Question: Please show all work. (No Excel) Problem IV (12 points) Here are the risk and return estimates for the T-Note Portfolio (#1) and the S&P

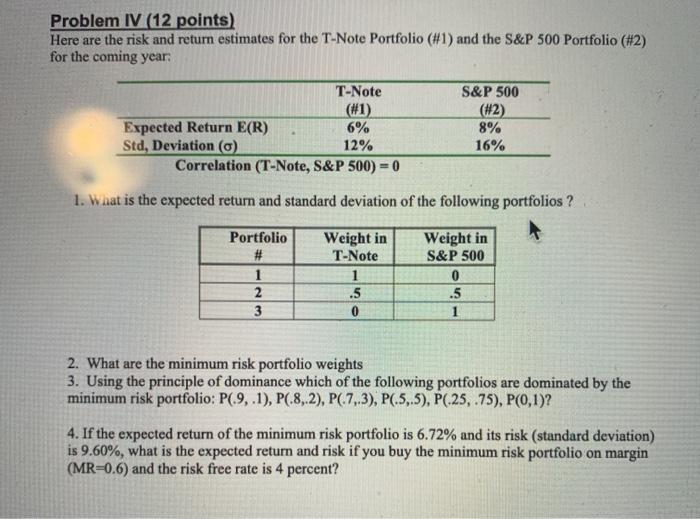

Problem IV (12 points) Here are the risk and return estimates for the T-Note Portfolio (#1) and the S&P 500 Portfolio (#2) for the coming year: T-Note S&P 500 (#2) 8% 16% Expected Return E(R) 6% Std, Deviation (0) 12% Correlation (T-Note, S&P 500) = 0 1. What is the expected return and standard deviation of the following portfolios ? Portfolio # 1 2 3 Weight in T-Note 1 .5 0 Weight in S&P 500 0 .5 1 2. What are the minimum risk portfolio weights 3. Using the principle of dominance which of the following portfolios are dominated by the minimum risk portfolio: P(9.1), P(-8,2), P(7.3), P6.5,.5), P(25.75), P(0,1)? 4. If the expected return of the minimum risk portfolio is 6.72% and its risk (standard deviation) is 9.60%, what is the expected return and risk if you buy the minimum risk portfolio on margin (MR=0.6) and the risk free rate is 4 percent

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts