Question: Please help on these three questions Start with the partial model in the file Ch03 P07 Build a Model.xlsx. Following is information for the required

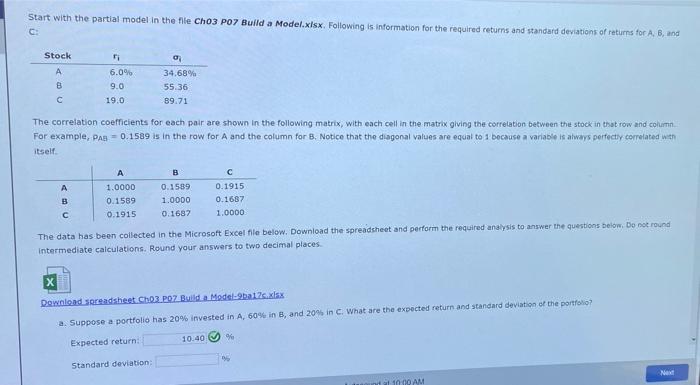

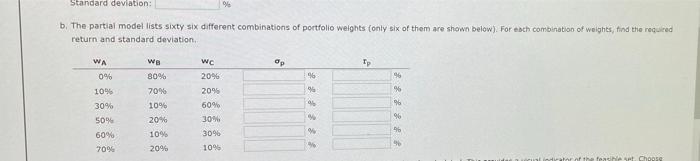

Start with the partial model in the file Ch03 P07 Build a Model.xlsx. Following is information for the required returns and standard deviations of returns for AB, and c Stock B 6.0% 9.0 19.0 34.68% 55.36 89.71 The correlation coefficients for each pair are shown in the following matrix, with each cell in the matrix giving the correlation between the stock in that row and column For example, Pas = 0.1589 is in the row for A and the column for B. Notice that the diagonal values are equal to 1 because a variable is always perfectly correlated with itself A B 1.0000 0.1589 0.1915 0.1589 1.0000 0.1687 0.1915 0.1687 1.0000 The data has been collected in the Microsoft Excel file below. Download the spreadsheet and perform the required analysis to answer the questions below. Do not round intermediate calculations. Round your answers to two decimal places Download spreadsheet.Cho3 POZ Build a Model 9ba1s.xlsx a. Suppose a portfolio has 20% invested in A, 60% in B, and 20% in c. What are the expected return and standard deviation of the portfolio 10.40 % Expected return Standard deviation: de 10 00 AM Standard deviation: 96 b. The partial model lists sixty six different combinations of portfolio welghts (only six of them are shown below). For each combination of weights, find the required return and standard deviation WA Op Tp 0% 96 WB 80% 70% 10% 109 96 96 wc 2096 2096 60% 30% 3096 10% F 96 30% 50% 60% 7096 96 96 20% 10% 20% FreeNA Choose If you seek a return of 10.1%, then what is the smallest standard deviation that you must accept? 96 Check My Work Reset

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts