Question: please answer both questions Use the Black-Scholes model to value a call option with the following data: Price $34 Post your answer with 2 decimal

please answer both questions

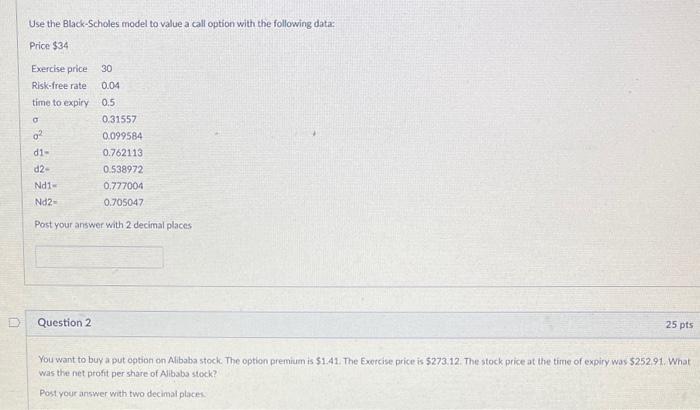

Use the Black-Scholes model to value a call option with the following data: Price $34 Post your answer with 2 decimal places Question 2 You want to buy a put ogtion on Alibaba stock. The option premium is $1.41. The Exercise price is 5273.12 . The stock price at the time of expiry was 5252,91 . What was the net profit per share of Alibaba stock? Post your answer with two decimal places

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock