Question: please do it correctly will upvote Question 2. (Total 20 marks) Use the following information to answer question a) to c). Assume that you have

please do it correctly will upvote

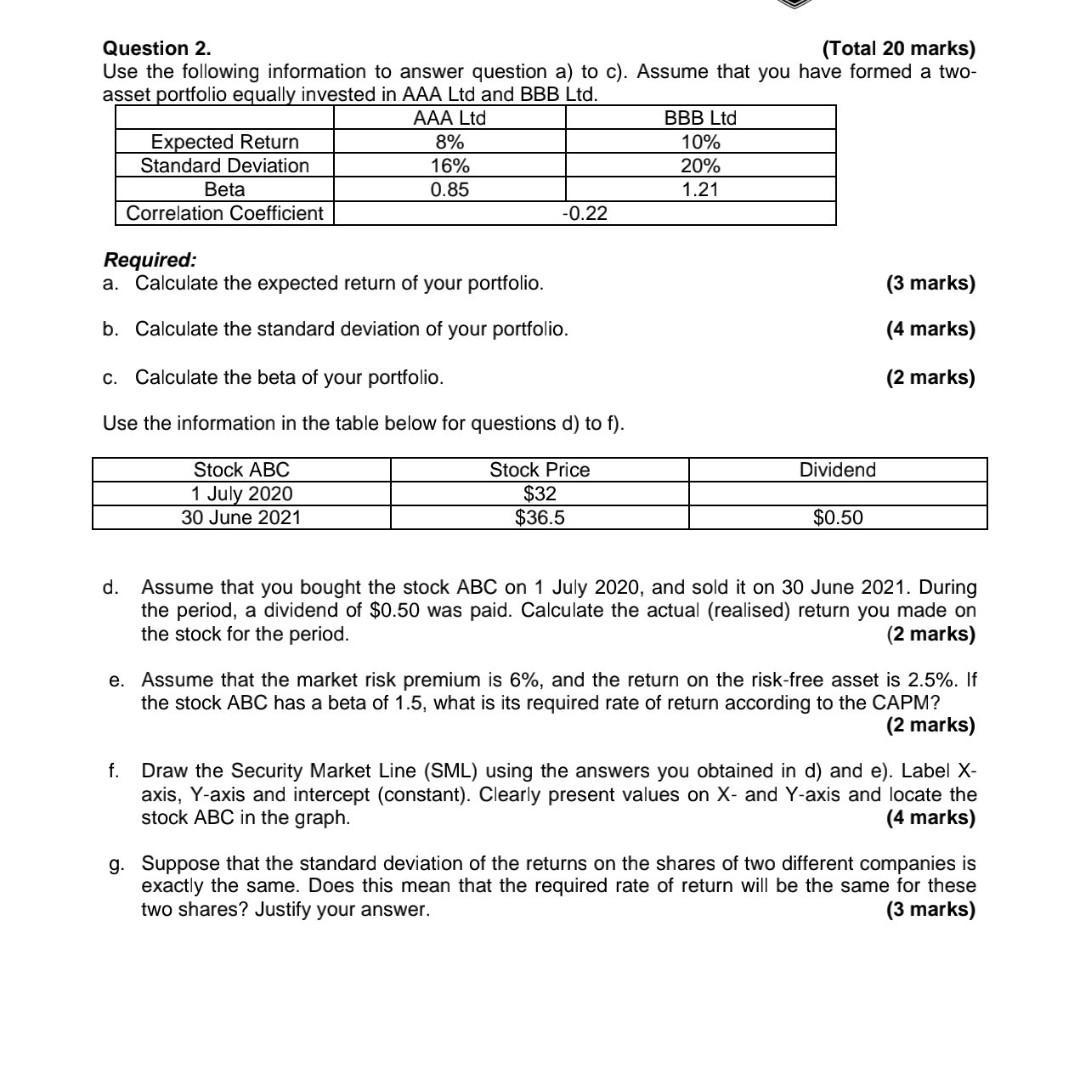

Question 2. (Total 20 marks) Use the following information to answer question a) to c). Assume that you have formed a two- asset portfolio equally invested in AAA Ltd and BBB Ltd. AAA Ltd BBB Ltd 8% 10% Expected Return Standard Deviation 16% 20% Beta 0.85 1.21 Correlation Coefficient -0.22 Required: a. Calculate the expected return of your portfolio. (3 marks) b. Calculate the standard deviation of your portfolio. (4 marks) c. Calculate the beta of your portfolio. (2 marks) Use the information in the table below for questions d) to f). Stock ABC Stock Price Dividend 1 July 2020 $32 $36.5 30 June 2021 $0.50 d. Assume that you bought the stock ABC on 1 July 2020, and sold it on 30 June 2021. During the period, a dividend of $0.50 was paid. Calculate the actual (realised) return you made on the stock for the period. (2 marks) e. Assume that the market risk premium is 6%, and the return on the risk-free asset is 2.5%. If the stock ABC has a beta of 1.5, what is its required rate of return according to the CAPM? (2 marks) f. Draw the Security Market Line (SML) using the answers you obtained in d) and e). Label X- axis, Y-axis and intercept (constant). Clearly present values on X- and Y-axis and locate the stock ABC in the graph. (4 marks) g. Suppose that the standard deviation of the returns on the shares of two different companies is exactly the same. Does this mean that the required rate of return will be the same for these two shares? Justify your

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts