Question: Please show all work and any formulas used . much appreciated Question Consider the following scenario analysis for stocks X and Y. Assume that you

Please show all work and any formulas used . much appreciated

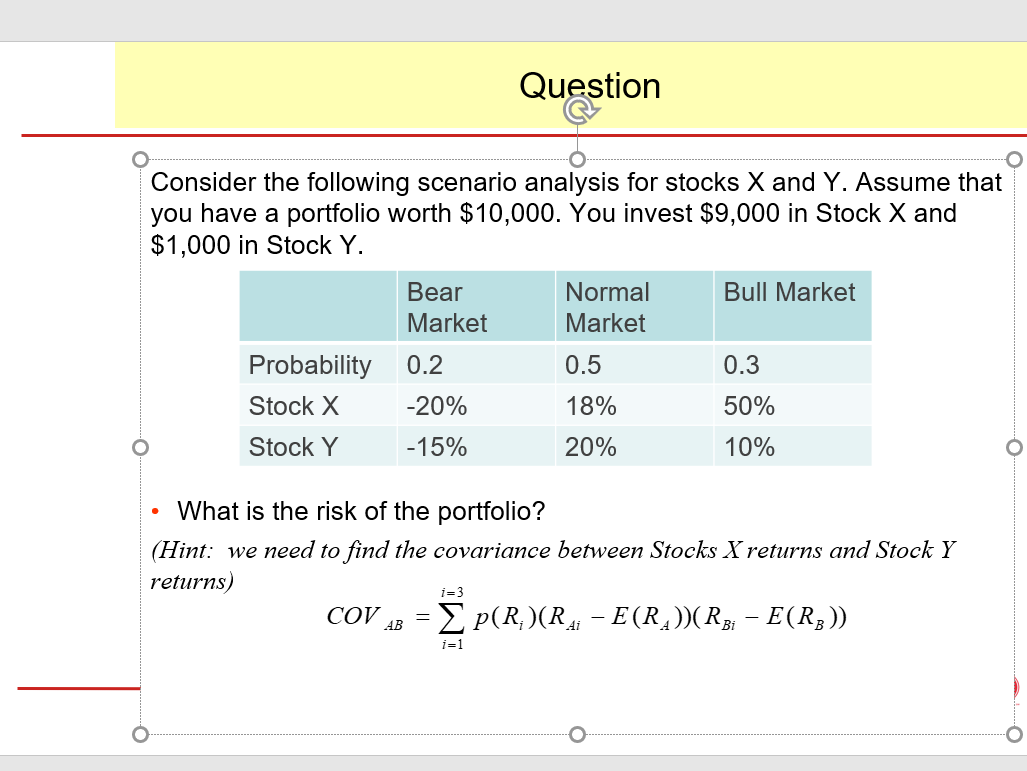

Question Consider the following scenario analysis for stocks X and Y. Assume that you have a portfolio worth $10,000. You invest $9,000 in Stock X and $1,000 in Stock Y. Bull Market Bear Market Normal Market 0.2 0.5 0.3 Probability Stock X -20% 18% 50% Stock Y -15% 20% 10% . What is the risk of the portfolio? (Hint: we need to find the covariance between Stocks X returns and Stock Y returns COV [AB = P(R)(R41 - E(R.))(Rg; E(R3)) i=3 i=1 b

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock