Question: Please as soon as possible 2. Consider a three-period binomial model in Figure 2 with S0=4,u=2, and d=1/2. The risk-free rate is 10% at each

Please as soon as possible

Please as soon as possible

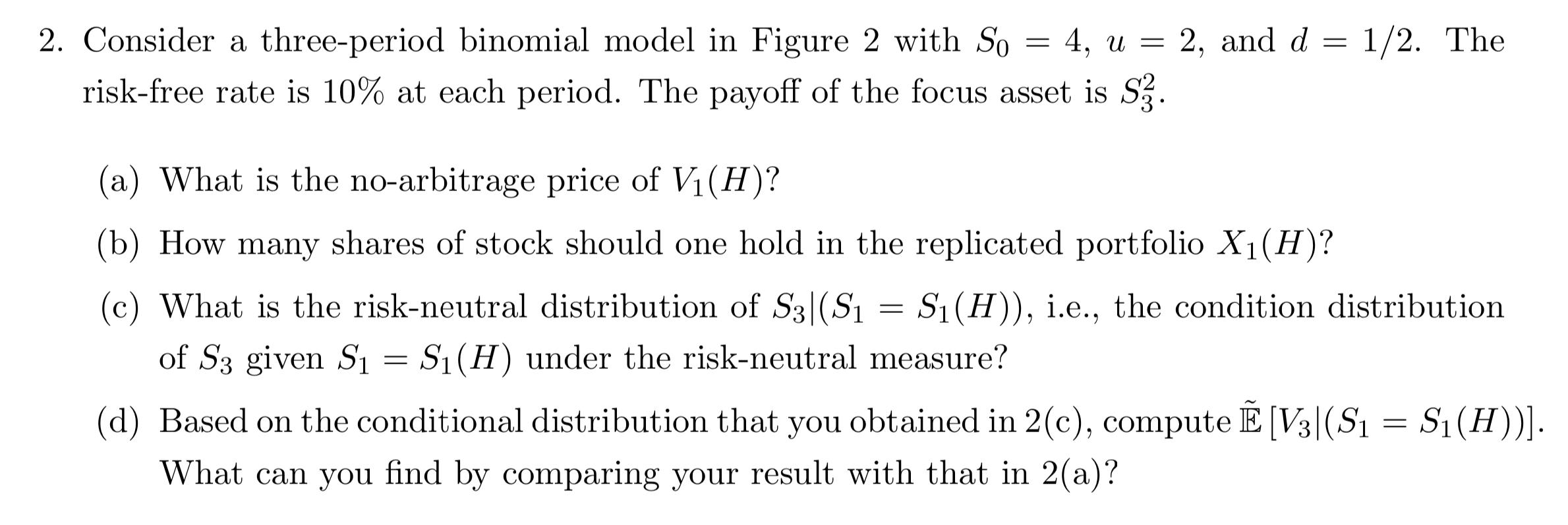

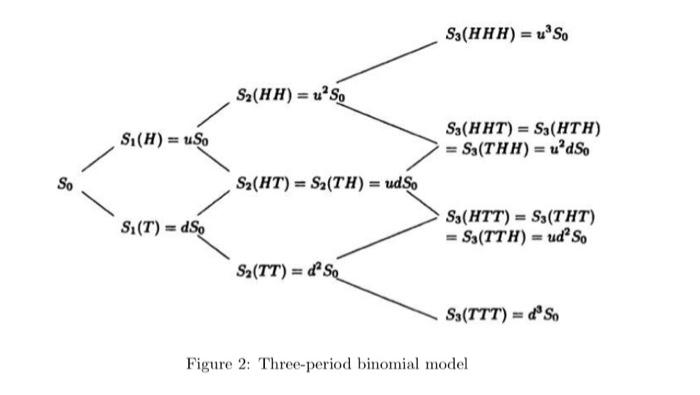

2. Consider a three-period binomial model in Figure 2 with S0=4,u=2, and d=1/2. The risk-free rate is 10% at each period. The payoff of the focus asset is S32. (a) What is the no-arbitrage price of V1(H) ? (b) How many shares of stock should one hold in the replicated portfolio X1(H) ? (c) What is the risk-neutral distribution of S3(S1=S1(H)), i.e., the condition distribution of S3 given S1=S1(H) under the risk-neutral measure? (d) Based on the conditional distribution that you obtained in 2( c ), compute E~[V3(S1=S1(H))]. What can you find by comparing your result with that in 2(a) ? Figure 2: Three-period binomial model 2. Consider a three-period binomial model in Figure 2 with S0=4,u=2, and d=1/2. The risk-free rate is 10% at each period. The payoff of the focus asset is S32. (a) What is the no-arbitrage price of V1(H) ? (b) How many shares of stock should one hold in the replicated portfolio X1(H) ? (c) What is the risk-neutral distribution of S3(S1=S1(H)), i.e., the condition distribution of S3 given S1=S1(H) under the risk-neutral measure? (d) Based on the conditional distribution that you obtained in 2( c ), compute E~[V3(S1=S1(H))]. What can you find by comparing your result with that in 2(a) ? Figure 2: Three-period binomial model

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts