Complete the calculation of profit and loss and reconciliation to taxable income/loss sections of the Company Tax

Fantastic news! We've Found the answer you've been seeking!

Question:

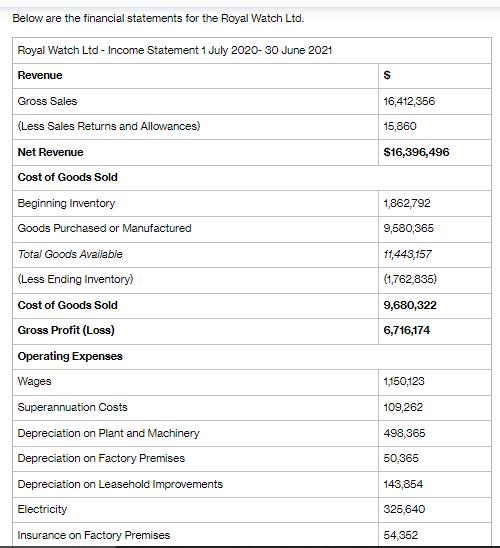

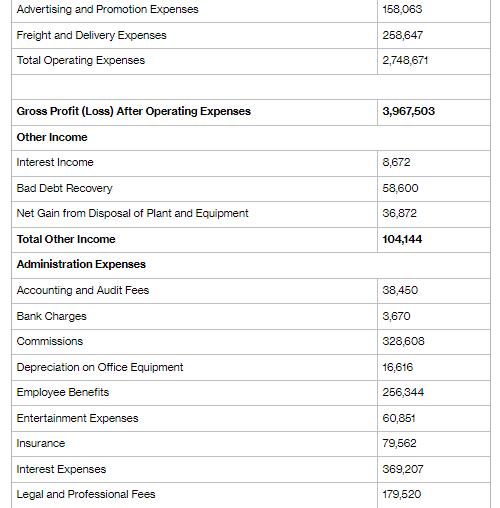

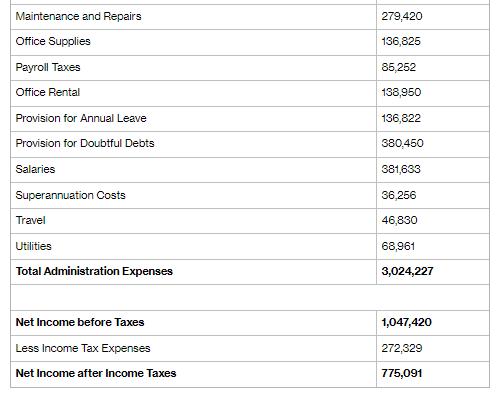

Complete the calculation of profit and loss and reconciliation to taxable income/loss sections of the Company Tax Return for the year ended 30 June 2021.

All blank boxes must be completed.

*Show your workings for the Non-deductible expenses (label W).

Note: The table is based on the Australian Taxation Office's Company Tax Return for 2021. The full return can be found at: You are a tax agent and have been engaged by Royal Watch Ltd to prepare their 2020/21 Income Tax Return.

- Royal Watch Ltd is a manufacturer and exporter of fashion watches and designer decorative clocks. Its activities have not changed during the tax year 2020/21. For accounting purposes, the company uses the straight-line method to depreciate assets. For taxation purposes, it chooses to use the diminishing value method to depreciate its assets. All assets are purchased post 10 May 2006 and the leasehold improvement is in relation to the leased office. The opening adjustable values as at 1 July 2020 are:

| Asset | Effective Live | Opening Adjustable Value |

| Plant and Machinery | 10 years | $3,125,052 |

| Leasehold improvement | 15 years | $1,635,988 |

| Office Equipment | 4 years | $250,635 |

- The company purchased office equipment of $50,890 on 1 November 2020.

- The company depreciates the building over 40 years for both accounting and taxation purposes. The construction cost of the factory premises is $2,014,600.

- Repairs and maintenance expense included the cost for the replacement of carpet in the factory meeting rooms with premier stone floor. This cost of $123,540 was paid on 1 April 2021.

- Among the entertainment expenses, $38,450 was for food and drinks provided during five whole day in-house seminars attended by clients and employees. The balance was for lunches and dinners with customers.

- The payment of annual leave was $35,750 during the year 2020/21.

- A provision of 5% is made on debts which are overdue for more than 30 days except for one debt which has been overdue for more than 12 months. A full provision has been made for this debt of $230,798. However, the receivables clerk failed to mail a legal claim to the client's correct address.

- The company has a franking account surplus of $8,000 on 1 July 2020. In addition, the company made the following transactions:

- On 21 July 2020 the company made a PAYG instalment payment of $40,500.

- On 21 October 2020 the company made a PAYG instalment payment of $45,500.

- On 1 November 2020, the company received a tax refund of $35,680 for the tax year 2019/20.

- On 31 December 2020, the company paid a fully franked interim dividend of $350,000.

- On 21 January 2021 the company made a PAYG instalment payment of $55,500.

- On 21 April 2021 the company made a PAYG instalment payment of $50,500.

- On 1 June 2021 the company received a dividend of $220,000. This had a franking percentage of 75%.

- On 30 June 2021 the company paid a fully franked final dividend of $450,000.

Expert Answer:

To complete the calculation of profit and loss and reconciliation to taxable incomeloss for Royal Wa... View the full answer

Related Book For

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

Posted Date: