Question: Please help me with those question. Can't seem to figure out. The standard deviation of the market-index portfolio is 20%. Stock A has a beta

Please help me with those question. Can't seem to figure out.

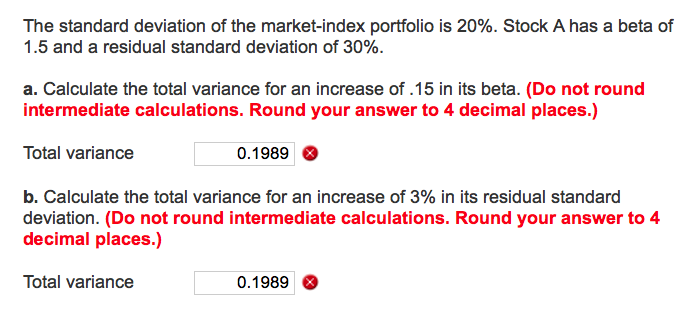

The standard deviation of the market-index portfolio is 20%. Stock A has a beta of 1.5 and a residual standard deviation of 30%. a. Calculate the total variance for an increase of .15 in its beta. (Do not round intermediate calculations. Round your answer to 4 decimal places.) Total variance 0.1989 b. Calculate the total variance for an increase of 3% in its residual standard deviation. (Do not round intermediate calculations. Round your answer to 4 decimal places.) Total variance 0.19898

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock