Question: * * Please answer the question accurately showing step - by - step solution by hand. NO EXCEL allowed. P . S . : Use

Please answer the question accurately showing stepbystep solution by hand.

NO EXCEL allowed.

PS: Use the appropriate Statistical tables if needed.

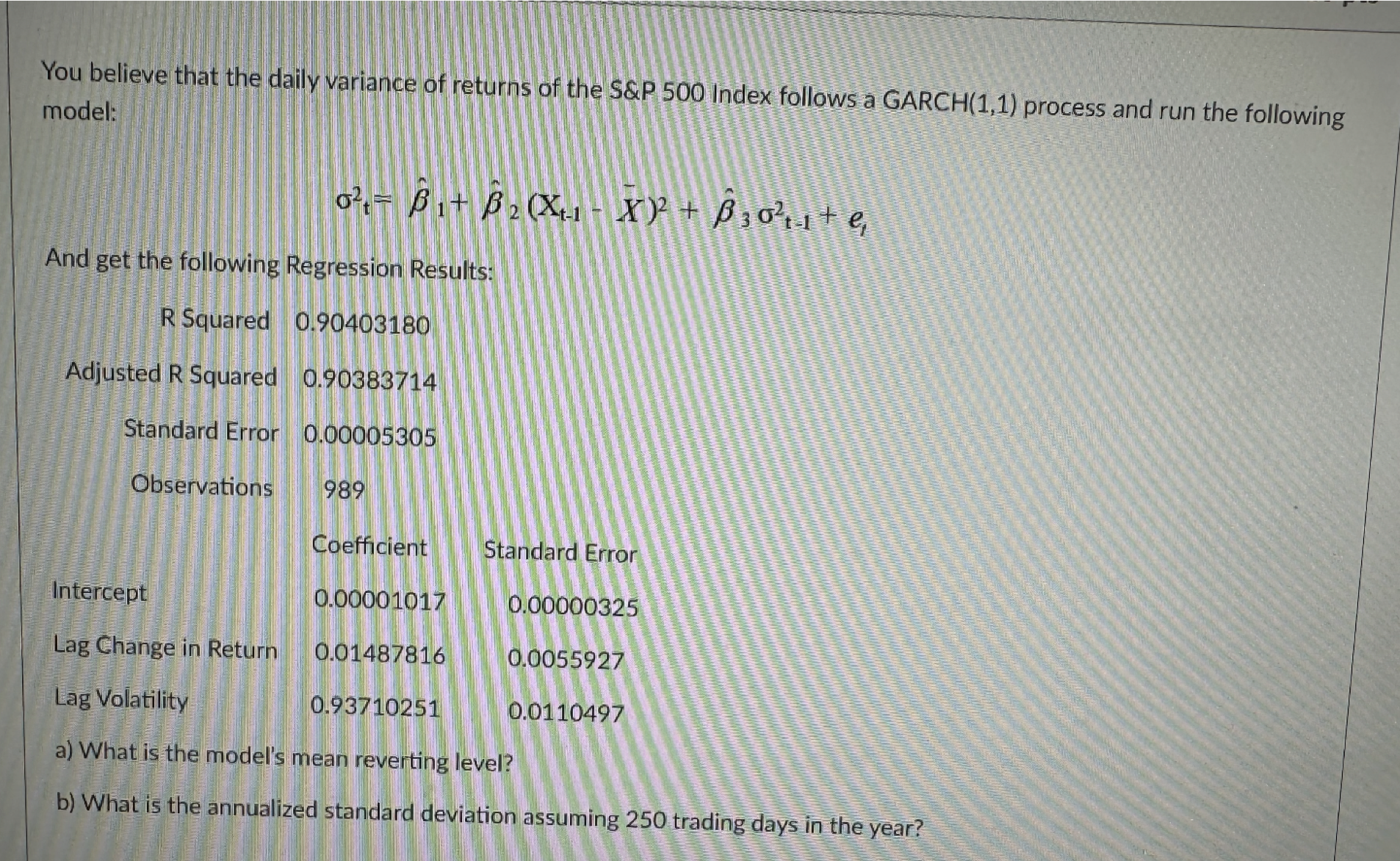

You believe that the daily variance of returns of the S&P Index follows a GARCH process and run the following

model:

hathathat

And get the following Regression Results:

a What is the model's mean reverting level?

b What is the annualized standard deviation assuming trading days in the year?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock