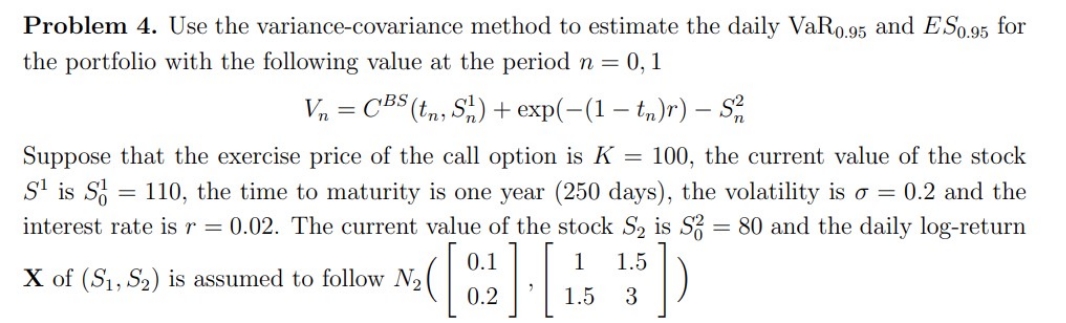

Question: please show all steps Problem 4. Use the variance-covariance method to estimate the daily VaR0_95 and E8035 for the portfolio with the following value at

please show all steps

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock