical application for the bonds defined in question 6 above. An investor considers putting 1 , 0 0 0 , 0 0 0 $ in

Numerical application for the bonds defined in question above. An investor considers putting $ in one of the following bonds :

Bond A: Coupon life span years

Bond B: Coupon life span years

Bond C: Coupon life span years

Bond D : Coupon life span years

Bond : Coupon life span years

Bond : Coupon life span years

We provide below the unit prices of these bonds for different values of the interest rate between and as obtained by applying the formula found in question above:

tableBCDBP

We assume that the current value of the interest rate r is If the investor puts the entirety of his $ in one of these bonds, which one should he select if following his purchase, the interest rate were to vary slightly, say move from to What would be the profit or loss in each case?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock