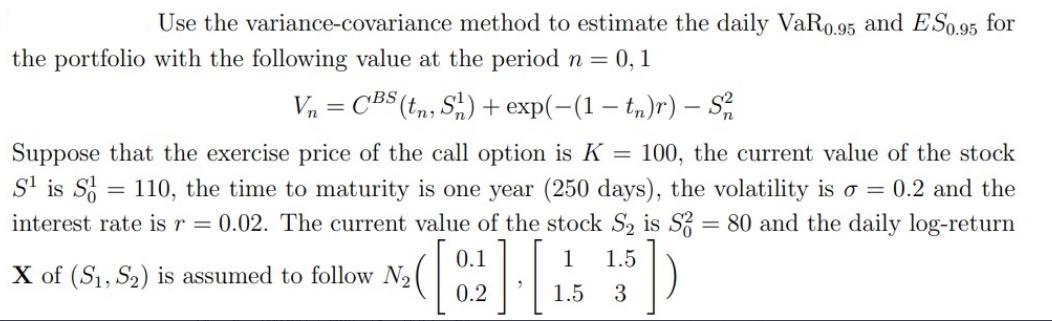

Question: Use the variance-covariance method to estimate the daily VaR0.95 and ES0.95 for the portfolio with the following value at the period n = 0,

Use the variance-covariance method to estimate the daily VaR0.95 and ES0.95 for the portfolio with the following value at the period n = 0, 1 Vn=CBS (tn, S) + exp(-(1-tn)r) - S/2 Suppose that the exercise price of the call option is K = 100, the current value of the stock S is S 110, the time to maturity is one year (250 days), the volatility is o = 0.2 and the interest rate is r = 0.02. The current value of the stock S is S2 = 80 and the daily log-return 0.1 1 1.5 ( [02] - [ HEBD 1.5 3 = X of (S1, S) is assumed to follow N

Step by Step Solution

★★★★★

3.49 Rating (159 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock