Question: Please find question 14.2 here. as for the question b the AR(4) model is The index of industrial production (IPt) is a monthly time series

Please find question 14.2 here.

as for the question b

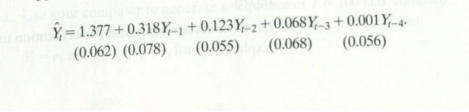

the AR(4) model is

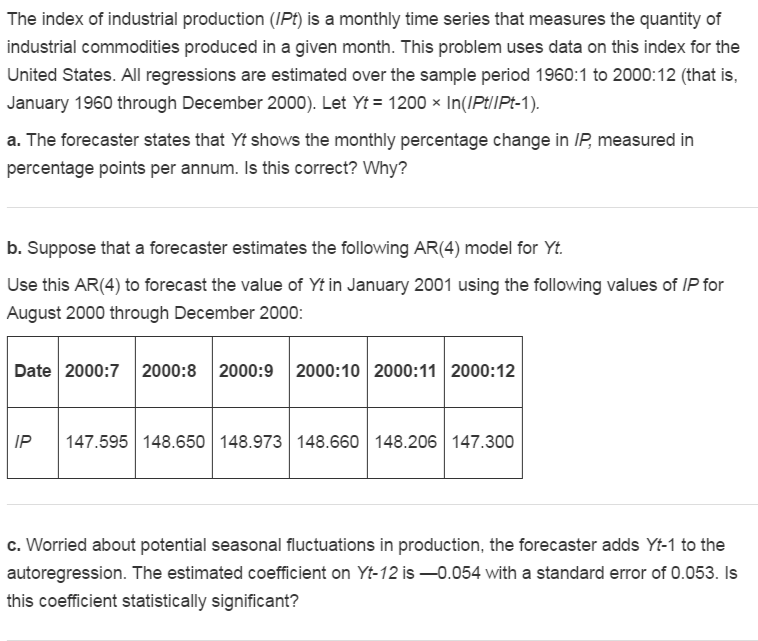

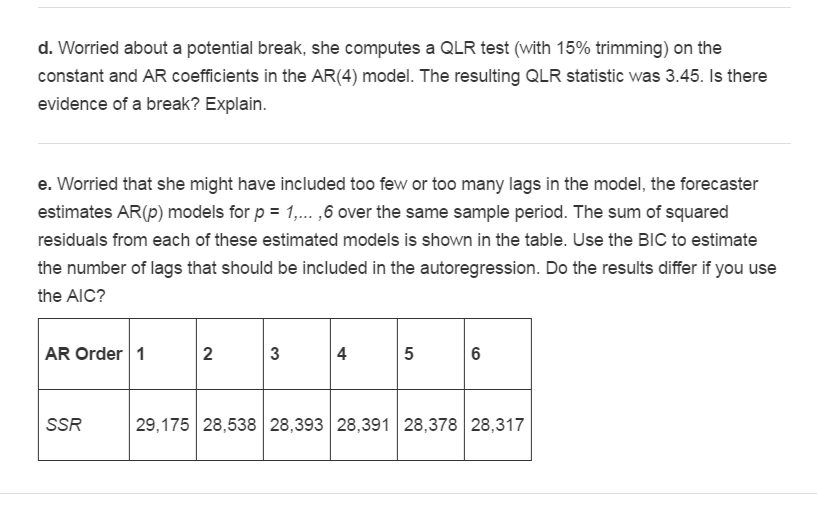

The index of industrial production (IPt) is a monthly time series that measures the quantity of industrial commodities produced in a given month. This problem uses data on this index for the United States. All regressions are estimated over the sample period 1960:1 to 2000:12 (that is, January 1960 through December 2000). Let Yt= 1200 in(RIP-1). a. The forecaster states that Yt shows the monthly percentage change in IP measured in percentage points per annum. Is this correct? Why? b. Suppose that a forecaster estimates the following AR(4) model for Yt. Use this AR(4) to forecast the value of Yt in January 2001 using the following values of IP for August 2000 through December 2000: Date 2000:7 2000:8 2000:9 2000:10 2000:11 2000:12 IP 147.595148.650 148.973 148.660 148.206 147.300 c. Worried about potential seasonal fluctuations in production, the forecaster adds Yt-1 to the autoregression. The estimated coefficient on Yt-12 is -0.054 with a standard error of 0.053. Is this coefficient statistically significant? The index of industrial production (IPt) is a monthly time series that measures the quantity of industrial commodities produced in a given month. This problem uses data on this index for the United States. All regressions are estimated over the sample period 1960:1 to 2000:12 (that is, January 1960 through December 2000). Let Yt= 1200 in(RIP-1). a. The forecaster states that Yt shows the monthly percentage change in IP measured in percentage points per annum. Is this correct? Why? b. Suppose that a forecaster estimates the following AR(4) model for Yt. Use this AR(4) to forecast the value of Yt in January 2001 using the following values of IP for August 2000 through December 2000: Date 2000:7 2000:8 2000:9 2000:10 2000:11 2000:12 IP 147.595148.650 148.973 148.660 148.206 147.300 c. Worried about potential seasonal fluctuations in production, the forecaster adds Yt-1 to the autoregression. The estimated coefficient on Yt-12 is -0.054 with a standard error of 0.053. Is this coefficient statistically significant

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts