Question: Please help with problem 23. Thank you 23 Using the yield curve in the Appendix, what is the implied 4yr rate in 1 years (to

Please help with problem 23. Thank you

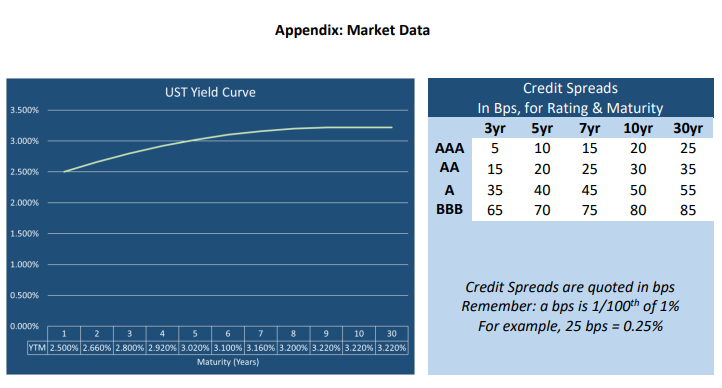

23 Using the yield curve in the Appendix, what is the implied 4yr rate in 1 years (to two decimal places)? Appendix: Market Data UST Yield Curve 3.500% 3.000% Credit Spreads In Bps, for Rating & Maturity 3yr Fyr Fyr 10yr 5 10 15 15 20 25 30 35 40 45 50 65 70 75 80 20 AAA AA A BBB 2.500% 30yr 25 35 55 85 2.000% 1.500% 1.000% 0.500% Credit Spreads are quoted in bps Remember: a bps is 1/100th of 1% For example, 25 bps = 0.25% 0.000% 1 2 3 4 5 6 7 8 9 10 30 YTM 2.500% 2.660% 2.800% 2.920% 3.020% 3.100% 3.160% 3.200% 3.220% 3.220% 3.220% Maturity (Years) 23 Using the yield curve in the Appendix, what is the implied 4yr rate in 1 years (to two decimal places)? Appendix: Market Data UST Yield Curve 3.500% 3.000% Credit Spreads In Bps, for Rating & Maturity 3yr Fyr Fyr 10yr 5 10 15 15 20 25 30 35 40 45 50 65 70 75 80 20 AAA AA A BBB 2.500% 30yr 25 35 55 85 2.000% 1.500% 1.000% 0.500% Credit Spreads are quoted in bps Remember: a bps is 1/100th of 1% For example, 25 bps = 0.25% 0.000% 1 2 3 4 5 6 7 8 9 10 30 YTM 2.500% 2.660% 2.800% 2.920% 3.020% 3.100% 3.160% 3.200% 3.220% 3.220% 3.220% Maturity (Years)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts