Question: PLEASE, DO NOT COPY AND PASTE ANY ANSWER FROM OTHER CHEGG POSTS Please show me all work so I can learn. Thanks! The option premiums

PLEASE, DO NOT COPY AND PASTE ANY ANSWER FROM OTHER CHEGG POSTS

Please show me all work so I can learn. Thanks!

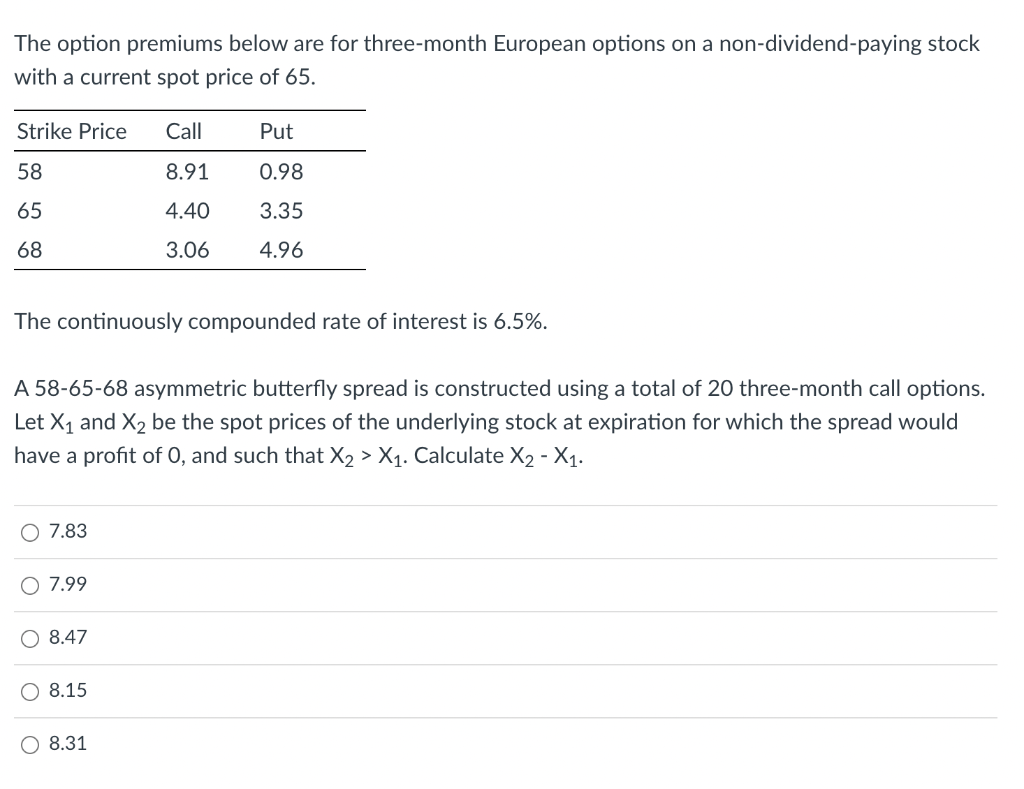

The option premiums below are for three-month European options on a non-dividend-paying stock with a current spot price of 65. Strike Price Call Put 58 8.91 0.98 65 4.40 3.35 68 3.06 4.96 The continuously compounded rate of interest is 6.5%. A 58-65-68 asymmetric butterfly spread is constructed using a total of 20 three-month call options. Let X1 and X2 be the spot prices of the underlying stock at expiration for which the spread would have a profit of O, and such that X2 > X1. Calculate X2 - X1. O 7.83 O 7.99 O 8.47 8.15 O 8.31

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock