Question: Please help with this question. Question 2 (20 Marks) (A) On June 1, 2019, a bond portfolio manager is evaluating the following data concerning the

Please help with this question.

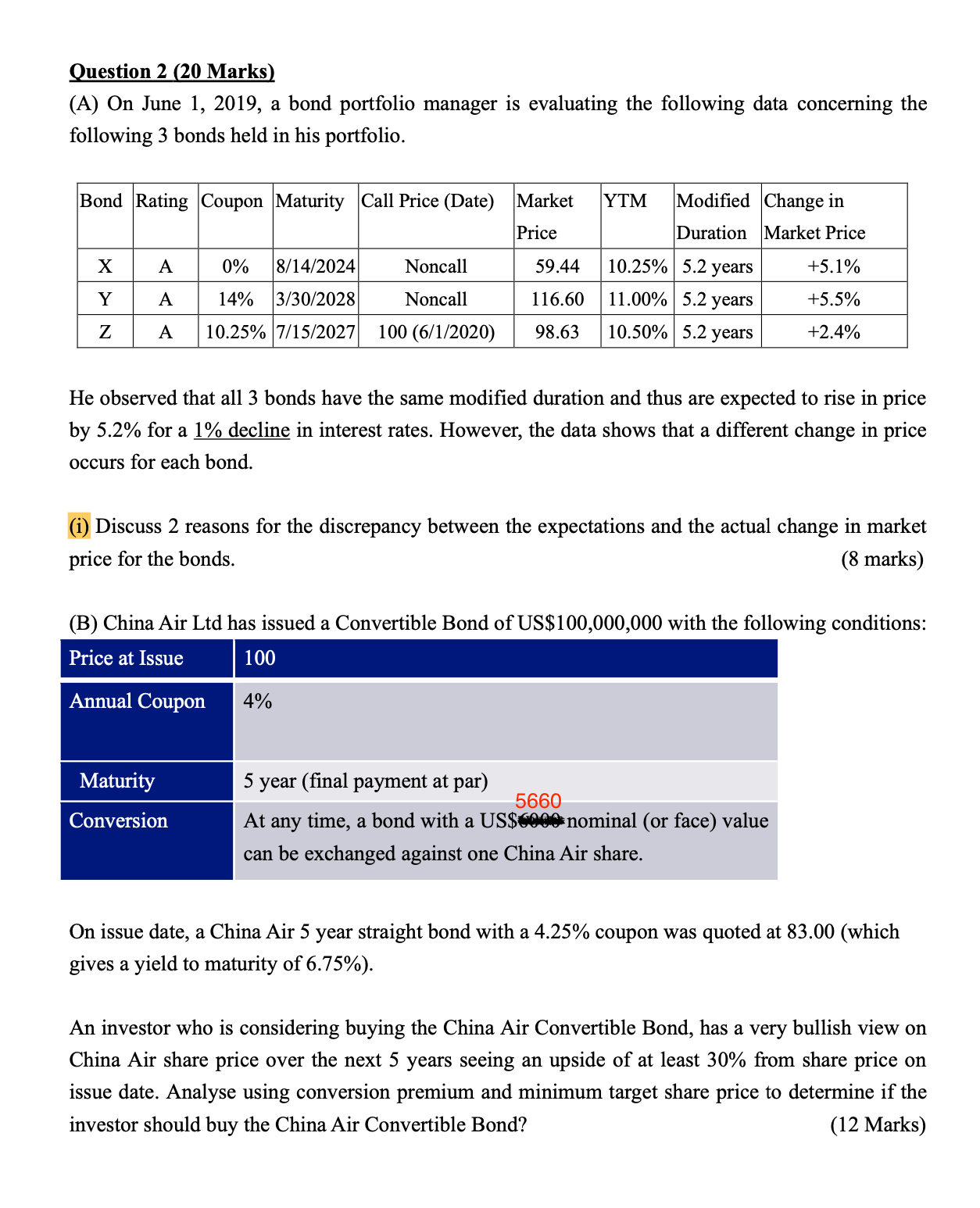

Question 2 (20 Marks) (A) On June 1, 2019, a bond portfolio manager is evaluating the following data concerning the following 3 bonds held in his portfolio. Bond Rating Coupon Maturity Call Price (Date) Market YTM Modified Change in Price Duration Market Price X A 0% 8/14/2024 Noncall 59.44 10.25% 5.2 years +5.1% V A 14% 3/30/2028 Noncall 116.60 11.00% 5.2 years +5.5% Z A 10.25% 7/15/2027 100 (6/1/2020) 98.63 10.50% 5.2 years +2.4% He observed that all 3 bonds have the same modified duration and thus are expected to rise in price by 5.2% for a 1% decline in interest rates. However, the data shows that a different change in price occurs for each bond. (i) Discuss 2 reasons for the discrepancy between the expectations and the actual change in market price for the bonds. (8 marks) (B) China Air Ltd has issued a Convertible Bond of US$100,000,000 with the following conditions: Price at Issue 100 Annual Coupon 4% Maturity 5 year (final payment at par) 5660 Conversion At any time, a bond with a US$6000 nominal (or face) value can be exchanged against one China Air share. On issue date, a China Air 5 year straight bond with a 4.25% coupon was quoted at 83.00 (which gives a yield to maturity of 6.75%). An investor who is considering buying the China Air Convertible Bond, has a very bullish view on China Air share price over the next 5 years seeing an upside of at least 30% from share price on issue date. Analyse using conversion premium and minimum target share price to determine if the investor should buy the China Air Convertible Bond? (12 Marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts