Question: Please help me with the following question based on the given article, there is only one option that is correct. Please also explain why is

Please help me with the following question based on the given article, there is only one option that is correct. Please also explain why is the option correct and other options are wrong.

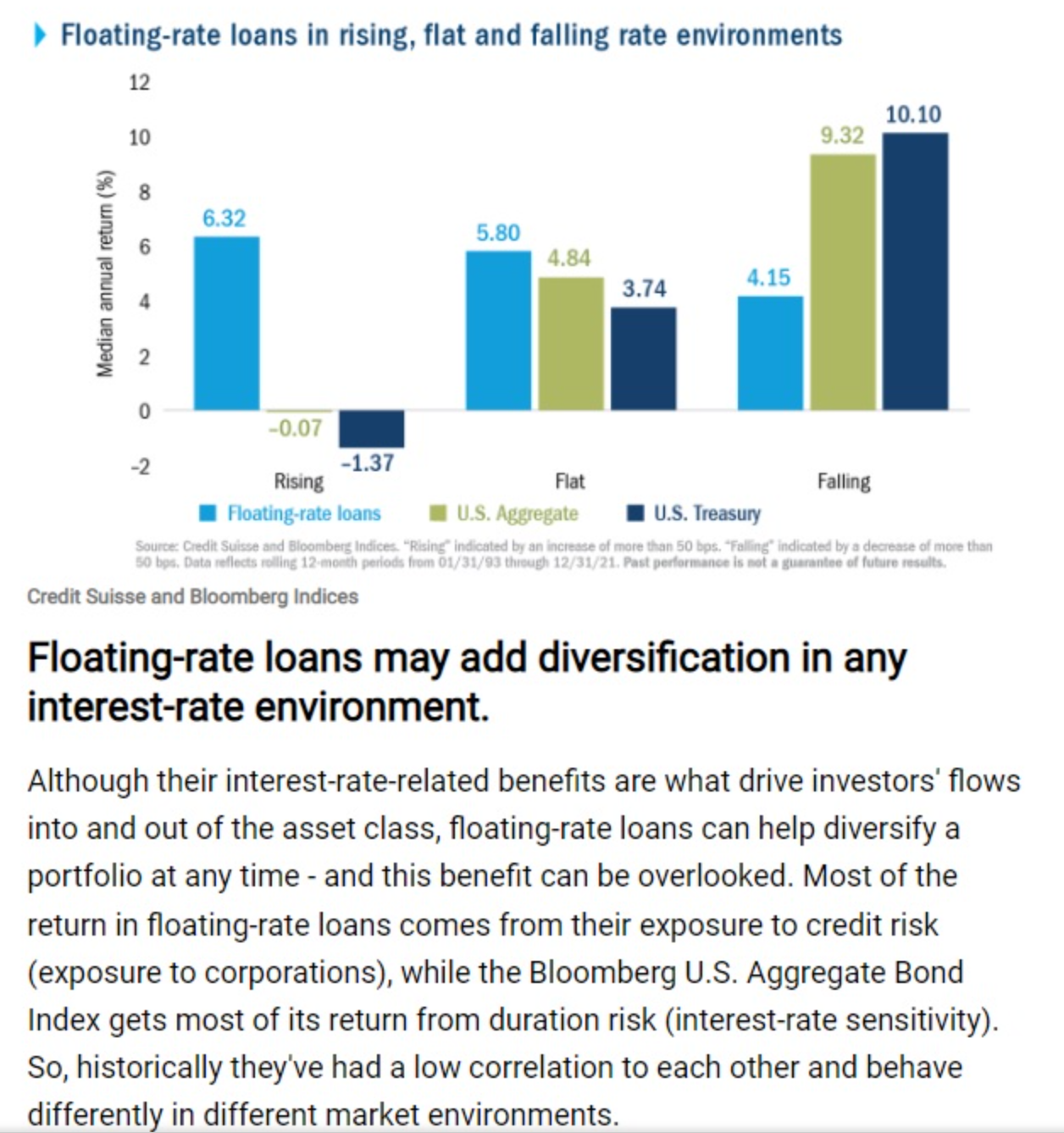

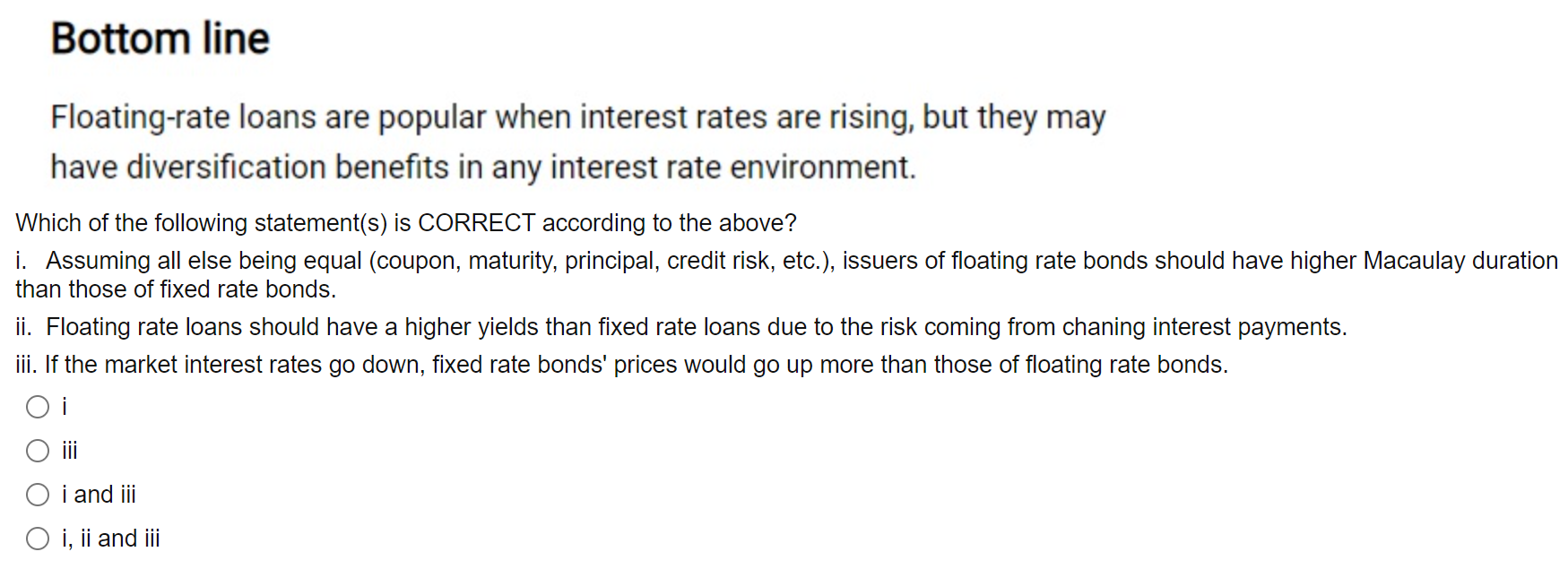

\fFloating-rate loans are known by many names, including bank loans, senior loans, and leveraged loans. They're typically extended to companies with higher levels of debt relative to cash ow, and because of this, they carry greater credit risk than investment-grade bonds. But unlike traditional bonds, oating-rate loans don't make a xed-interest payment, or coupon, for each period. Instead, their coupons reset every 30 or 90 days, oating up or down with the changes in prevailing interest rates. This oating feature makes loan prices less sensitive to shifts in interest rates, so ows into oating-rate loan funds tend to increase when the Federal Reserve is actively raising rates in response to a growing economy and improved labor market. And, as you can guess, this trend tends to reverse when rates are falling. Historically, oating-rate loans have outperformed in rising and at interest- rate environments. When rates are rising, the median annual return for oating-rate loans, as gauged by the Credit Suisse Leveraged Loan index, has exceeded the return on U.S. Treasuries and the Bloomberg U.S. Aggregate Bond Index by more than 6 percentage points. But what's possibly overlooked is that oating-rate loans have also delivered attractive absolute and relative performance regardless of the broader interest-rate environment. Because yield is such a significant component of total return, oating-rate loans also have outperformed U.S. Treasuries and the Bloomberg Aggregate Bond Index when rates are at. It's only when rates fall that we have seen oating-rate loans underperform. \fBottom line Floating-rate loans are popular when interest rates are rising, but they may have diversication benets in any interest rate environment. Which of the following statement(s) is CORRECT according to the above? i. Assuming all else being equal (coupon, maturity, principal, credit risk, etc.), issuers of oating rate bonds should have higher Macaulay duration than those of fixed rate bonds. ii. Floating rate loans should have a higher yields than fixed rate loans due to the risk coming from chaning interest payments. iii. If the market interest rates go down, fixed rate bonds' prices would go up more than those of oating rate bonds. O i 0 iii 0 land iii 0 i, ii and

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!