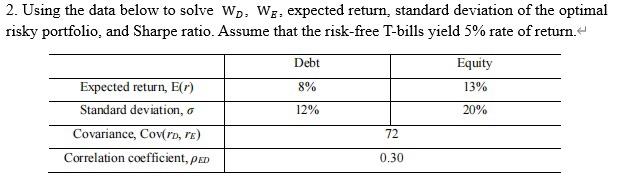

Question: please be accurate 2. Using the data below to solve WD,WE, expected return, standard deviation of the optimal risky portfolio, and Sharpe ratio. Assume that

please be accurate

2. Using the data below to solve WD,WE, expected return, standard deviation of the optimal risky portfolio, and Sharpe ratio. Assume that the risk-free T-bills yield 5% rate of return

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock