Question: Question 2 (20 Marks) (A) On June 1, 2019, a bond portfolio manager is evaluating the following data concerning the following 3 bonds held in

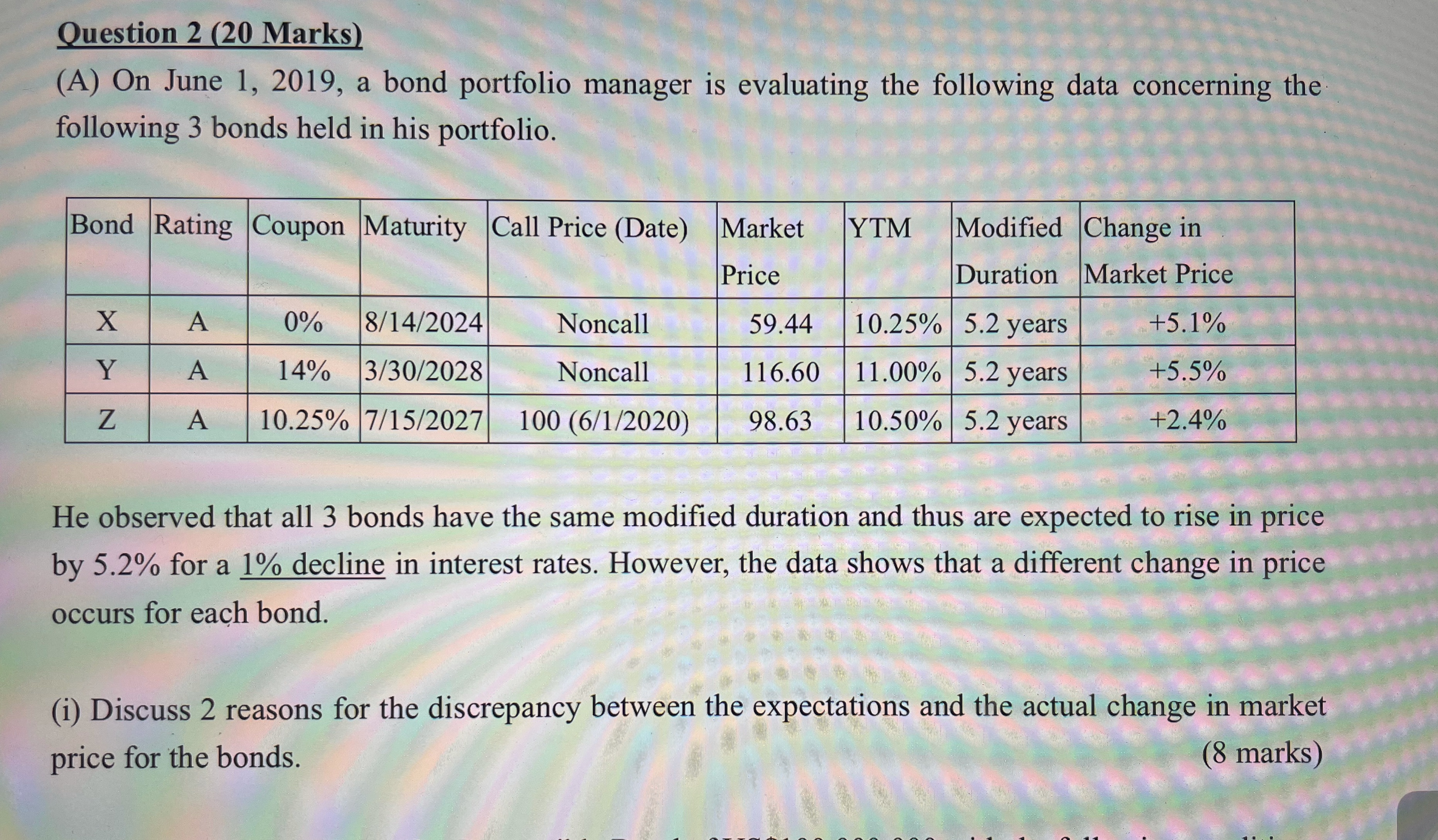

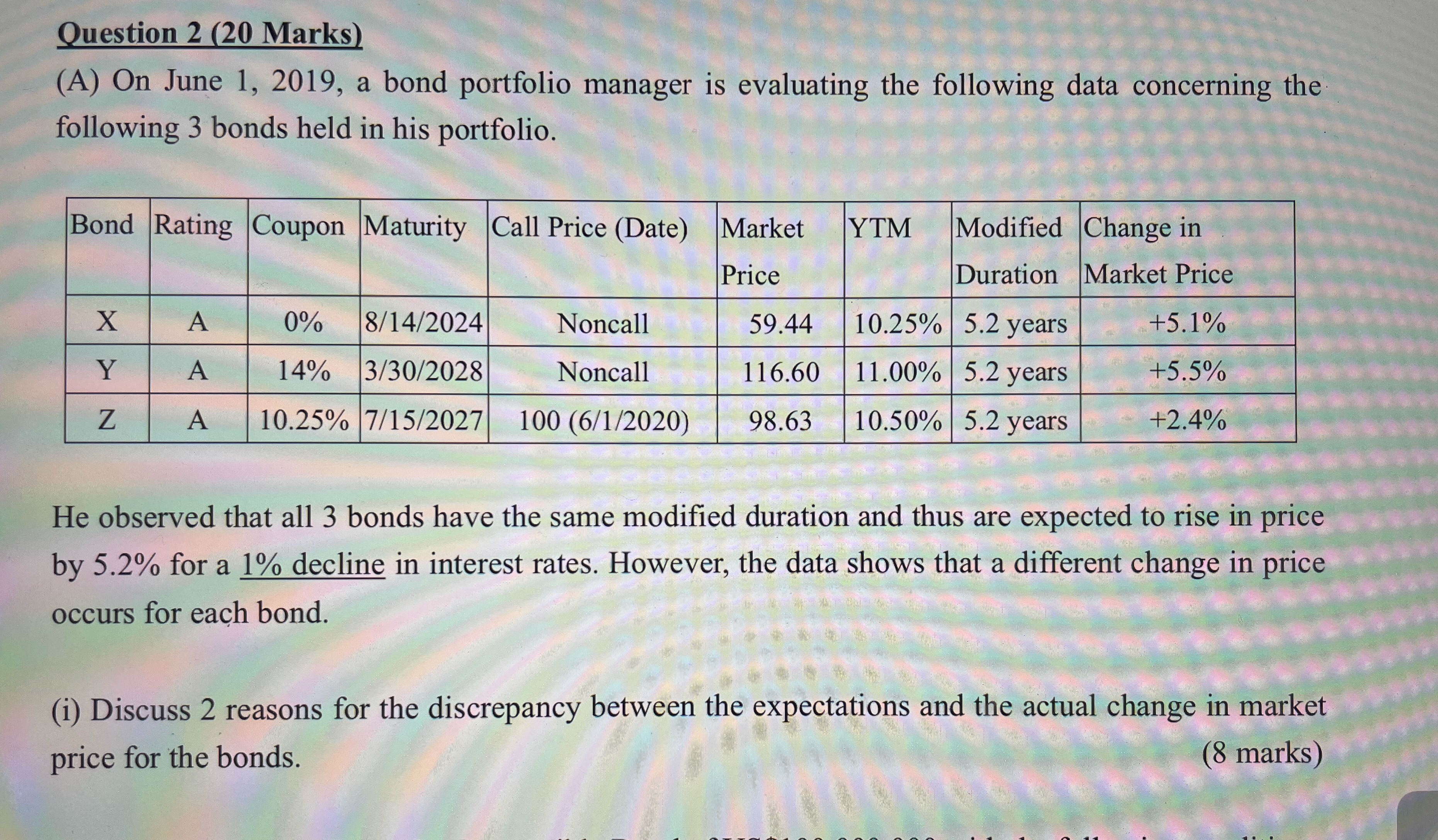

Question 2 (20 Marks) (A) On June 1, 2019, a bond portfolio manager is evaluating the following data concerning the following 3 bonds held in his portfolio. Bond Rating Coupon Maturity Call Price (Date) Market YTM Modified Change in Price Duration Market Price X A 0% 8/14/2024 Noncall 59.44 10.25% 5.2 years +5.1% Y A 14% 3/30/2028 Noncall 116.60 11.00% 5.2 years +5.5% Z A 10.25% 7/15/2027 100 (6/1/2020) 98.63 10.50% 5.2 years +2.4% He observed that all 3 bonds have the same modified duration and thus are expected to rise in price by 5.2% for a 1% decline in interest rates. However, the data shows that a different change in price occurs for each bond. (i) Discuss 2 reasons for the discrepancy between the expectations and the actual change in market price for the bonds. (8 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts