Question: Please help with this question. 10.14.* (Finding the optimal investment time (I)) Solve the optimal stopping problem V (s, p) = sup E(s,p) e-p( stt

Please help with this question.

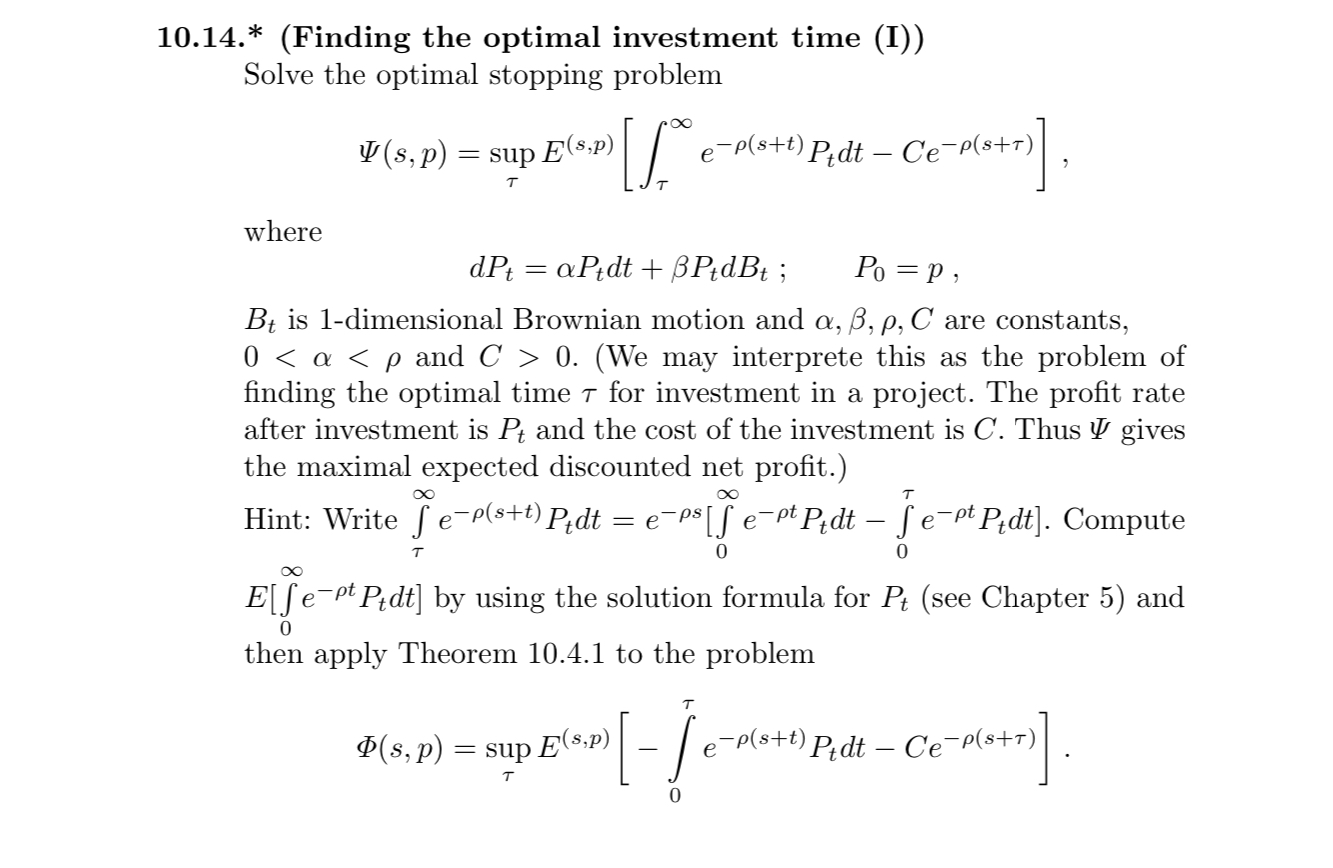

10.14.* (Finding the optimal investment time (I)) Solve the optimal stopping problem V (s, p) = sup E(s,p) e-p( stt ) Pidt - Ce-p(str ) where dPt = aPedt + BPtdBt ; Po = P , Bt is 1-dimensional Brownian motion and a, B, p, C are constants, 0 0. (We may interprete this as the problem of finding the optimal time T for investment in a project. The profit rate after investment is Pt and the cost of the investment is C. Thus I gives the maximal expected discounted net profit.) Hint: Write fe-p(s+t) Pedt = e-Ps[f empt Pidt - Sept Pidt]. Compute E[J e- pt Pedt] by using the solution formula for Pt (see Chapter 5) and 0 then apply Theorem 10.4.1 to the problem D(s, p) = sup E(s,p) - ( e- p(stt ) Pidt - Ce-p(str )

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts