Question: Only qesution 25 please A pension fund manager is considering two mutual funds: a stock fund, and a bond fund. The probability distribution of the

Only qesution 25 please

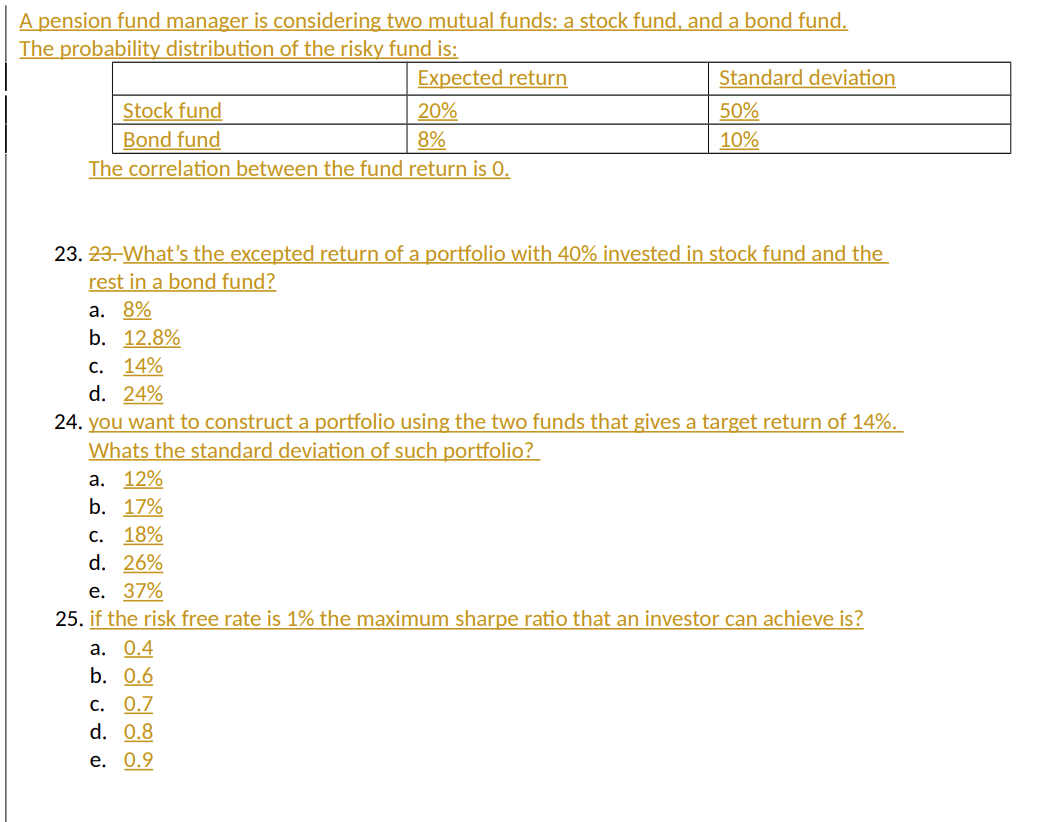

A pension fund manager is considering two mutual funds: a stock fund, and a bond fund. The probability distribution of the risky fund is: The correlation between the fund return is 0 . 23. 23. What's the excepted return of a portfolio with 40% invested in stock fund and the rest in a bond fund? a. 8% b. 12.8% c. 14% d. 24% 24. you want to construct a portfolio using the two funds that gives a target return of 14%. Whats the standard deviation of such portfolio? a. 12% b. 17% c. 18% d. 26% e. 37% 25. if the risk free rate is 1% the maximum sharpe ratio that an investor can achieve is? a. 0.4 b. 0.6 c. 0.7 d. 0.8 e. 0.9

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock