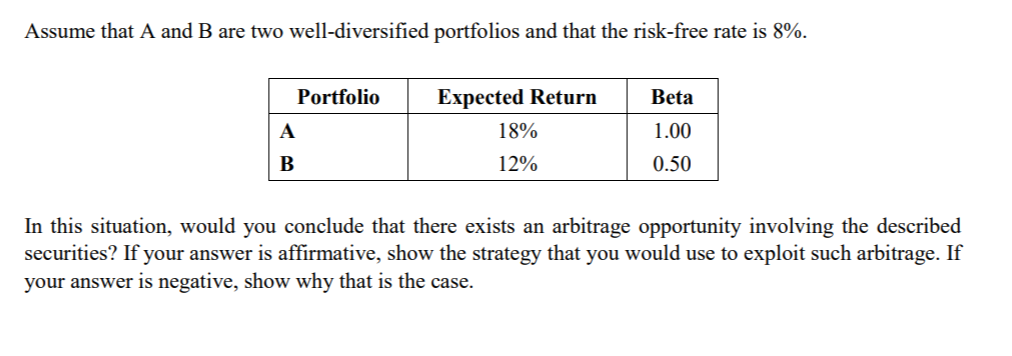

Question: Please show all equations and work as needed. Assume that A and B are two well-diversified portfolios and that the risk-free rate is 8%. PortfolioExpected

Please show all equations and work as needed.

Assume that A and B are two well-diversified portfolios and that the risk-free rate is 8%. PortfolioExpected Returm 1.00 18% 12% 0.50 In this situation, would you conclude that there exists an arbitrage opportunity involving the described securities? If your answer is affirmative, show the strategy that you would use to exploit such arbitrage. If your answer is negative, show why that is the case

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock