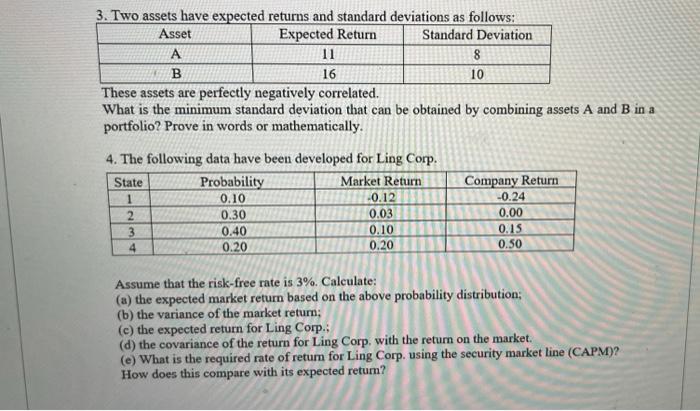

Question: please help! 3. Two assets have expected returns and standard deviations as follows: Asset Expected Return Standard Deviation A 11 8 B 16 10 These

3. Two assets have expected returns and standard deviations as follows: Asset Expected Return Standard Deviation A 11 8 B 16 10 These assets are perfectly negatively correlated. What is the minimum standard deviation that can be obtained by combining assets A and B in a portfolio? Prove in words or mathematically. 4. The following data have been developed for Ling Corp. State Probability Market Return 1 0.10 -0.12 2 0.30 0.03 3 0.40 0.10 4 0.20 0.20 Company Return -0.24 0.00 0.15 0.50 Assume that the risk-free rate is 3%. Calculate: (a) the expected market return based on the above probability distribution: (b) the variance of the market return; (c) the expected return for Ling Corp.: (d) the covariance of the return for Ling Corp, with the return on the market. (e) What is the required rate of retum for Ling Corp. using the security market line (CAPM)? How does this compare with its expected retum

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts