Pie Corporation acquired 75 percent of Slice Company's ownership on January 1, 20X8, for $93,000. At...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

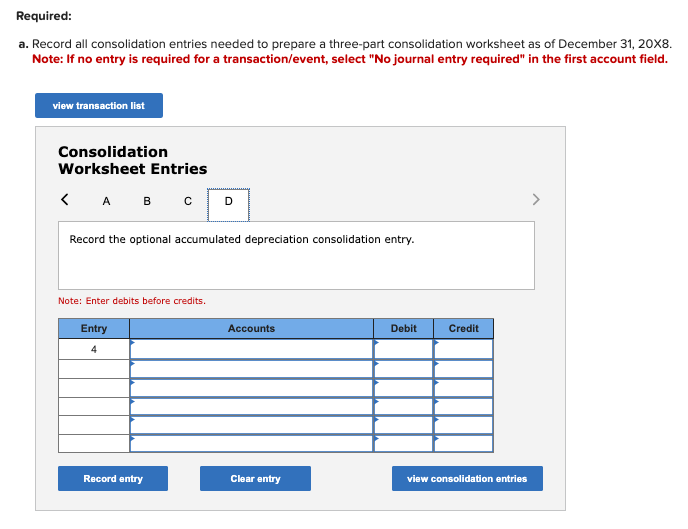

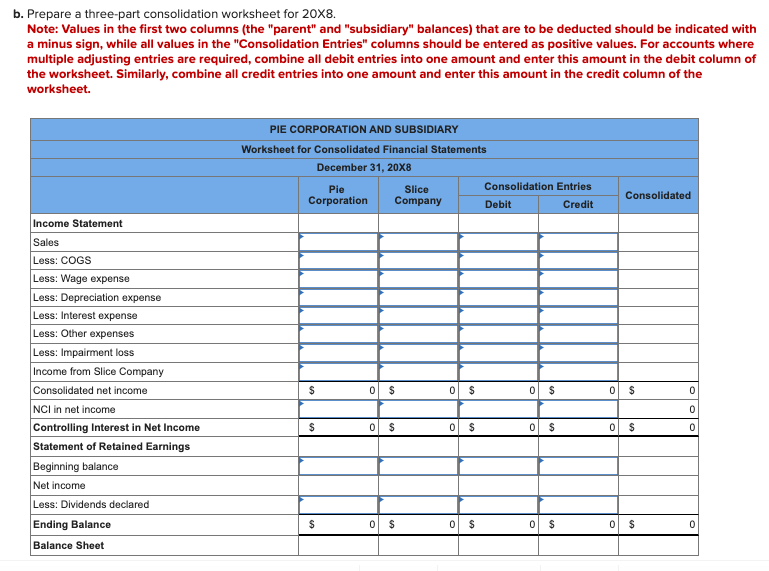

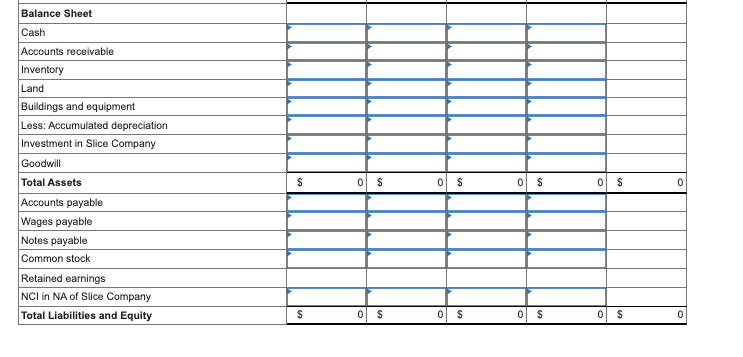

Pie Corporation acquired 75 percent of Slice Company's ownership on January 1, 20X8, for $93,000. At that date, the fair value of the noncontrolling interest was $31,000. The book value of Slice's net assets at acquisition was $90,000. The book values and fair values of Slice's assets and liabilities were equal, except for Slice's buildings and equipment, which were worth $18,000 more than book value. Accumulated depreciation on the buildings and equipment was $24,000 on the acquisition date. Buildings and equipment are depreciated on a 10-year basis. Although goodwill is not amortized, the management of Pie concluded at December 31, 20X8, that goodwill from its purchase of Slice shares had been impaired and the correct carrying amount was $3,100. Goodwill and goodwill impairment were assigned proportionately to the controlling and noncontrolling shareholders. Trial balance data for Pie and Slice on December 31, 20X8, are as follows: Item Cash Accounts Receivable Pie Corporation Debit Slice Company Credit Debit Credit $ 50,500 $ 23,000 88,000 14,000 Inventory 108,000 27,000 Land 46,000 17,000 Buildings and Equipment 359,000 162,000 Investment in Slice Company 104,325 Cost of Goods Sold 120,000 105,000 Wage Expense 40,000 23,000 Depreciation Expense 21,000 8,000 Interest Expense 8,000 2,000 Other Expenses 9,500 3,000 Dividends Declared 31,000 17,200 Accumulated Depreciation $ 141,000 Accounts Payable 44,000 $ 32,000 10,000 Wages Payable 11,000 6,000 Notes Payable 207,100 75,200 Common Stock 196,000 54,000 Retained Earnings 98,000 36,000 Sales 264,000 188,000 Income from Slice Company $ 985,325 24,225 $ 985,325 $ 401,200 $ 401,200 Required: a. Record all consolidation entries needed to prepare a three-part consolidation worksheet as of December 31, 20X8. Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Required: a. Record all consolidation entries needed to prepare a three-part consolidation worksheet as of December 31, 20X8. Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field. view transaction list Consolidation Worksheet Entries A B C D Record the basic consolidation entry. Note: Enter debits before credits. Entry 1 Accounts Debit Credit Record entry Clear entry view consolidation entries Required: a. Record all consolidation entries needed to prepare a three-part consolidation worksheet as of December 31, 20X8. Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field. view transaction list Consolidation Worksheet Entries > A B C D Record the amortized excess value reclassification entry. Note: Enter debits before credits. Entry 2 Accounts Debit Credit Record entry Clear entry view consolidation entries > Required: a. Record all consolidation entries needed to prepare a three-part consolidation worksheet as of December 31, 20X8. Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field. view transaction list Consolidation Worksheet Entries < A B C Record the excess value (differential) reclassification entry. Note: Enter debits before credits. Entry 3 Accounts Debit Credit Record entry Clear entry view consolidation entries Required: a. Record all consolidation entries needed to prepare a three-part consolidation worksheet as of December 31, 20X8. Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field. view transaction list Consolidation Worksheet Entries A B C D Record the optional accumulated depreciation consolidation entry. Note: Enter debits before credits. Entry 4 Accounts Debit Credit Record entry Clear entry view consolidation entries b. Prepare a three-part consolidation worksheet for 20X8. Note: Values in the first two columns (the "parent" and "subsidiary" balances) that are to be deducted should be indicated with a minus sign, while all values in the "Consolidation Entries" columns should be entered as positive values. For accounts where multiple adjusting entries are required, combine all debit entries into one amount and enter this amount in the debit column of the worksheet. Similarly, combine all credit entries into one amount and enter this amount in the credit column of the worksheet. Income Statement Sales Less: COGS Less: Wage expense Less: Depreciation expense Less: Interest expense Less: Other expenses Less: Impairment loss PIE CORPORATION AND SUBSIDIARY Worksheet for Consolidated Financial Statements December 31, 20X8 Pie Corporation Slice Company Consolidation Entries Consolidated Debit Credit Income from Slice Company Consolidated net income $ 0 $ 0 $ 0 $ 0 $ 0 NCI in net income 0 Controlling Interest in Net Income $ 0 $ 0 $ 0 $ 0 $ 0 Statement of Retained Earnings Beginning balance Net income Less: Dividends declared Ending Balance Balance Sheet $ $ 0 $ 0 $ $ Balance Sheet Cash Accounts receivable Inventory Land Buildings and equipment Less: Accumulated depreciation Investment in Slice Company Goodwill Total Assets Accounts payable Wages payable Notes payable Common stock $ 0 $ 0 $ 0 $ 0 $ 0 Retained earnings NCI in NA of Slice Company Total Liabilities and Equity $ 0 $ 0 $ 0 $ 0 $ Pie Corporation acquired 75 percent of Slice Company's ownership on January 1, 20X8, for $93,000. At that date, the fair value of the noncontrolling interest was $31,000. The book value of Slice's net assets at acquisition was $90,000. The book values and fair values of Slice's assets and liabilities were equal, except for Slice's buildings and equipment, which were worth $18,000 more than book value. Accumulated depreciation on the buildings and equipment was $24,000 on the acquisition date. Buildings and equipment are depreciated on a 10-year basis. Although goodwill is not amortized, the management of Pie concluded at December 31, 20X8, that goodwill from its purchase of Slice shares had been impaired and the correct carrying amount was $3,100. Goodwill and goodwill impairment were assigned proportionately to the controlling and noncontrolling shareholders. Trial balance data for Pie and Slice on December 31, 20X8, are as follows: Item Cash Accounts Receivable Pie Corporation Debit Slice Company Credit Debit Credit $ 50,500 $ 23,000 88,000 14,000 Inventory 108,000 27,000 Land 46,000 17,000 Buildings and Equipment 359,000 162,000 Investment in Slice Company 104,325 Cost of Goods Sold 120,000 105,000 Wage Expense 40,000 23,000 Depreciation Expense 21,000 8,000 Interest Expense 8,000 2,000 Other Expenses 9,500 3,000 Dividends Declared 31,000 17,200 Accumulated Depreciation $ 141,000 Accounts Payable 44,000 $ 32,000 10,000 Wages Payable 11,000 6,000 Notes Payable 207,100 75,200 Common Stock 196,000 54,000 Retained Earnings 98,000 36,000 Sales 264,000 188,000 Income from Slice Company $ 985,325 24,225 $ 985,325 $ 401,200 $ 401,200 Required: a. Record all consolidation entries needed to prepare a three-part consolidation worksheet as of December 31, 20X8. Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Required: a. Record all consolidation entries needed to prepare a three-part consolidation worksheet as of December 31, 20X8. Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field. view transaction list Consolidation Worksheet Entries A B C D Record the basic consolidation entry. Note: Enter debits before credits. Entry 1 Accounts Debit Credit Record entry Clear entry view consolidation entries Required: a. Record all consolidation entries needed to prepare a three-part consolidation worksheet as of December 31, 20X8. Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field. view transaction list Consolidation Worksheet Entries > A B C D Record the amortized excess value reclassification entry. Note: Enter debits before credits. Entry 2 Accounts Debit Credit Record entry Clear entry view consolidation entries > Required: a. Record all consolidation entries needed to prepare a three-part consolidation worksheet as of December 31, 20X8. Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field. view transaction list Consolidation Worksheet Entries < A B C Record the excess value (differential) reclassification entry. Note: Enter debits before credits. Entry 3 Accounts Debit Credit Record entry Clear entry view consolidation entries Required: a. Record all consolidation entries needed to prepare a three-part consolidation worksheet as of December 31, 20X8. Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field. view transaction list Consolidation Worksheet Entries A B C D Record the optional accumulated depreciation consolidation entry. Note: Enter debits before credits. Entry 4 Accounts Debit Credit Record entry Clear entry view consolidation entries b. Prepare a three-part consolidation worksheet for 20X8. Note: Values in the first two columns (the "parent" and "subsidiary" balances) that are to be deducted should be indicated with a minus sign, while all values in the "Consolidation Entries" columns should be entered as positive values. For accounts where multiple adjusting entries are required, combine all debit entries into one amount and enter this amount in the debit column of the worksheet. Similarly, combine all credit entries into one amount and enter this amount in the credit column of the worksheet. Income Statement Sales Less: COGS Less: Wage expense Less: Depreciation expense Less: Interest expense Less: Other expenses Less: Impairment loss PIE CORPORATION AND SUBSIDIARY Worksheet for Consolidated Financial Statements December 31, 20X8 Pie Corporation Slice Company Consolidation Entries Consolidated Debit Credit Income from Slice Company Consolidated net income $ 0 $ 0 $ 0 $ 0 $ 0 NCI in net income 0 Controlling Interest in Net Income $ 0 $ 0 $ 0 $ 0 $ 0 Statement of Retained Earnings Beginning balance Net income Less: Dividends declared Ending Balance Balance Sheet $ $ 0 $ 0 $ $ Balance Sheet Cash Accounts receivable Inventory Land Buildings and equipment Less: Accumulated depreciation Investment in Slice Company Goodwill Total Assets Accounts payable Wages payable Notes payable Common stock $ 0 $ 0 $ 0 $ 0 $ 0 Retained earnings NCI in NA of Slice Company Total Liabilities and Equity $ 0 $ 0 $ 0 $ 0 $

Expert Answer:

Related Book For

Advanced Financial Accounting

ISBN: 9781265042615

13th International Edition

Authors: Theodore E. Christensen, David M. Cottrell, Cassy Budd

Posted Date:

Students also viewed these accounting questions

-

This problem is a continuation of P533. Pie Corporation acquired 75 percent of Slice Companys ownership on January 1, 20X8, for $96,000. At that date, the fair value of the noncontrolling interest...

-

Do you think companies that opt to use the international strategy are typically looking to have low cost pressures as well as low pressure from the local consumers?

-

The Soda Corp. has decided to launch a new product of canned drink that will include "fruity" flavors,. The marketing department is predicting that there will be an increase in demand because of a...

-

On 28 April 2020, Mr Guna, CEO of Econ Engineering Malaysia, proposed to complete an abandoned boiler project that no one had dared to revive. He knew that the project was 60% complete before it was...

-

(a) (b) RNA polymerase cytochrome c Elution volume RNA polymerase Direction of migration cytochrome c

-

Color Explosion prepares and packages paint products. Color Explosion has two departments: Blending and Packaging. Direct materials are added at the beginning of the blending process (dyes) and at...

-

Which profit margin measures the overall operating efficiency of the firm? (a) Gross profit margin. (b) Operating profit margin. (c) Net profit margin. (d) Return on equity.

-

Curts Casting manufactures metal parts in a large manufacturing facility. Curts customers order 100,000 tons of castings each quarter. The facility has a practical capacity of 150,000 tons. Curt...

-

The table below gives information on the Results of two semesters in Muscat College Language Center in the year 2018. Semester 1-2018 Results Semester 2 -2018 Results Name Reading Writing Listening...

-

The following is the extract from trial balance of Green Limited, subsidiary of Yellow Limited for the year ended 31 December 2021. Inventory on hand: 31/12/2020 Sales Purchases Depreciation Rent...

-

An economy depends on two commodities, bees and honey. It takes 3 4 units of bees to produce 1 unit of honey and 1 2 unit of honey to produce 1 unit of bees. Find the production required to satisfy a...

-

During Pete's exit interview he states that he did not receive managerial direction or training in regard to accessing computer systems and online patient records. The hospital administrator reviews...

-

How do viruses exhibit remarkable genetic diversity and adaptive potential through mechanisms such as mutation, recombination, and reassortment, and what are the implications of viral genetic...

-

k=0 2k 'WI Find the sum of the series:

-

Using the two article links below Coca Cola and Starbucks, compare these two brands to uncover how the branding makes them part of the top 10 list of successful brands worldwide. Answer the following...

-

Choose one independent variable and one dependent variable from the data set. The variables from the data set are as follows: Write and analysis paper about the variables chosen and also address the...

-

In Exercises, find the equation of the tangent line at the given point on each curve. 2y 2 - x = 4; (16, 2)

-

How much would the price have to fall for consumers to be willing to buy 1 million more tons of coffee per month?

-

How does the quota, \(\bar{Q}\), set by the United States on foreign sugar imports affect the total American supply curve for sugar given the domestic supply curve, \(S^{d}\) in panel a of the graph,...

-

Using the demand function for lamb from Question 1.1, show how the quantity demanded at a given price changes as annual per capita income, Y, increases by AU$200. Data From Question 1.1:- Suppose...

Study smarter with the SolutionInn App