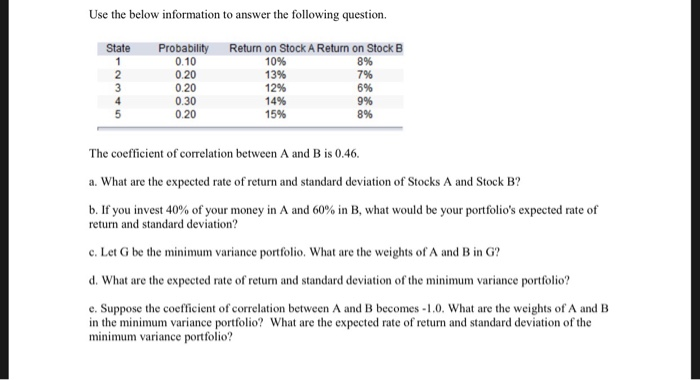

Question: Please show all equations and work as necessary. Use the below information to answer the following question State Probability 0.10 0.20 0.20 0.30 0.20 Return

Use the below information to answer the following question State Probability 0.10 0.20 0.20 0.30 0.20 Return on Stock A Return on Stock B 10% 13% 1296 14% 15% 8% 7% 6% 996 8% The coefficient of correlation between A and B is 0.46 a. What are the expected rate of return and standard deviation of Stocks A and Stock B? b. If you invest 40% of your money in A and 60% in B, what would be your portfolio's expected rate of return and standard deviation? c. Let G be the minimum variance portfolio. What are the weights of A and B in G? d. What are the expected rate of return and standard deviation of the minimum variance portfolio e. Suppose the coefficient of correlation between A and B becomes-1.0. What are the weights of A and B in the minimum variance portfolio? What are the expected rate of return and standard deviation of the minimum variance portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts