Question: please help Question 04 ! This vers ! This vers There are two research papers-the second article argues that the first article's results do not

please help

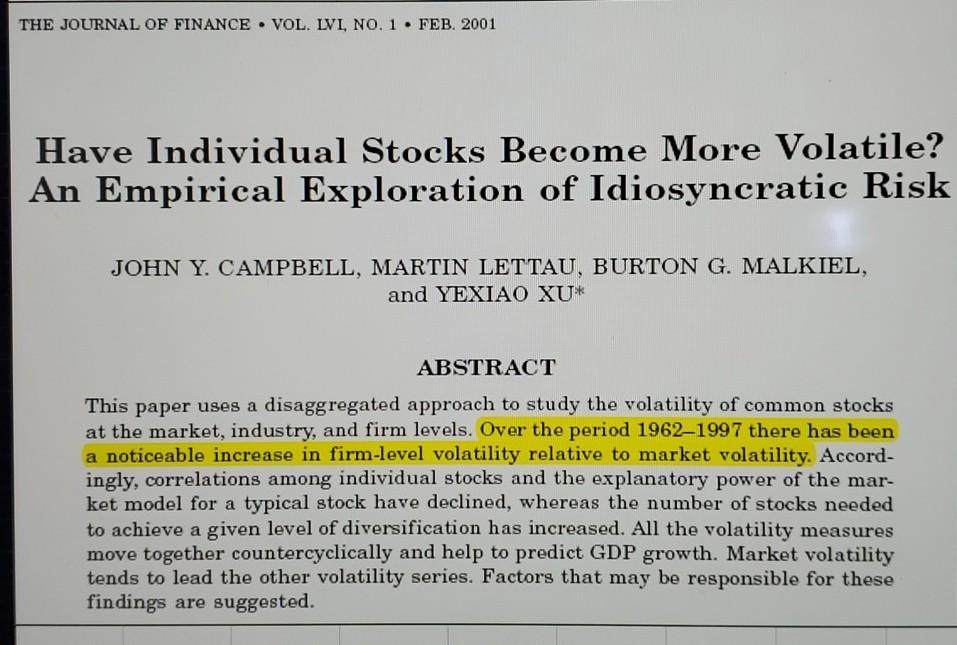

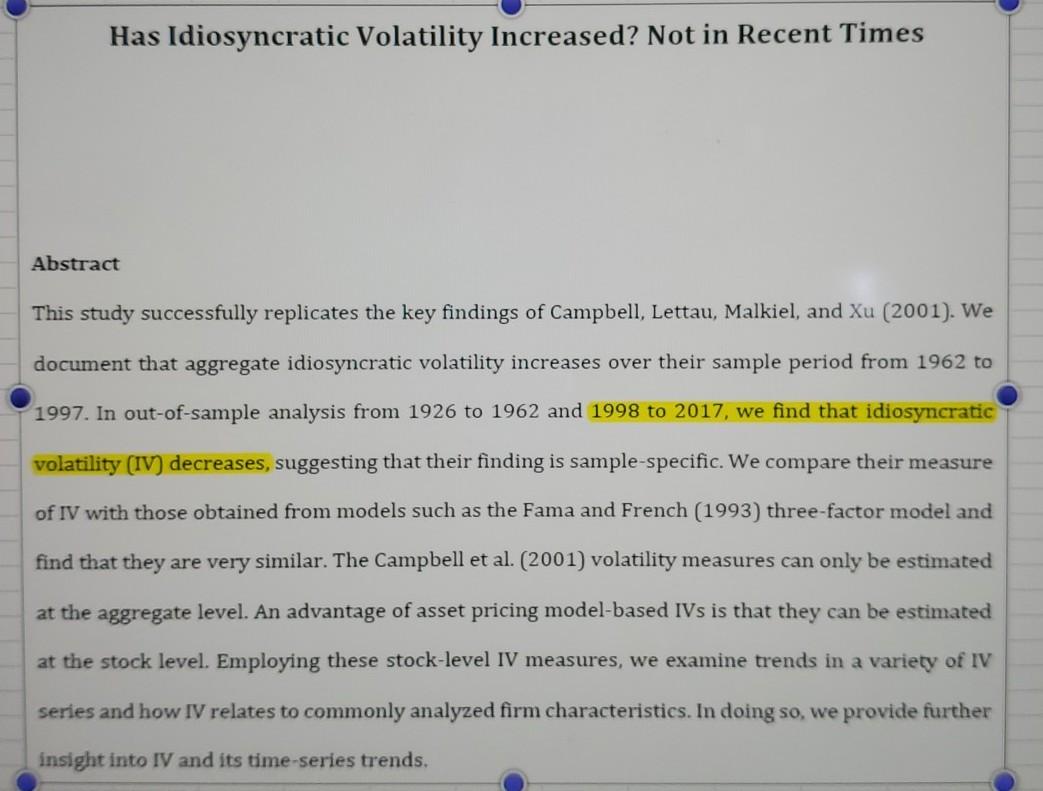

Question 04 ! This vers ! This vers There are two research papers-the second article argues that the first article's results do not hold these days. According to the second article, which of the following statements is true? Hint: Assignment 2 Question 9 A B The portfolio diversification benefit of investors has increased Arbitrary stocks will be more correlated to the market than before Arbitrary two stocks in the market will be less correlated than before Passive investors will demand more stocks for their portfolios than before C D THE JOURNAL OF FINANCE VOL. LVL NO. 1. FEB. 2001 Have Individual Stocks Become More Volatile? An Empirical Exploration of Idiosyncratic Risk JOHN Y. CAMPBELL, MARTIN LETTAU, BURTON G. MALKIEL, and YEXIAO XU* ABSTRACT This paper uses a disaggregated approach to study the volatility of common stocks at the market, industry, and firm levels. Over the period 19621997 there has been a noticeable increase in firm-level volatility relative to market volatility. Accord- ingly, correlations among individual stocks and the explanatory power of the mar- ket model for a typical stock have declined, whereas the number of stocks needed to achieve a given level of diversification has increased. All the volatility measures move together countercyclically and help to predict GDP growth. Market volatility tends to lead the other volatility series. Factors that may be responsible for these findings are suggested. Has Idiosyncratic Volatility Increased? Not in Recent Times Abstract This study successfully replicates the key findings of Campbell, Lettau, Malkiel, and Xu (2001). We document that aggregate idiosyncratic volatility increases over their sample period from 1962 to 1997. In out-of-sample analysis from 1926 to 1962 and 1998 to 2017, we find that idiosyncratic volatility (IV) decreases, suggesting that their finding is sample-specific. We compare their measure of IV with those obtained from models such as the Fama and French (1993) three-factor model and find that they are very similar. The Campbell et al. (2001) volatility measures can only be estimated at the aggregate level. An advantage of asset pricing model-based IVs is that they can be estimated at the stock level. Employing these stock-level IV measures, we examine trends in a variety of IV series and how IV relates to commonly analyzed firm characteristics. In doing so, we provide further insight into IV and its time-series trends

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts